MNI US MARKETS ANALYSIS - CPI to Show Pace of Passthrough

Highlights:

- CPI report next up, markets look to gauge energy price passthrough

- Islamabad negotiations set to start from Saturday - but attendance remains up-in-the-air

- Ukraine - Russia deal prospects seem to improve, helping support risk at the margins

US TSYS: Light Volumes Ahead Of March CPI Report, TYM6 Resistance Monitored

Treasuries are mildly lower overnight ahead of today’s CPI report on particularly light overnight volumes compared to those seen since the start of the US-Israel-Iran war. TYM6 is off highs from earlier in the week but resistance is still monitored for a signal of whether what have been corrective gains can extend.

- The front end yesterday fully reversed the initial rally on Lebanon negotiation and Israel scaling back Lebanon strikes headlines but with a somewhat more limited paring of the moves in the long end.

- President Trump demanded Iran reopen the Strait of Hormuz, raising pressure on Tehran before talks to turn a fragile ceasefire into lasting peace. US and Iranian delegations are set to meet in Pakistan on Saturday.

- This morning's reports of Zelenskiy's top aide seeing Ukraine nearing a deal with Putin only prompted a small rally.

- Cash yields are 1.4-1.8bp higher across the curve.

- TYM6 trades at 111-08 (+00+) on particularly light cumulative volumes of 175k.

- Resistance is monitored at 111-20 (50-day EMA) having probed it earlier this week with 111-21 (Apr 8 high), with a clear break required to signal scope for a stronger recovery away from what have been corrective gains. Next lies 111-31 (50% retrace of Mar 2-27 bear leg).

- Support meanwhile is seen at 111-00+ (Apr 9 low) before 110-16 (Apr 2 low) and ultimately the bear trigger at 109-24 (Mar 27 low).

- Data: CPI Mar (0830ET), Real av earnings Mar (0830ET), Factory orders Feb (1000ET), U.Mich Apr prelim (1000ET), Federal budget balance Mar (1400ET)

- Politics: Trump in policy meeting (1530ET), Trump departs White House (1650ET), Trump in MAGA roundtable dinner (1915ET), Trump departs Trump Winery (1510ET)

