BONDS: Supply Underpinning Yields; 10-year Gilt/Bund Close To YTD Low

- Impending sovereign supply is likely underpinning UK and German yields this morning, keeping the 10-year Gilt/Bund spread close to the 2025 low of ~177.5bps.

- The DMO will sell GBP3.75bln of the new 4.125% Mar-33 Gilt at 1000GMT. Meanwhile, Germany will sell E4.5bln of the 10-year 2.60% Aug-35 Bund at 1030GMT.

- The April low continues to contain downside in 10-year Gilts, which are currently little changed at 4.40%.

- Spanish Q3 flash GDP confirmed expectations at 0.6% Q/Q (vs 0.8% prior), but domestic demand signals were solid. UK September consumer credit was in line with expectations.

- The EFSF has sent an RFP for an upcoming transaction, which will likely be held early next week.

- In the Eurozone, focus remains on the ECB decision (Thurs), Eurozone Q3 flash GDP (Thurs) and October flash inflation (Fri). In the UK, spillover from US Treasuries amid today’s FOMC decision will be eyed alongside ongoing budget headline flow.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: Belgium HICP a Tenth Higher Y/Y, Core CPI Notably Higher

Belgium HICP rose to 2.7% Y/Y (from 2.6% prior), its highest rate since June according to the Statbel flash estimate. National CPI (non HICP) inflation meanwhile also accelerated, to 2.12% in September from 1.91% previously.

- Sticking to the non-HICP details, core CPI (ex energy & unprocessed food) ticked up notably, to 2.61% Y/Y (vs 2.30% prior).

- Services inflation was almost unchanged at 3.47% Y/Y (3.48% prior).

- "Inflation for food products (including alcoholic beverages) stands at 3.32% this month, compared with 2.42% last month.", INE adds. Food inflation is expected to be roughly unchanged on the yearly rate on the Eurozone-wide HICP release, and may undergo increased scrutiny in the coming months following a recent ECB blog post drawing attention to the importance for inflation expectations of the category. After the Belgian increase, we will be watching to see if we get a similar increase in other countries - which could then provide an upside surprise to headline HICP.

- Energy inflation meanwhile has dropped in September in Belgium, with a -1.48% Y/Y rate (vs -0.75% August, -1.86% July). Energy is seen to drive an uptick in the Eurozone-wide headline print in September.

