MNI EUROPEAN OPEN: RBA Leaves Cash Rate At 3.60%

EXECUTIVE SUMMARY

- THE RESERVE BANK OF AUSTRALIA LEAVES THE CASH RATE AT 3.60% - MNI

- TRUMP GIVES PERMISSION FOR NVIDIA TO SHIP TO CHINA - BBG

- US THREATENS MEXICO WITH FURTHER TARIFFS - BBG

- DEAL TO RELEASE FROZEN RUSSIAN ASSETS CLOSE - TIMES

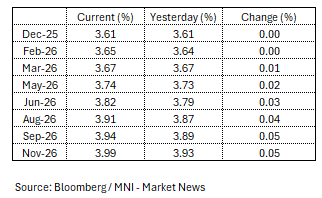

Fig 1: RBA -Dated OIS

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

MNI INTERVIEW: Inflation Expectations Resisted BOE Hikes-Weale. Firms' price increase expectations during the post-COVID inflationary period were not significantly affected by UK monetary policy shocks which saw Bank Rate climb from 0.1% to 5.25%, according to new research by ex-Monetary Policy Committee member Martin Weale, with the findings suggesting a de-anchoring from target.

UKRAINE (TIMES): “A deal to release up to £100 billion of frozen Russian assets in Europe to aid Ukraine is just days away, Sir Keir Starmer believes, as he said negotiations to end the war had reached a “critical stage”.”

POLITICS (POLITICO): “U.K. police will investigate allegations Reform UK breached spending rules in last year’s general election campaign.”

POLITICS (TIMES): “Angela Rayner has blamed “vested interests” for attempts to delay Labour’s workers’ rights reforms and urged ministers not to “blink or buckle” in the face of opposition. The Employment Rights Bill returned to the Commons on Monday after the government watered down its manifesto pledge plans to give workers legal protections from day one.”

EU

ECB (MNI): “The European Central Bank has invited the Italian government to reconsider a revised draft of the 2026 budget law, “concerning the management of reserves must be construed as meaning that the gold reserves managed and held by the Banca d’Italia, as recorded on its balance sheet, belong to the Italian people”.”

FRANCE (LOCAL FRANCE): “On Tuesday MPs in the Assemblée nationale will vote on the first part of the budget - the (Sécu) social security spending. If Prime Minister Sébastien Lecornu fails to achieve a majority, there is virtually no chance of getting the budget passed by the normal routes.”

UKRAINE (POLITICO): “Ukrainian President Volodymyr Zelenskyy said Monday his country will not make territorial concessions to Russia as the Trump administration looks to broker a peace deal between the two countries.”

UKRAINE (BBC): “In London, Zelensky held talks with Prime Minister Sir Keir Starmer, French President Emmanuel Macron and the German Chancellor Friedrich Merz.”

US

MNI FED WATCH: 3rd Risk-Management Cut, Then Easing Bar Rises. The Federal Reserve is expected Wednesday to lower its overnight benchmark rate for a third straight meeting to 3.50%-3.75% but with dwindling support for continued easing, the bar moves higher on further cuts next year.

MNI: NY FED - Inflation Expectations Steady, Consumers Gloomy. U.S. consumers inflation expectations in November were steady across time horizons, according to a Federal Reserve Bank of New York report Monday, while consumers' perceptions and expectations about their current and future financial situation became more negative.

US CHINA RELATIONS (BBG): “President Donald Trump granted Nvidia Corp. permission to ship its H200 artificial intelligence chip to China in exchange for a 25% surcharge, a move that lets the world’s most valuable company potentially regain billions of dollars in lost business from a key global market.”

US COURT RULING (BBG):”President Donald Trump’s executive order directing government agencies to halt approving new wind energy projects was ruled illegal by a federal judge. The ruling Monday sided with more than a dozen states and a New York clean energy group that had challenged the executive order that essentially froze US approvals of wind energy developments pending a review. “

US AGRICULTURE (BBG): “US growers say the Trump administration’s $12 billion aid package brings temporary relief, but is unlikely to kickstart a lasting recovery for the American farm economy.”

