MACRO ANALYSIS: MNI US Macro Weekly: Fed Divided As Data Trickles Back In

We've just published our latest US Macro Weekly - Download Full Report Here

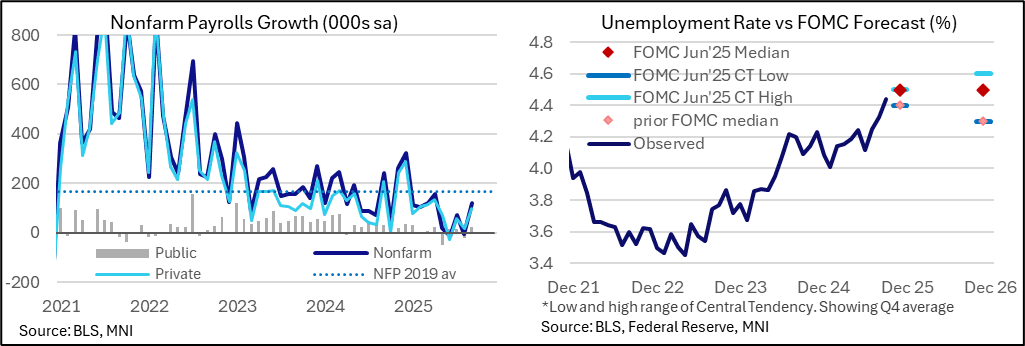

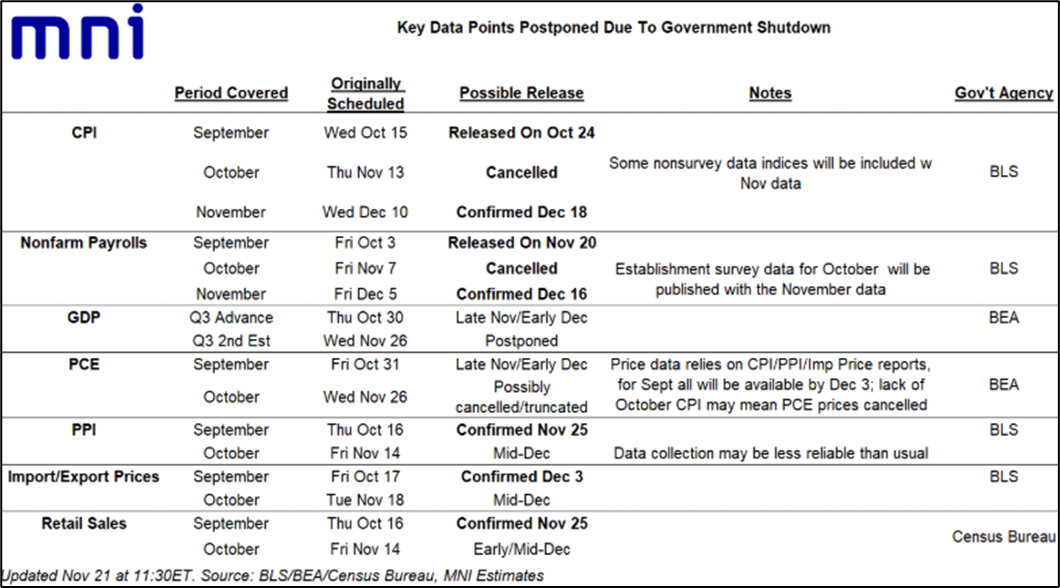

- The “fog” of data following the federal government shutdown is only slowly lifting, with the return of official national-level reports this week largely limited to August and September-vintage releases.

- The long-postponed September Employment Situation report delivered a largely solid if slightly stale snapshot of the US labor market, with an unexpectedly large uptick in the unemployment rate to a 4-year high appearing to outweigh consensus-beating payrolls growth to deliver a slightly dovish market reaction.

- NY Fed’s Williams however had the largest impact of the week on Friday, in an uncharacteristic steer from a core member of the FOMC towards a further adjustment in the “near term”. We end the week with 16bp of cuts priced for Dec (vs 6bp pre-payrolls), 25bp for Jan and 58bp for June.

