MNI Fed Preview-September 2025: A Reluctant Return To Easing

Sep-12 21:15By: Tim Cooper

US+ 1

Download Full Report Here

- The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%.

- The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”.

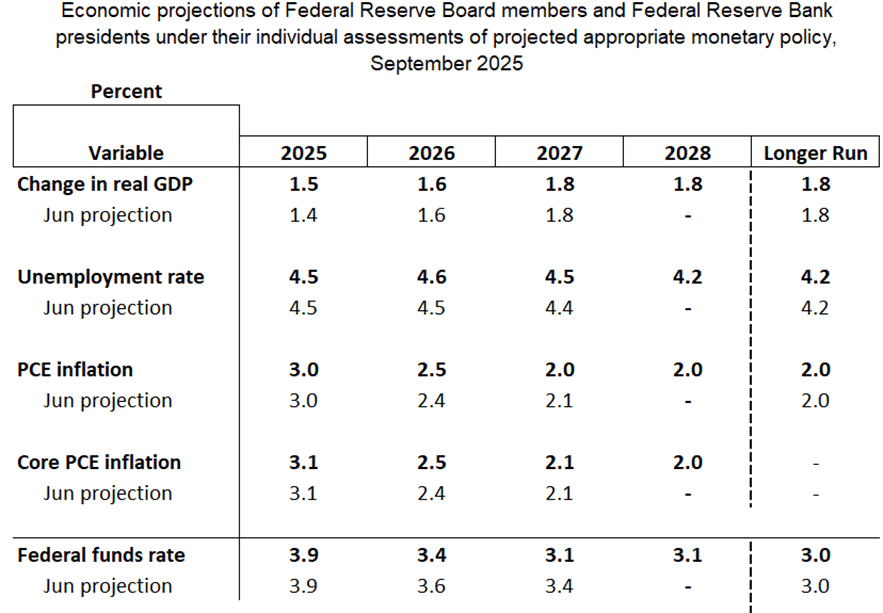

- The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- The Statement will downgrade the description of the labor market to reflect a rise in the unemployment rate and poor payrolls growth, and is likely to include at least one dissent to the rate decision.

- But with a Committee that is fairly divided on the way forward, Powell will be noncommittal on future action, reiterating that policy is not on a preset course, and upcoming decisions will be data-dependent.

- A key undercurrent is an increasingly activist approach to Fed personnel management from the White House, which leaves the composition of the FOMC uncertain not just over the medium-term but also at this meeting.

MNI’s separate preview of sell-side analyst summaries to follow on Monday Sep 15

Trending Top

Mar-27 20:13