MNI RBA WATCH: Board Eyes 25bp Cash Rate Hike

The Reserve Bank of Australia Board will strongly consider a 25-basis-point hike to the 3.6% cash rate when it meets next Tuesday, in order to contain a recent lift in underlying inflation, but its forecasts and the tone of Governor Michele Bullock’s post-meeting remarks will determine whether the move is a modest adjustment or a signal of further increases ahead.

Q4 inflation data landed too strong for the Bank to ignore, while tight labour market conditions provide scope to raise rates without excessive concern about a sharp rise in unemployment. (See MNI INTERVIEW: Trimmed Mean Key To Feb RBA Hike) A hike next week would mark the RBA’s first increase since November 2023 and its first cash-rate adjustment since it eased by 25bp in August 2025. (See MNI RBA WATCH: Board Sees 2026 Hike Risks, Cuts Ruled Out)

Markets have priced in a 72.6% chance of a hike on Tuesday and see the cash rate at 4.10% by December.

ECONOMIC DATA

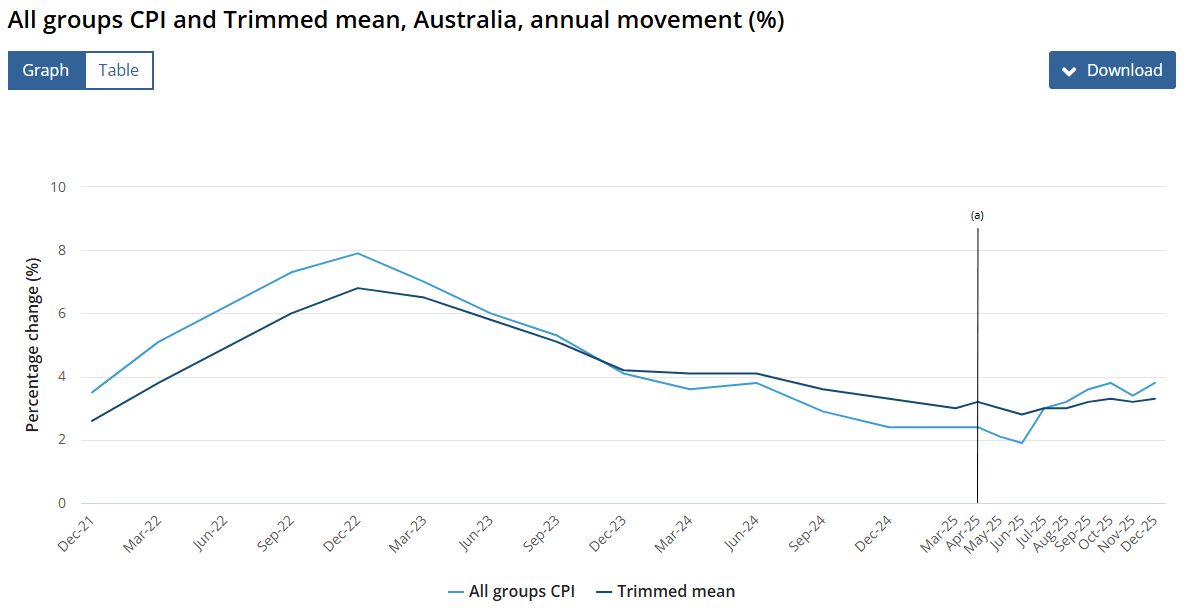

Trimmed-mean inflation, the RBA's preferred gauge, was 0.9% q/q in Q4, taking the annual pace to 3.4% y/y, 20bp above market expectations and higher than the 3.2% forecast in the RBA’s most recent Statement on Monetary Policy. The firmer-than-expected outcome, up 40bp y/y despite falling 10bp over the quarter, will add pressure on the RBA to hike the cash rate.

Headline monthly inflation was 1.0% m/m in December, taking the annual pace to 3.8%, though the RBA continues to place greater weight on the quarterly trimmed mean as its benchmark measure. (See chart)

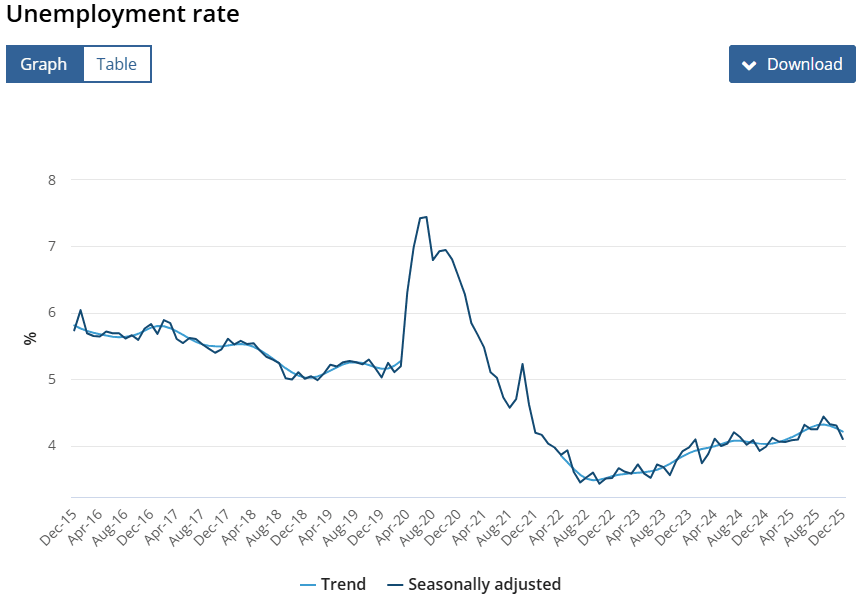

Australia’s unemployment rate also fell to 4.1% in December, 20bp below expectations and down from November, while employment rose by 65,000, well above expectations for a 27,000 gain, driven by a 55,000 increase in full-time jobs. The stronger labour data will will provide the Board additional cover for a hike.

FORECASTS & TONE

A shift in tone would mark a sharp turnaround from Bullock’s “mission accomplished” messaging in mid-2025 and an implicit acknowledgement that inflation pressures have not yet been fully contained.

Failure to act decisively also risks undermining inflation expectations, which underpin the RBA’s relatively optimistic forecasts, former RBA research chief John Simon recently told MNI.

“With inflation above target for such a long time, credibility becomes more tenuous,” he said, noting the rate may ultimately need to move above 4%. A hike next week without a corresponding upgrade to the RBA’s forecasts — which currently show inflation returning below 3% by mid-2027 — would amount to a dovish tilt. By contrast, a hike accompanied by a faster projected return to target would signal a more hawkish stance, opening the door to further rate increases through 2026.

HOLD CASE

However, one academic believes the RBA is likely to hold, arguing the Bank targets inflation over a longer horizon and has repeatedly shown a high tolerance for price growth above target. The RBA has already demonstrated a willingness to tolerate inflation above the 2–3% band, and even a 50-basis-point rise in the Q4 trimmed-mean measure to around 3.5% would likely be insufficient to prompt a rate hike at the Feb 3 meeting, said Mark Wooden, emeritus professor at the University of Melbourne’s Melbourne Institute. He added that political pressure to avoid further rate increases also plays a role in the Bank’s thinking.