- The minutes for the Oct 28-29 FOMC meeting were hawkish, at the time suggesting that it may only be a minority of the Committee that is pushing for a follow-up cut in December. And most other Fedspeak erred on the hawkish or at least cautious about a December cut side, with various speakers most sounding concerned about the latest increase in the unemployment rate in September.

- But Williams reinforced our view that FOMC voters are leaning to deliver a “hawkish cut” in December, with Williams part of a core bloc including Chair Powell in support.

- The latest BLS reschedulings mean the Fed won't get October or November nonfarm payrolls or CPI reports ahead of its Dec 10 decision, and the October data will be heavily truncated.

- As such the assessment of the current state of play will largely come down to interpreting alternative data points. Again, activity data is showing little sign of relenting, “alternative” measures of labor market health show conditions certainly haven’t improved since September but neither is it likely that the bottom is falling out; and unfortunately the lack of reliable inflation data stands out and is likely to keep hawks cautious.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: GS Below Consensus For CPI, Helped By Lower Airfares

Goldman Sachs are at the dovish end unrounded analyst estimates we've seen for monthly CPI inflation in Friday's September release, eyeing core CPI at 0.25% M/M after the 0.35% M/M in August and headline CPI at 0.33% M/M. We judge the median unrounded analyst estimate to be at 0.32% M/M for core CPI, with a range of 0.25-0.36%.

- Four key component-level trends Goldman expect to see in this report:

- “unchanged used car prices, reflecting the signal from auction prices, and a modest increase in new car prices, reflecting downward pressure on consumer prices from increased dealer incentives.”

- “a 0.3% increase in the car insurance category based on premiums in our online dataset.”

- “a 1.5% decline in airfares in September, reflecting a fading boost from seasonal distortions and a decline in underlying airfares based on our equity analysts’ tracking of online price data.”

- “upward pressure from tariffs on categories that are particularly exposed, such as communication, household furnishings, and recreation, worth +0.07pp on core inflation.”

- “Over the subsequent few months, we expect tariffs to continue to boost monthly inflation and forecast monthly core CPI inflation of around 0.2-0.3%. Aside from tariff effects, we expect underlying trend inflation to fall further, reflecting shrinking contributions from the housing rental and labor markets.” They see core CPI at 3.1% Y/Y in Dec 2025 and core PCE at 3.0% Y/Y (or 2.2% for both excluding tariff effects).

US TSYS: Tsys Buoyed Amid Ongoing Trade Tensions

- Treasuries look to finish modestly higher Wednesday, reversing midmorning losses after Reuters reported the Trump admin "is considering broad restrictions of exports to China made with US software, citing an unnamed US official and three people briefed by US authorities."

- No noticeable reaction in rates after late Bbg headline: "US TO ANNOUNCE 'PICK UP' IN RUSSIA SANCTIONS TODAY OR TOMORROW".

- Treasury futures gain slightly (TYZ5 113-24 +0.0) after $13B 20Y Bond auction re-open (912810UN6) stopped through - drawing a high yield of 4.506% vs 4.517% WI at the cutoff; 2.73x bid-to-cover vs. 2.74x prior.

- The Wall Street Journal reports citing sources that the ADP has stopped providing the Fed with weekly data on private payrolls and earnings. Per the WSJ piece, the Fed has had access to the data since "at least 2018", and was available to the Fed with "a roughly one-week delay". The publicly-available ADP payrolls report is published monthly.

- Equity earnings expected to release after the close include Southwest Airlines, Raymond James, Churchill Downs, Alcoa, Crown Castle, United Rental, Lam Research, Tesla and IBM.

- Thursday's weekly Jobless Claims & Chicago Fed data suspended.

AUDUSD TECHS: Potential Reversal Signal

- RES 4: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 2: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 1: 0.6545 50-day EMA

- PRICE: 0.6505 @ 15:38 BST Oct 22

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

AUDUSD remains in consolidation mode. Price action on Oct 14 continues to highlight a possible reversal pattern - a hammer candle. It signals the end of the bear cycle that started Sep 17. Note that MA studies have remained in a bull-mode position during the latest bear leg, highlighting a dominant M/T uptrend. Initial resistance is 0.6545, the 50-day EMA. A breach of 0.6440, the Oct 14 low, would cancel the reversal pattern and reinstate a bear threat.