TARIFFS (BBG): “President Donald Trump threatened to impose an additional 5% tariff on imports from Mexico if the country did not release water that his administration says must be allowed to flow under a treaty.”

JAPAN

UKRAINE (POLITICO): “Japan has rebuffed the EU’s offer to join its plan to use frozen Russian state assets to fund Ukraine — dashing the bloc's hopes of securing global support for the initiative.”

OTHER

AUSTRALIA (MNI): RBA Leaves Cash Rate at 3.6%

SOUTH KOREA (YONHAP): “ The finance ministry is working to set up a task force charged with devising measures to respond to the weakening local currency, in cooperation with exporters, securities firms and relevant authorities, officials said Tuesday.”

CHINA

MNI China Press Digest Dec 9: Politburo, Car Sales, Exports

MNI: PBOC Net Drains CNY39 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY117.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY39.0 billion after offsetting maturities of CNY156.3 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4219% at 09:53 am local time from the close of 1.4459% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Monday, the same as the close on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.0773 Tues; +2.98% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0773 on Tuesday, compared with 7.0764 set on Monday. The fixing was estimated at 7.0764 by Bloomberg survey today.

MNI: China CFETS Yuan Index Down 0.27% In Week of Dec 5

The CFETS Weekly RMB Index was 97.65 on Dec 5, down 0.27% from 97.92 on Nov 28.

The gauge, which compares the yuan to a basket of currencies from China's 24 major trading partners, has decreased 3.76% this year, when compares with 101.47 on Dec. 31, 2024.

MARKET DATA

AUSTRALIA NAB BUSINESS CONFIDENCE NOVEMBER 1, PRIOR 6

AUSTRALIA NAB BUSINESS CONDITIONS NOVEMBER 7, PRIOR 10 (REVISED UP)

AUSTRALIA RBA CASH RATE TARGET 3.60%, EST 3.60%, PRIOR 3.60%

JAPAN MONEY STOCK M2 YOY NOVEMBER 1.8%, PRIOR 1.6%

JAPAN MONEY STOCK M3 YOY NOVEMBER 1.2%, PRIOR 1.1%

MARKETS

US TSYS: Yields Trend Higher in Afternoon Trade

Bond futures turned down in the afternoon with the US-10-Yr falling to 112-06. Having traded up at 112-11 it lost ground in the afternoon session. TYH6 is at the mid-point between the 100-day EMA of 112-14+ and the 200-day EMA of 111-29+.

Cash was weak with yields up to +1.3bps higher in the mid-part of the curve.

- The 2-Yr is up +0.9bps at 3.586%

- The 5-Yr is up 1.2bps at 3.76%

- The 10-Yr is up 1.2bps at 4.178%

- The 30-Yr is up +1.0bps at 4.813%

The 10-Yr remains in the 4.00% -4.20% range that has held in recent weeks. A more hawkish outlook from the FED could see new ranges established, particularly for the 10-yr.

Tuesday Data Calendar in the US: ADP Weekly, Redbook and JOLTS for Sep/Oct; Treasury auctions include $39B 10Y note reopen.

Tonight sees a US$75bn 6-week bill auction and a US$39bn 10-Yr auction.

AUSSIE BONDS: Market Cheapens During RBA Governor Presser

ACGBs (YM -11.0, XM -6.5) cheapened sharply during Governor Bullock’s post-meeting press conference. While markets initially took the decision and accompanying statement in stride, her comments were interpreted as distinctly more hawkish, prompting a swift repricing

- Bullock signalled that inflation risks have shifted to the upside, with recent data suggesting more economic tightness than previously thought. The RBA is cautious about over-interpreting the new monthly CPI but is alert to any broad-based pickup in inflation.

- The Board did not consider rate cuts and does not expect them in the foreseeable future.

- Overall, downside risks have faded and upside risks have grown. The policy debate is now between an extended pause or potential hikes, with the Board uncomfortable about current inflation and guided strictly by incoming data.