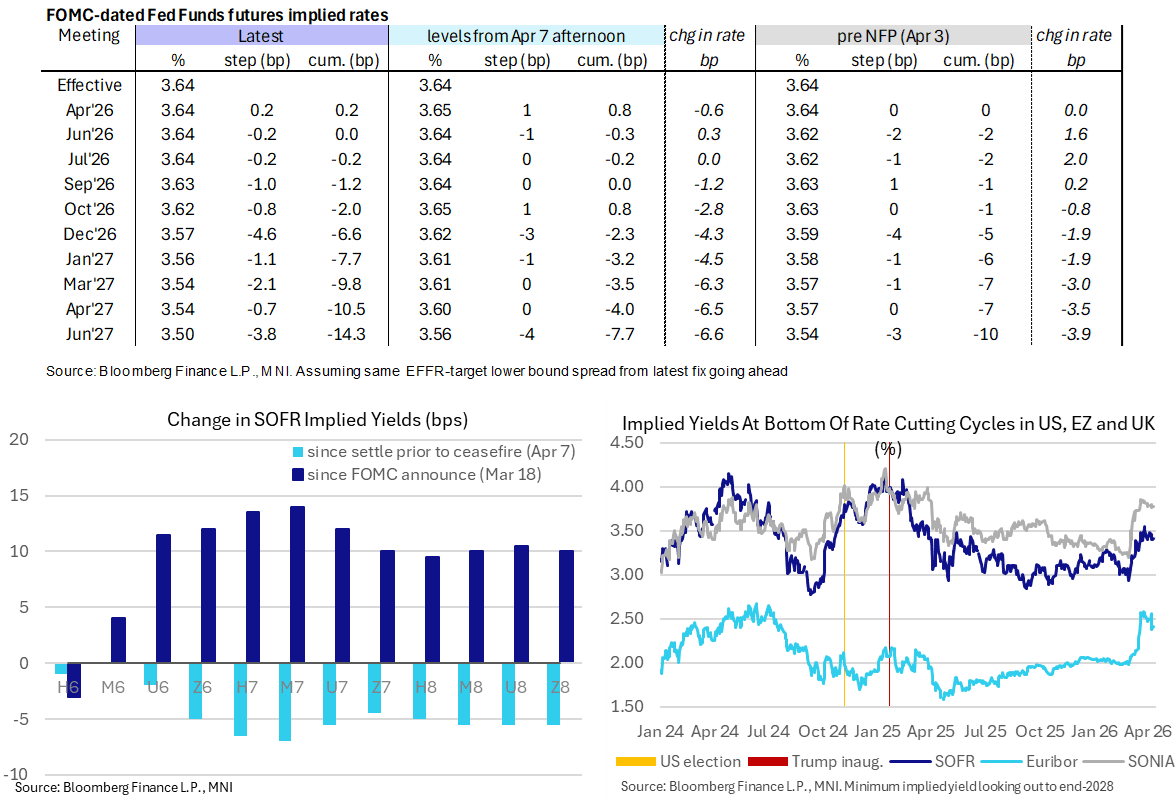

STIR: Mild Fed Easing Bias Held Ahead Of March CPI Report

- US rates have seen a largely steady overnight, consolidating yesterday’s reversal of initial gains on Lebanon negotiation and Israel scaling back Lebanon strikes headlines.

- This morning's reports of Zelenskiy's top aide seeing Ukraine nearing a deal with Putin saw a small rally away from session lows.

- Data has recently played a reduced role although today’s CPI report could be more notable as it captures the historically sharp rise in fuel prices with spillover watched.

- MNI CPI Preview: https://media.marketnews.com/USCPI_Prev_Apr2026_76aa0947d0.pdf

- Cumulative cuts from 3.64% effective: 0bp Apr, 0bp Jun, 0bp Jul, 1.5bp Sep, 2bp Oct and 7bp Dec before building to 15bp in Jun 2027.

- SOFR futures are mostly 0.5-1 tick lower overnight, with the terminal implied yield of 3.41% (Z7) little changed compared to the past two closes. It compares with a range of 3.075% (Mar 2) - 3.55% (Mar 26) for closes since US-Israel strikes on Iran on Feb 28.

UKRAINE: Moscow & Kyiv Still Poles Apart On Key Issues

Following on from the declaration of a 32-hour Orthodox Easter ceasefire to run from 16:00 local time (09:00ET, 14:00BST) on Saturday, 11 April, through to the end of Sunday, 12 April, Bloomberg News reports that an aide to Ukrainian President Volodymyr Zelenskyy said to the outlet last week that both sides want the war to end and "I don’t think it will be long".

- As MNI notes (see EM FX: PLN, HUF Rally on Ukraine Story, But Moves Limited Overall) the article carries some notable caveats. Crucially, "maximalist" positions from both sides, especially with regard to territorial control, have shown little to no signs of resolution.

- Russian state-run Tass reports comments from Kremlin spox Dmitri Peskov. He confirms the visit of special presidential envoy Kirill Dmitriev to the US, but adds that he "is not negotiating on a Ukraine settlement", and the visit does not represent the resumption of peace negotiations.

- Another crucial issue has been security guarantees for Ukraine. While Kyiv has sought significant commitments from the US, recent rhetoric from the White House has raised questions about its reliability. The Guardian quotes a European official saying "Ukraine is rightfully questioning whether these American security guarantees really stand for anything.”

- Indeed, speaking to The Rest is Politics podcast, Ukrainian President Volodymyr Zelenskyy notes that Europe's security (including that of Ukraine) may in the future be reliant on internal rather than external support. "If the United States truly thinks about withdrawing from NATO, then European security will be based solely on the European Union. But not in its current form. I think that the EU is in a situation where it needs more countries. The UK, Ukraine, Türkiye, and Norway."

