US CONSUMER STAPLES: MNI US IG Consumer: Week in Review

MNI US IG Consumer: Week in Review Consumer names in our coverage universe on average were -0.9bps,...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

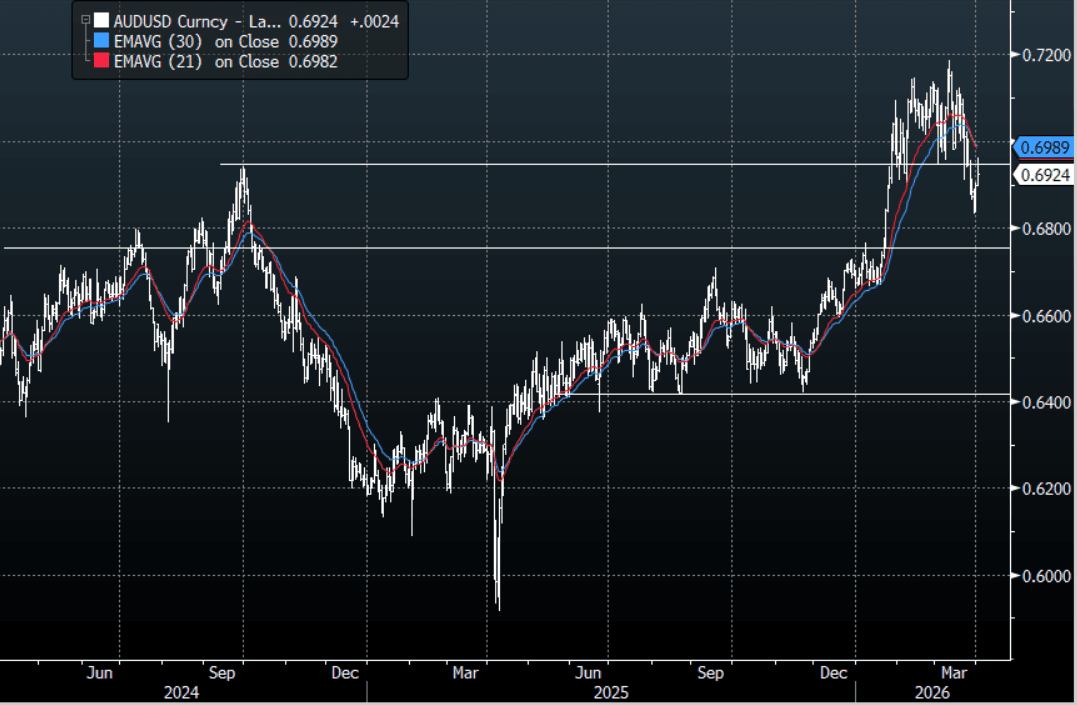

AUD: AUD/USD - Stalls Around 0.6950 As Markets Awaits Trump

The AUD/USD had a range overnight of 0.6903-0.6962, Asia is currently trading around 0.6925. The AUD extended its bounce overnight, finally running into sellers around the 0.6950 area. The market will be waiting for Trump’s speech now to get any further clarity on what they hope is an early end to the conflict. Comments from Trump earlier today that he’ll only consider a halt to attacks on Iran when the Strait of Hormuz is reopened do not bode well. Nor the fact that the Pentagon is moving a large number of the A-10, a close-air support plane that could be used to help U.S. ground forces seize territory near the Strait of Hormuz as per the NYT. On the day, any hint of a ceasefire would see this relief rally have another leg higher but I err on the side of more disappointment for now. The first resistance is around the overnight highs 0.6950-0.6970 and then the more important 0.7050 area. Initial support on the day is toward the 0.6875-0.6900 area while the market looks for a clear path to an off-ramp it is likely to tread water for now.