- Cash ACGBs are 6-11bps cheaper, with the AU-US 10-year yield differential at +58bps.

- The bills strip has bear-steepened, with pricing -2 to -13.

- RBA-dated OIS pricing is 1-8bps firmer versus pre-decision levels. Tightening expectations are seen across all meetings, with the probability of a 25bp hike rising from 28% for February to 119% by June and 190% by December 2026.

- Tomorrow, the local calendar will be empty.

source: Bloomberg Finance LP /MNI

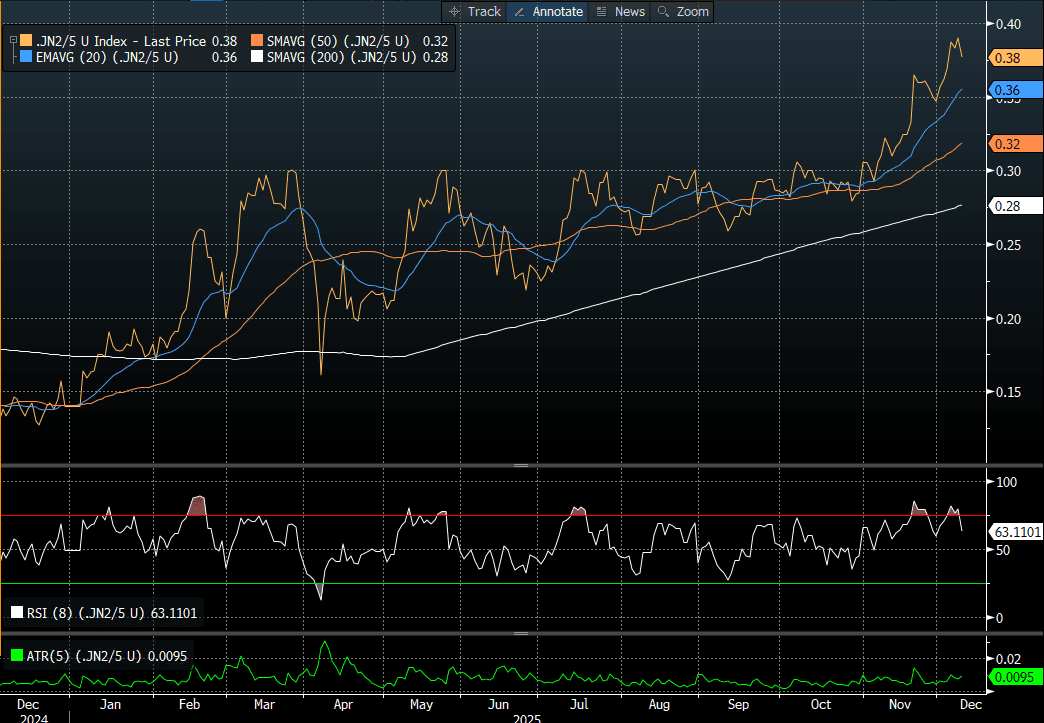

JGBS: Little Reaction To 5Y Auction, 2/5 Curve At Steepest Since 2009

JGB futures are stronger, +10 compared to settlement levels, after dealing in a narrow range in today’s session.

- Today’s 5-year JGB auction delivered lacklustre demand signals. The low price was slightly below expectations at 99.81, the bid-to-cover ratio fell to 3.1676x from 3.3258x, and the tail widened to 0.04 from 0.03.

- The result contrasts with the strong results seen at this month’s 10-year and 30-year auctions, but is consistent with last month’s poor 2-year auction.

- Ahead of that 2-year auction, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance is expected to rise by around 100bn each for the 2-year and 5-year tenors. Reuters also noted that there are no changes to the planned issuance for 10-40-year tenors.

- Cash US tsys are slightly cheaper in today's Asia-Pac session.

- Cash JGBs are flat to 1.7bps lower across benchmarks, with the 5-year leading.