RATINGS: Moody’s On France & S&P On UK Due After Hours

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Moody’s on France (current rating: Aa3; Outlook Negative)

- S&P on the United Kingdom (current rating: AA; Outlook Stable)

- Morningstar DBRS on Lithuania (current rating: A (high), Stable Trend) & Malta (current rating: A (high), Stable Trend)

- Scope Ratings on Hungary (current rating: BBB; Outlook Stable) & Luxembourg (current rating: AAA; Outlook Stable)

- Please use this link to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings).

- Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis.

- Rating agencies may also adjust their schedules during the year.

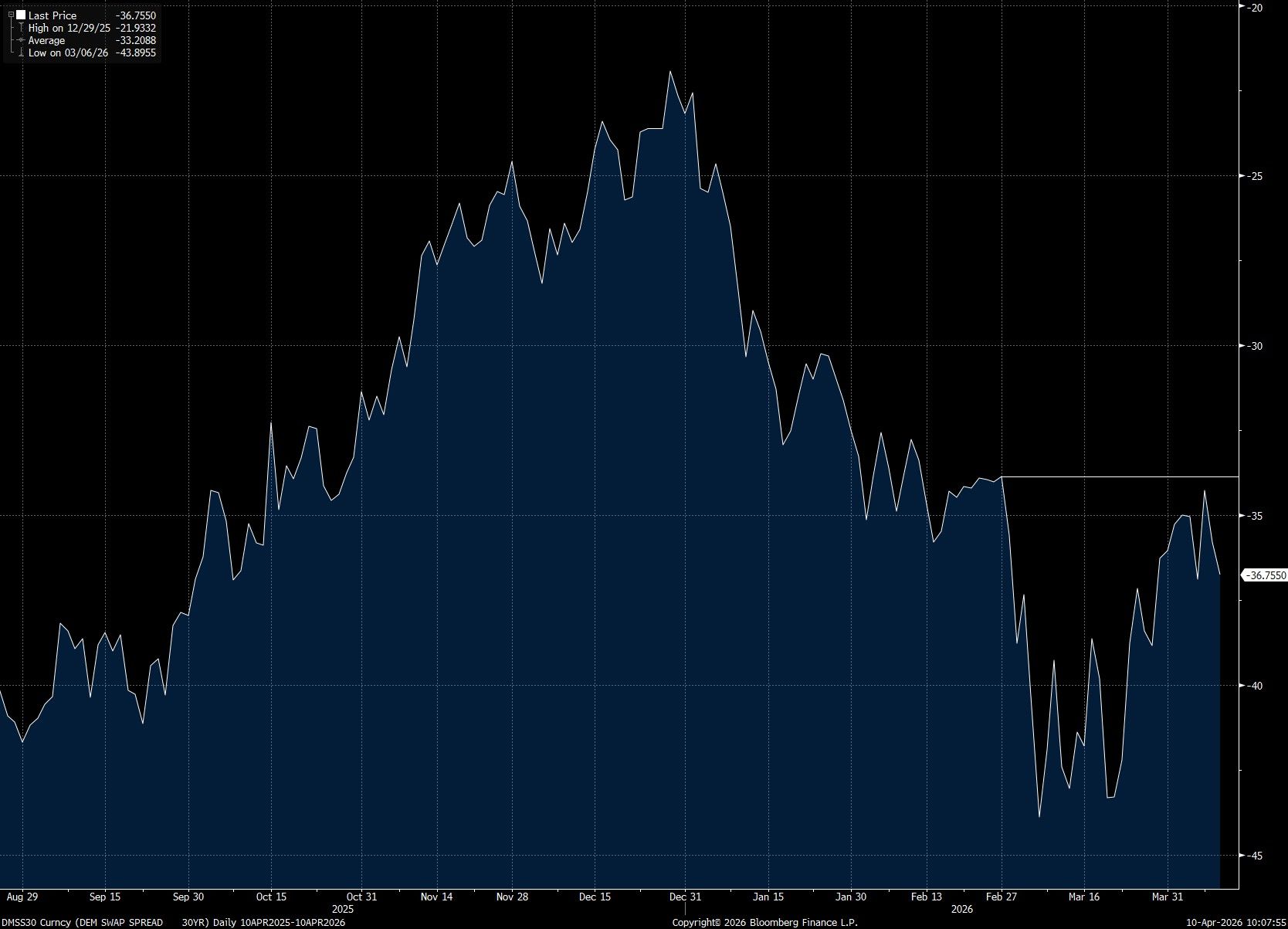

SWAPS: Buxl Weakness Comes Alongside Failure To Retake Pre-Iran Levels In Spds

Note that the weakness in Buxl seen over the past couple of sessions comes after a recovery in 30-Year German swap and ASW spreads stalled at/ahead of pre-Iran escalation levels (in closing terms).

- Doubts surrounding the longevity/viability of the U.S.-Israel-Iran ceasefire have weighed on long end swap & ASW spreads since yesterday’s open.

- Early March proved that the long end of the German curve does not always hold safe haven status (evidenced by the move lower in swap spreads and ASWs as risk-off flows intensified).

- This was largely a product of inflationary risks stemming from the Middle East, with Germany’s newfound preference for fiscal loosening (albeit with questions still evident re: the ultimate scale that any related investment will reach) continuing to provide a background consideration.

- Note that pre-existing spread widener positioning linked to the Dutch pension fund transition may have also factored into the early March move in swap spreads, with the aforementioned macro pressure adding to disappointment re: the size of flows and lack of market footprint since the latest transition date.

Fig. 1: German 30-Year Swap Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

MNI US CPI PREVIEW: A Crude Shift Further From Target