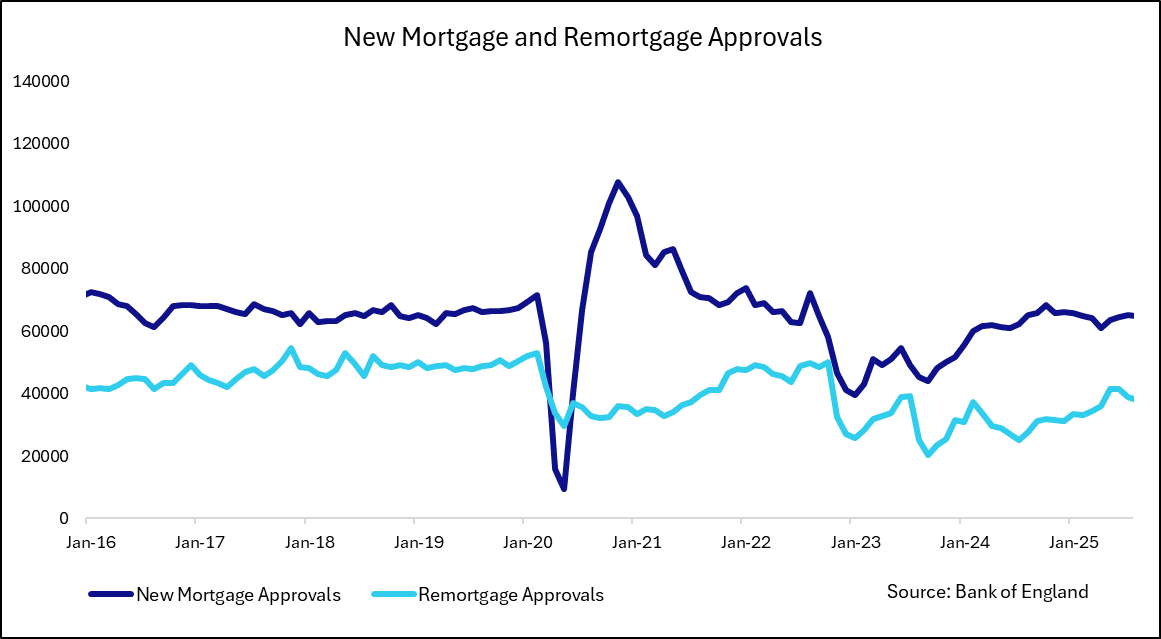

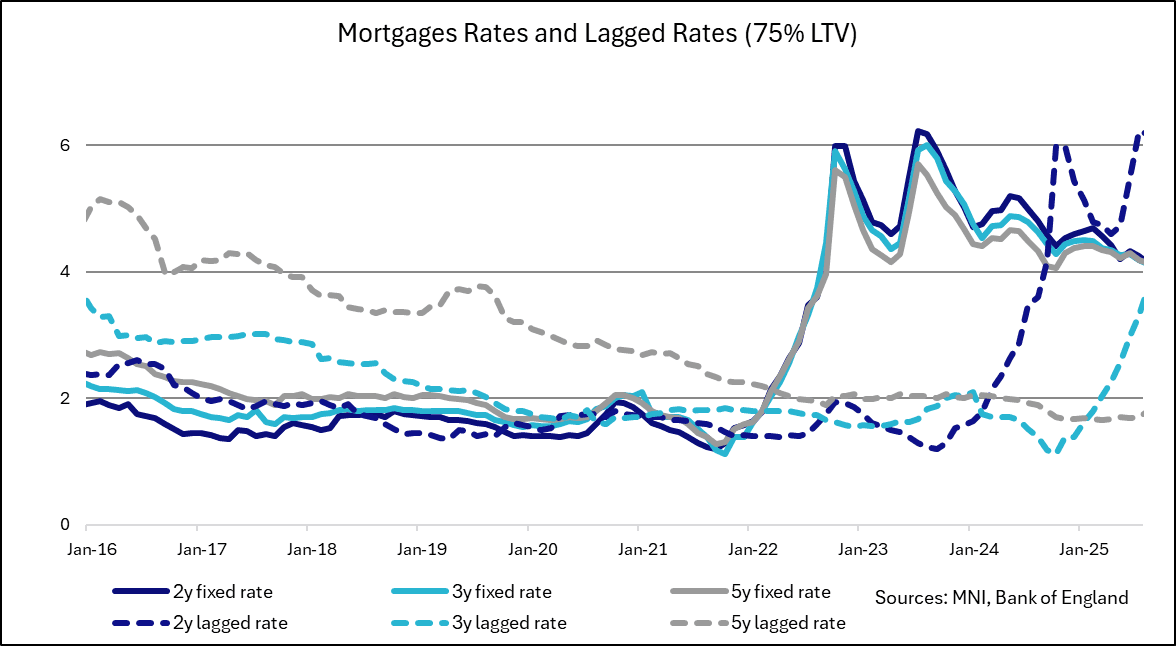

UK DATA: BOE Credit Data Broadly In Line, Weaker Mortgage Lending, Higher M4

BOE money and credit data for August came in broadly in line with expectations, though there were slight drops in secured lending and mortgage approvals. Mortgage rates fell due to the August rate cut, though the bar for future base rate cuts appears high. M4 money supply increased on the year at a faster rate than in July.

- Despite steady and in-line mortgage approvals data (64.7k vs 64.6k cons, 65.4k July), net lending on dwellings came in slightly below expectations at GBP4.31bn (vs 4.8bn cons, 4.52bn July).

- Likely due in part to the August rate cut, quoted mortgage rates fell across the maturity profile, with 2y, 3y and 5y 75% LTV fixed rates all sitting between 4.12-4.14%. As households assess refinancing conditions, this drop will be welcome. Those refinancing from a 2y fixed rate two years ago would now see a c.2ppt lower interest rate for the same mortgage, however the passthrough of previous rate cuts is not yet complete for those on longer mortgage terms.