- Nonetheless, the 2s/5s curve is holding near its cycle high of 39bps, the steepest since late 2009 (see chart).

- Swap rates are flat to slightly higher, with a flattening bias.

- Tomorrow, the local calendar will see PPI data.

Source: Bloomberg Finance LP/ MNI

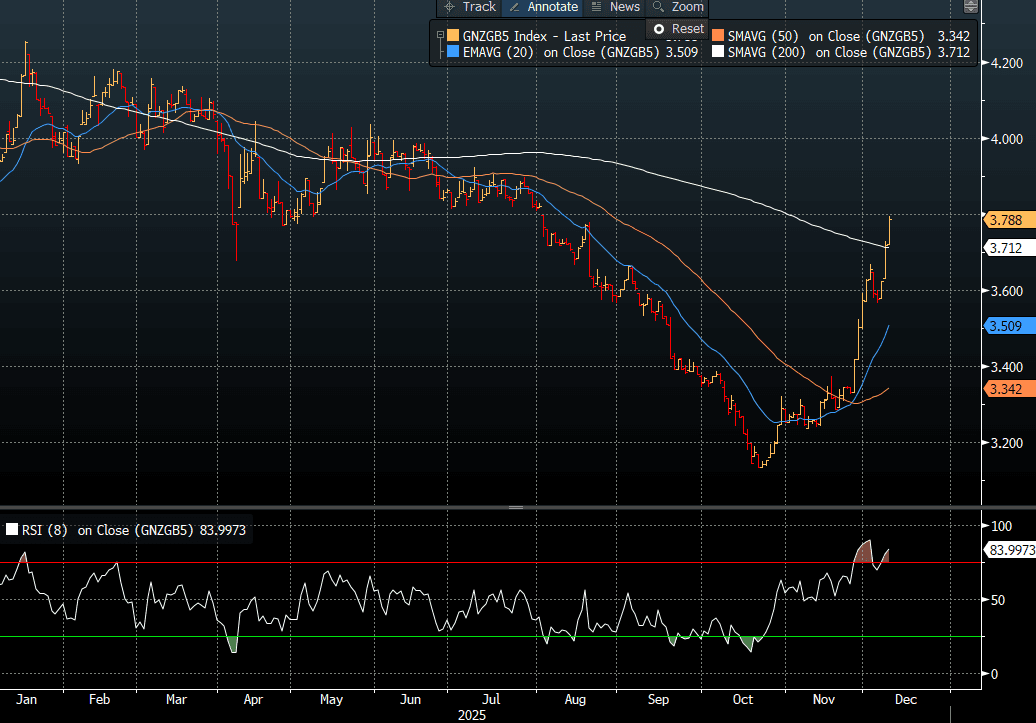

BONDS: NZGBS: Post-RBNZ Sell-Off Keeps Extending, 5YY Up +45bps

NZGB benchmark yields closed 6-7bps higher, but slightly below session highs (see chart).

- On a relative basis versus the $-bloc, NZGBs also had a heavy session, with the NZ-US and NZ-AU 10-year yield differentials 2-3bps higher. However, it is worth noting that the RBA decision was delivered with the local market closed. Accordingly, any market reaction will be reflected in tomorrow’s open. That said, at this stage, the reaction has been muted, with the RBA noting that inflation risks have shifted higher and that it wanted more time to judge how persistent these pressures are.

- (Bloomberg) “Westpac New Zealand is raising interest rates on fixed-term home loans of two years or longer. Effective Wednesday, a two-year special home loan will carry a 4.75% rate up from 4.45%.”

- Swap rates closed 4-6bps higher, with the 2s10s curve flatter.

- RBNZ-dated OIS pricing closed flat to 11bps firmer across meetings. No change is priced for February, while November 2026 assigns 56bps of tightening.

- Tomorrow, the local calendar will see RBNZ Governor Breman host a media Q+A alongside Net Migration data.