Released Friday at 0830ET, headline CPI is expected to have surged in March with a 0.9-1.0% M/M increase due to a historically large energy price increase on the US-Israel-Iran war. Core CPI is seen increasing a more modest 0.27% M/M in March after 0.22% M/M, with much more limited initial spillover from the energy shock. Within core, expect transportation-related categories to be in focus plus broader indications of supply chain pressures which ticked up to a fresh high since early 2023 according to the NY Fed.

MNI POLITICAL RISK ANALYSIS: Hungary Election Preview

For the first time since the governing Fidesz party took power in 2010, the government faces a serious electoral challenge on 12 April, which could see Prime Minister Viktor Orbán ousted after an unbroken 16-year period in office. In this preview, we provide a background to the election race, an explainer of the electoral system for the National Assembly and identities of the main political parties, a chartpack of the latest opinion polling and predictions market odds, analysis of various post-election scenarios with assigned probabilities, a financial market overview, and views from sell-side analysts.

MNI POLITICAL RISK ANALYSIS: Peru Election Preview

Peru holds its general election on 12 April in a contest that follows five years of political chaos in the aftermath of the 2021 vote. Voters will determine the next president and vice president, as well as all members of Congress (130 seats in the Chamber of Deputies, 60 in the Senate), following a return to a bicameral legislature. In this preview, we provide a background to the election race, an explainer of the electoral system and identities of the main presidential candidates, a chartpack of the latest opinion polling and predictions market odds, analysis of various post-election scenarios with assigned probabilities, a financial market and EM credit overview, and views from sell-side analysts.

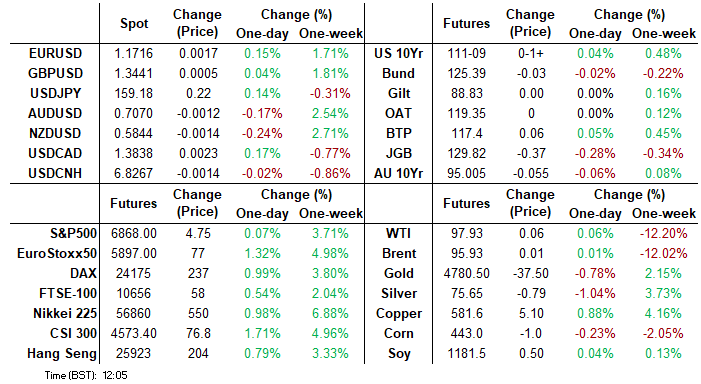

FOREX: Dollar Index Consolidating 1% Losses This Week, US CPI Awaited

- Modest upward pressure on crude futures has tilted the dollar index into positive territory early Friday, but net adjustments for the major pairs remain very contained. Overall, the DXY is consolidating a 1% slide this week, as cautious optimism surrounding the ceasefire in the Middle East takes away some of the safe haven demand for the greenback.

