MNI: March RBA Hike Risk Rises - Ex Staffers

The Reserve Bank of Australia will likely need to lift the 3.85% cash rate by a further 50-75 basis points, with a hike next week gaining in likelihood, former staffers told MNI, noting the Bank’s “narrow path” strategy had failed to contain inflation.

“The RBA made a choice about strategy and that strategy hasn't panned out,” said Martin Eftimoski, an RBA economist from 2017 to 2021, noting the Iran conflict will exacerbate inflation that is already above the Bank’s 2-3% target band. “And now they're locked into probably 50-75bp increases from here. Australia is in a potentially very bad spot. We're actually at risk, in the medium term, of unanchored inflationary expectations.”

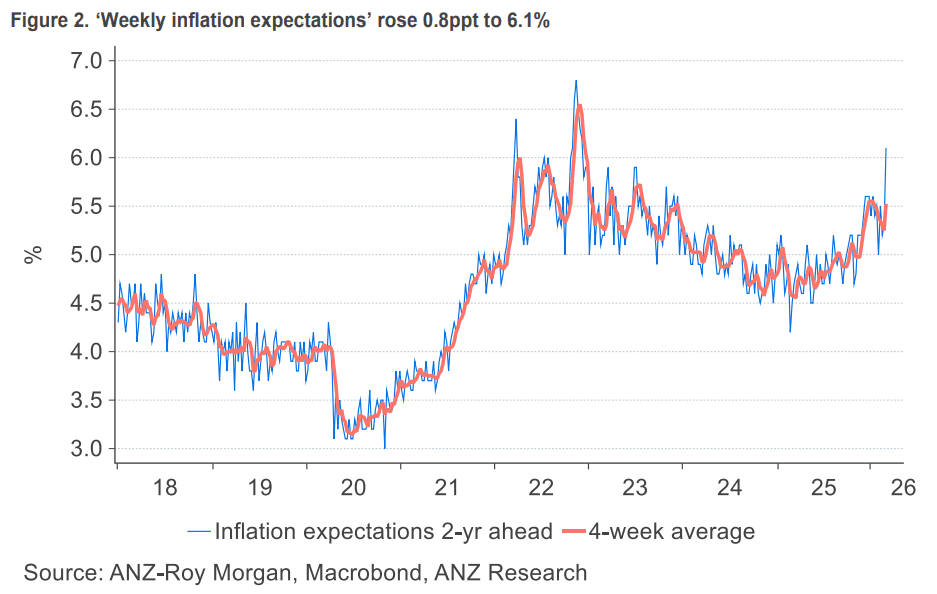

Hidden PDF Tuesday showed inflation expectations jumping 0.8 percentage points to 6.1%, a three-year high. (See chart)

The increase preceded comments by Deputy Governor Andrew Hauser, who warned that the jump in oil prices could push inflation above the 4.2% forecast and that keeping interest rates too low risks fuelling a damaging rise in inflation expectations.

Peter Tulip, chief economist at the Centre for Independent Studies and a former senior RBA official, said recent commentary from the RBA is being taken as a signal that rates will probably rise at the next meeting. "I think that’s good. But the case for tightening was strong before the recent rise in oil prices," he noted.

Markets now see a 60% chance of a hike next week, up 30 percentage points since Hauser's comments.

"My guess is that the current outlook would justify a fairly prompt increase of about 75bp, to 4.6%, staying there for a few quarters, then gradually easing once we’ve seen inflation and unemployment moving back towards their targets," Tulip continued, warning that the RBA typically moves more slowly than it should. "Which means it has to do more. So a more gradual increase of about 1 percentage point is more likely."

Eftimoski cautioned the Bank could still choose to space out hikes following February’s 25bp increase to avoid overdoing it. “The global macroeconomic situation is so uncertain. There are upside inflationary risks and downside growth risks. A lot of this could be temporary, but that kind of misled them last time during the transitory versus persistent debate. I find this particular rate call incredibly hard to think about."

FAILED STRATEGY

Eftimoski said the RBA’s narrow path strategy, which aimed to protect employment gains at the expense of a lower cash rate and slower return to target, directly contributed to the current reflation.

“Many other central banks are watching Australia as an experiment. The trajectory here is different, and other central banks are taking note of our alternate path,” he said.

“If oil prices stay at USD120–130 [per barrel] for months on end, we could face a serious inflation breakout. But the war just started, and oil prices are highly volatile. The only thing that’s certain is ongoing uncertainty. For now, the RBA might look through current oil prices.”

He said the RBA should answer three key questions to help markets gauge its reaction function. “First, are you treating this inflationary shock as transitory or permanent? That’s the number one question,” he noted. “Second, what’s your view on global macro risks? Are you worried about a U.S. recession, developments in China, or the lack of Chinese stimulus? That will heavily influence whether the shock is considered transitory. Third, how broad is the domestic recovery in Australia?”

Answering these questions would provide insight into the RBA’s likely trajectory over 2026, including how reactive it may be to the geopolitical crisis and other global developments, he continued, adding the Bank may not have a definitive, or settled internal view.