- On Thursday, the NZ Treasury plans to sell NZ$175mn of the 4.50% May-30 bond, NZ$200mn of the 3.50% Apr-33 bond and NZ$75mn of the 5.00% May-54 bond.

source: Bloomberg Finance LP / MNI

FOREX: USD - BBDXY Consolidates Overnight Gains

The BBDXY has had a range today of 1213.40 - 1214.57 in the Asia-Pac session; it is currently trading around 1213, -0.05%. The USD has traded sideways in a quiet Asian session. US yields continued to extend higher as we approach the FOMC, and overnight both risk and the USD started to react. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1219-1222. Support remains toward 1210 which needs to be worked through and then the more important 1205 area.

- EUR/USD - Asian range 1.1635-1.1649, Asia is currently trading 1.1645. The pair continues to consolidate around the 1.1650 area. On the day it looks like dips back toward 1.1580-1600 should be supported initially, looking to retest the 1.1680 area again eventually.

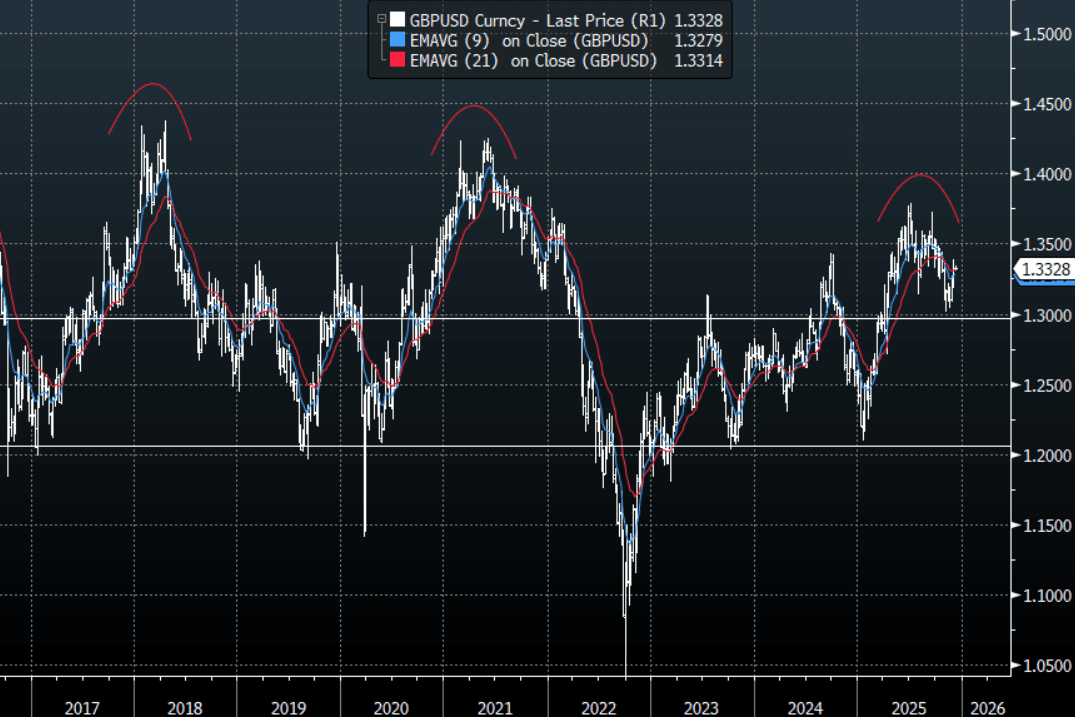

- GBP/USD - Asian range 1.3319-1.3335, Asia is currently dealing around 1.3330. The pair is consolidating on a 1.33 handle. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3260-1.3290 area, while above here look for the market to test the 1.3370-90 area again at some point.