- AUD, NZD and SEK are the worst performers on Friday, eroding around 0.3% of their solid rallies this week, with potential profit taking dynamics at play as we approach the weekend and markets remain nervous over the upcoming negotiations in Pakistan.

- For NZDUSD specifically, the risk on impulse and the hawkish tilt to the RBNZ meeting this week keeps the pair around 2.7% off the week’s lows, and a weekly close back above the 50-day EMA at 0.5844 will be closely eyed.

- The Japanese yen is a touch weaker today amid the higher core yields, helping USDJPY re-establish itself back above 159.00 and EURJPY above 186.00. This week’s EURJPY climb has resulted in a breach of key short-term resistance at 184.77, the Feb 25 high, highlighting a bullish reversal and a recent false break of a bull channel support drawn from the Feb 28 ‘25 low. 186.36 is the next level on the topside (the Feb 9 high), before 186.87, the Jan 23 high and a key medium-term resistance.

- All focus turns to today’s release of US CPI. Other scheduled data points include Canada employment and prelim readings of UMich sentiment and inflation expectations.

OPTIONS: Expiries for Apr10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E786mln), $1.1725(E767mln)

- USD/JPY: Y158.00($1.8bln), Y159.50($781mln), Y160.00($1.1bln)

- GBP/USD: $1.3500(Gbp572mln)

- EUR/GBP: Gbp0.8700(E550mln)

- EUR/JPY: Y178.00(E650mln)

- NZD/USD: $0.5800(N$503mln)

- USD/CNY: Cny6.8000($750mln)

EQUITIES: EuroStoxx Futures Holding Onto Gains, Bull Trigger at 6143.00

- EuroStoxx 50 futures are holding on to their recent gains. The contract has traded through both the 20- and 50-day EMAs, paving the way for a climb towards 5945.47, a Fibonacci retracement point. Note that a break of 5945.47 would expose the key resistance and bull trigger at 6143.00, the Feb 26 high. First key support to watch lies at 5525.00, the Apr 2 low. A move lower and a breach of this support would highlight a reversal.

- A strong rally in S&P E-Minis this week highlights an extension of the reversal that started Mar 31. Note that trend signals remain bearish and for now, this suggests that gains are corrective. A continuation higher would open 6921.09 next, a Fibonacci retracement point. Key medium-term resistance and the bull trigger is far off at 7096.50, the Jan 28 high. Initial firm support to watch lies at 6567.00, the Apr 6 low.

COMMODITIES: This Week's Sharp WTI Pullback Still Considered Corrective

- A sharp pullback in WTI futures this week is for now, considered corrective. The contract has traded through the 20-day EMA and this exposes a key support around the 50-day EMA, at $85.87. A clear break of the 50-day average is required to highlight a stronger short-term reversal. On the upside key resistance and the bull trigger has been defined at $117.63, the Apr 7 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- Recent gains in Gold appear to be corrective, however for now, the short-term bull cycle remains intact. The metal has pierced the 50-day EMA, at $4782.5. This signals scope for an extension towards $4914.9, a Fibonacci retracement point. Clearance of this level would open the $5000.0 handle. Initial firm support to watch lies at $4554.2, the Apr 2 low. Clearance of this level would be bearish.

| Date | GMT/Local | Impact | Country | Event |

| 10/04/2026 | - | *** | New Loans | |

| 10/04/2026 | - | *** | Money Supply | |

| 10/04/2026 | - | *** | Social Financing | |

| 10/04/2026 | 1200/0800 | ** | Brazil Final CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1800/1400 | ** | Treasury Budget |