- “Anthony Albanese is set to announce A$1 billion ($700 million) in interest-free loans for Australian businesses hit by soaring energy costs.” -BBG

- “Compared with Liberation Day, AUD has been more resilient this time round as the market’s belief in a swift-ish resolution of the crisis and the terms-of-trade dynamics are shielding the AUD. However, the domestic labor market and cyclical data have started to weaken in Australia; and should the energy crisis persist for longer, AUD will almost certainly come under pressure as global growth would sour” wrote TS Lombard.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6800(AUD1.17b), 0.6900(AUD1.14b), 0.7025(AUD740m). Upcoming Close Strikes : 0.6800(AUD981m April 7), 0.7000(AUD1.22b April 7), 0.7200(AUD933m April 7) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 76 Points

- Data/Event: Trade Balance

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BOC: March Deliberations Show No Rush To Judgment, Inflation Concern Limited

The Bank of Canada's March meeting deliberations out Wednesday don't offer much of a tilt toward the next move being either a hike or a cut. If anything they suggested that concerns on Governing Council were not widespread over the inflationary implications of the Middle East war-related energy shock. There was no discernable market reaction to the release of the deliberations, with OIS continuing to imply around 45bp of hikes by the end of 2026.

- Discussion over the Iran war impact was close to what was conveyed with the meeting communications - namely, that there were mixed risks to growth and upside risks to inflation but it was too soon and too uncertain to draw any conclusions: "Because Canada is a net energy exporter, higher oil prices would increase export revenues, raise incomes and thereby support GDP. However, higher gasoline prices could restrain consumer spending and add costs for many businesses. The impacts on the economy and inflation would also depend on how the exchange rate responded to the change in oil prices and on financial conditions. Members agreed that these effects could shift the composition of growth. But it was too early to assess their net impact on the growth outlook given the acute uncertainty surrounding the duration and scope of the conflict in Iran."

- They pointed to lingering risks from other ongoing crises too: "The war in Iran had clearly added a new layer of uncertainty, but they agreed that they should not lose sight of the other risks already facing the economy: shifting US trade policy, the upcoming review of the Canada-United States-Mexico Agreement, and ongoing structural changes. With no indication of whether the Middle East conflict would end quickly or persist for some time, members agreed that it was too early to discern the net impact from the combination of these forces. "

- Overall, while policymakers "agreed it would be important to communicate to Canadians that they would look through the immediate effect on inflation of the oil price shock. But they would respond, if needed, to ensure that price increases did not spread to other goods and services and become persistent inflation", Governing Council sounded relatively relaxed on inflation risks from the war given the circumstances.

- "One perspective emphasized that the near-term increase in total inflation would raise inflation risks over the projection horizon" in part via the danger of higher inflation expectations. But that appeared to be a minority opinion: "Members also noted, however, that beyond the short run, the impact of higher energy prices on ongoing inflation could be limited" because "the economy was starting from a position of excess supply...Typically, higher inflation expectations make it easier for businesses to pass along cost increases. But when the economy is soft, firms often look for ways to avoid raising prices so that they don’t lose customers. Similarly, upward pressure on wages is less likely in a weak economy."

- Overall, "they agreed that, in the near term, risks to growth looked tilted to the downside while the oil price shock represented additional upside risk to inflation."

- On how to deal with the nascent supply shock, "inflationary pressures from higher energy prices were expected to push inflation above target with the economy in excess supply. This presents a difficult trade-off for monetary policy. On the one hand, raising the policy rate to bring down inflation could weaken the economy further. On the other hand, lowering rates to support the economy could risk pushing inflation even higher."

- Members "acknowledged that they would need to rely on judgement more heavily than usual and take a risk management approach to monetary policy. They agreed to keep options open while closely monitoring the unfolding conflict in the Middle East, US trade policy and incoming data. Members agreed that they should be ready to respond as needed as the outlook evolved."

USDCAD TECHS: Bull Cycle Remains In Play

- RES 4: 1.4051 High Nov 28

- RES 3: 1.4015 High Dec 2 ‘25

- RES 2: 1.3985 76.4% retracement of the Nov 5 ‘25 - Jan 30 bear leg

- RES 1: 1.3967 High Mar 31

- PRICE: 1.3886 @ 16:46 BST Apr 1

- SUP 1: 1.3845 Low Mar 27

- SUP 2: 1.3753 High Mar 3 and a recent breakout level

- SUP 3: 1.3670 Low Mar 23 and a key short-term support

- SUP 4: 1.3526 Low Mar 09

A bull cycle in USDCAD remains in play and this week’s extension reinforces current trend conditions. Recent gains have resulted in a break of key resistance at 1.3753, the Mar 3 high, highlighting a short-term reversal. An important resistance at 1.3929, the Jan 16 high, has been pierced. A clear break of this hurdle would open 1.3985, a Fibonacci retracement. Initial firm support to watch lies at 1.3670, the Mar 23 low.