- Cross asset : SPX +0.10%, Gold $4195, US 10-Year 4.166%, BBDXY 1213, Crude Oil $58.75

- Data/Events : Germany Trade Balance SA

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

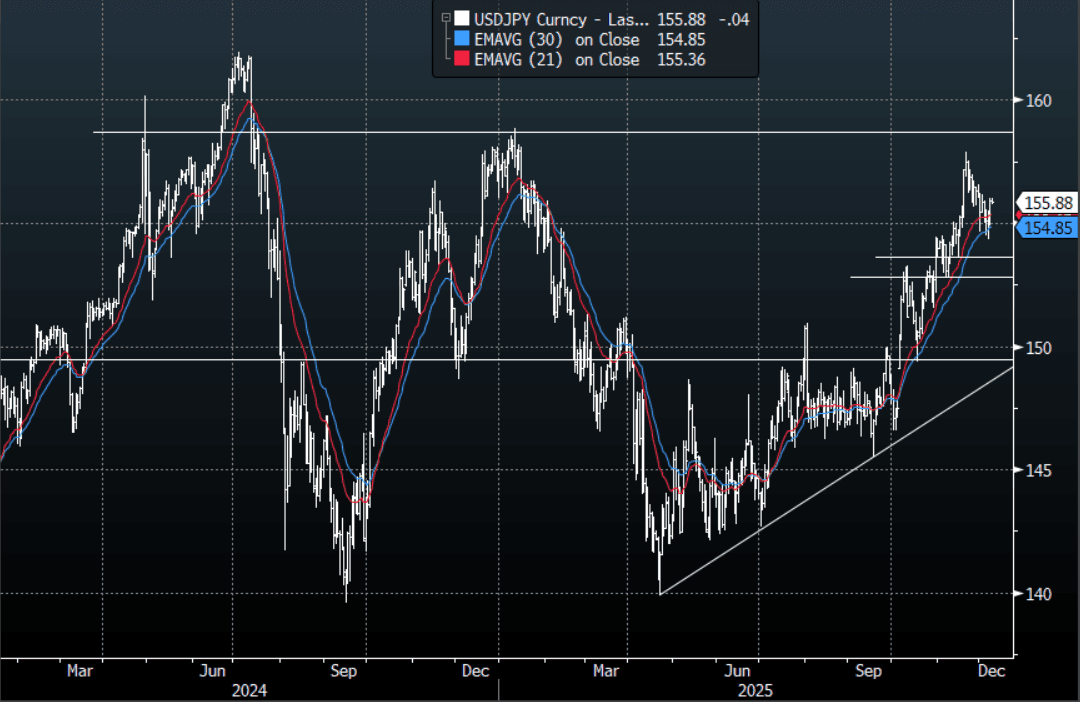

JPY: USD/JPY - Largely Unchanged, Consolidating Below 156.00

The USD/JPY range today has been 155.74 - 156.04 in the Asia-Pac session, it is currently trading around 155.90, +0.05%. The pair has traded sideways with little direction in a quiet session. The move overnight was supported by the sell-off in treasuries which has seen US yields move quite a bit higher as we approach the FOMC. The market is pricing in the fact that the Yen move looks likely to force the BOJ into action in December. This has stalled the upward momentum for the moment and could keep it contained in the short-term but I suspect the market will still look for opportunities to express a long USD at the right levels. Technically USD/JPY is still in an uptrend, the first big support back toward the 153-155 area has held on very well upon first examination. On the day, the market will be watching to see if there is any follow-through on this constructive price action. First support on the day is back toward 155.30-50, looking for a test of 156.20-40, a break of which would open up a move back to the 157.00 area.

- Bloomberg - “Foreign investors now dominate Japan’s $7.4 trillion government bond market, accounting for roughly 65% of monthly transactions, up from 12% in 2009. The BOJ’s retreat, coupled with PM Sanae Takaichi’s spending plans, have driven yields to multi-decade highs, sparking concerns of market volatility.”