- In March, we saw frontloading of home sales ahead of the stamp duty changes, though given the lagged nature of housing data it's difficult to assess whether these figures have returned to normal levels. Given today's release, mortgage approvals and secured lending seem to be showing continued strength despite small dips in lending.

- Also in the release, M4 money supply rose to 0.4% M/M, 3.4% Y/Y (vs 0.1% M/M, 2.9% Y/Y July).

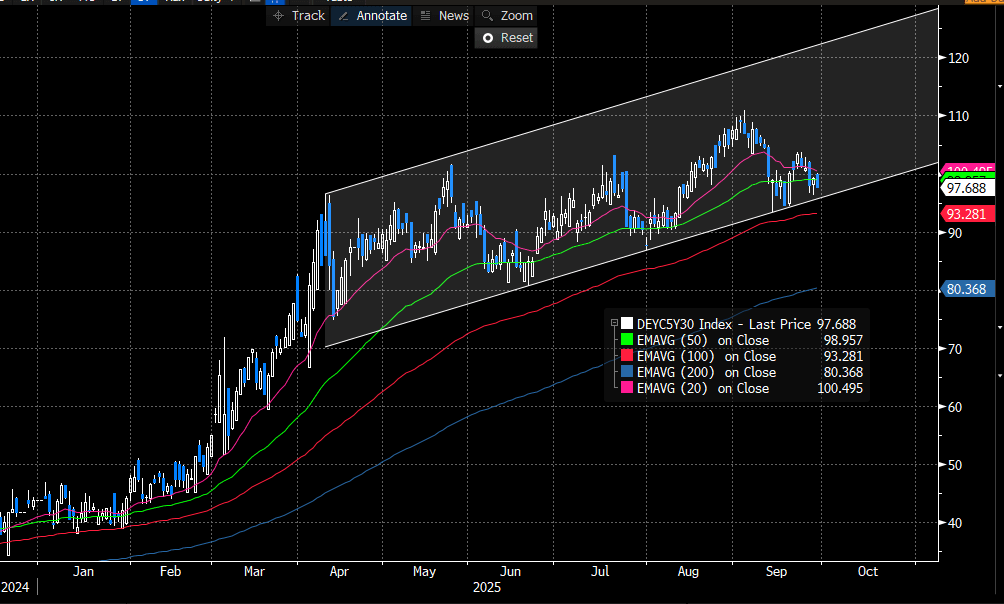

EGBS: German Curve Bull Flatter Amid Russia/Ukraine and US Shutdown Risks

The German curve is bull flatter, but trendline support in 5s30s remains intact for now. Yields are 1 to 3bps lower across the cure, with 5s30s down 1.5bps at 97.7bps. Trendline support resides at 95.7bps today.

- This morning’s headline flow has been relatively light, but markets have been digesting ongoing Russia/Ukraine tensions, increased US government shutdown risks and semi-core/peripheral EGB ratings action since Friday’s close.

- Bund futures are +19 ticks at 128.45, off session highs of 128.57. Resistance at the 20-day EMA (128.45) has been pierced, exposing the Sep 17 high at 129.13.

- 10-year EGB spreads to Bunds are biased up to 1bp tighter with the exception of OATs. Diverging ratings action are playing a part. France’s sovereign rating outlook was moved to negative at Scope Ratings on Friday, while Spain received one-notch upgrades at both Fitch & Moody’s. European equities are off session highs, but remain up 0.35% today.

- In data, Spanish flash September core HICP was a little softer-than-expected, but had a limited market impact. Eurozone September sentiment was a touch above consensus at 95.5 (vs 95.3 cons and prior).

- ECB’s Makhlouf suggested the bank was “near the bottom” of its easing cycle. These were Makhlouf’s first comments since the September decision. Overall, we’d say they are broadly in line with the Governing Council median. ECB Chief Economist Lane is scheduled to speak at 1300BST.

Figure 1: German 5s30s Curve