- "AKAZAWA: SEE NO PARTICULAR CHANGE IN CHINA RARE EARTH CONTROLS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($589m), 157.00($425m). Upcoming Close Strikes : 155.00($1.1b Dec 12), 156.00($1.77b Dec 11), 159.00($1.4b Dec 12) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 91 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

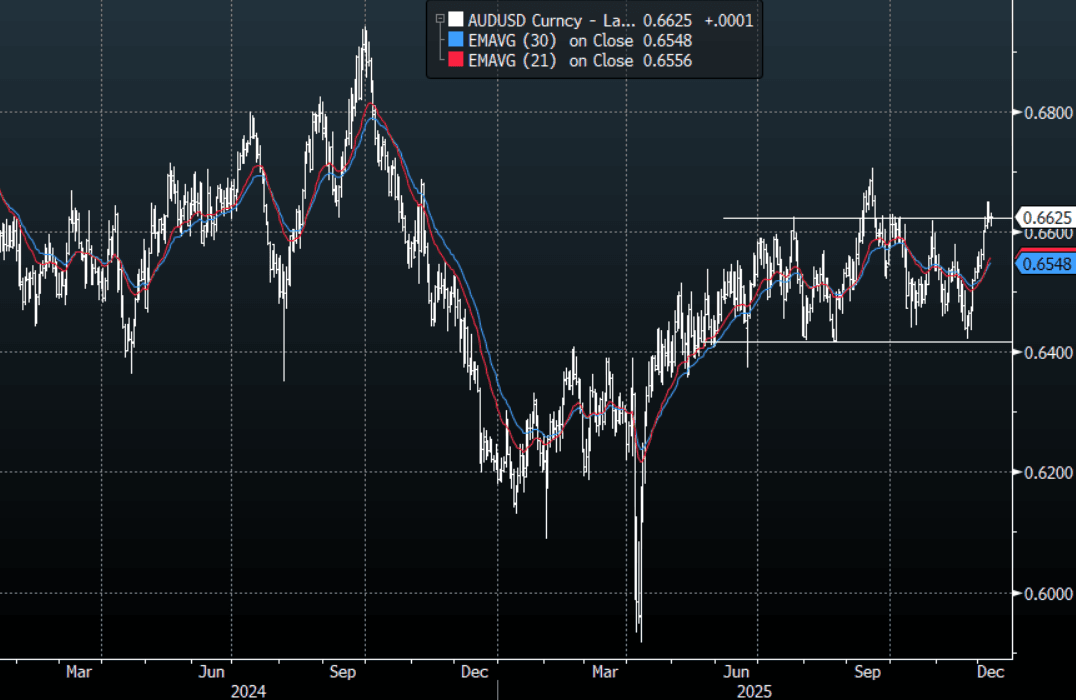

AUD/USD-Holding Above 0.6600, Market Hoping Press Briefing More Hawkish

The AUD/USD has had a range today of 0.6609 - 0.6631 in the Asia- Pac session, it is currently trading around 0.6625, +0.02%. The AUD/USD tried lower on the RBA as the market was looking for something more to confirm their hawkish skew, this added to the headwinds from the pullback in the USD overnight. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. On the day attention will now turn to the press conference where the hawkish tilt the market was looking for could still be expressed. It has come a long way very quickly so a pullback is not out of the question if the market does not get any love from the press conference, first support is toward 0.6570/90 where we should see demand reappear. Ultimately the AUD is looking to rebuild momentum to have another look back toward the 0.6700 area at some point.

- MNI AU - RBA: Rates On Hold, Upside Risks To Inflation Indicated. The RBA left rates at 3.6% at its December decision but noted that risks to inflation are tilted to the upside. The labour market remains “a little tight” and the private domestic economic momentum stronger.

- MNI AU - Q4 Conditions Up On Q3, Q4 Business Inflation Series Moderate: November NAB business conditions moderated to 7 from an upwardly-revised 10, while the more volatile confidence fell to 1 from 6, the lowest since April. Conditions remained in line with Q3 outcomes and at this stage looks like normalisation rather than slowing as the sharp rise in WA in October unwound. With hard data showing a pickup in domestic demand and inflation above the top of the RBA’s 2-3% band.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6630(AUD621m), 0.6635(AUD714m). Upcoming Close Strikes : 0.6550(AUD1.59b Dec 11) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

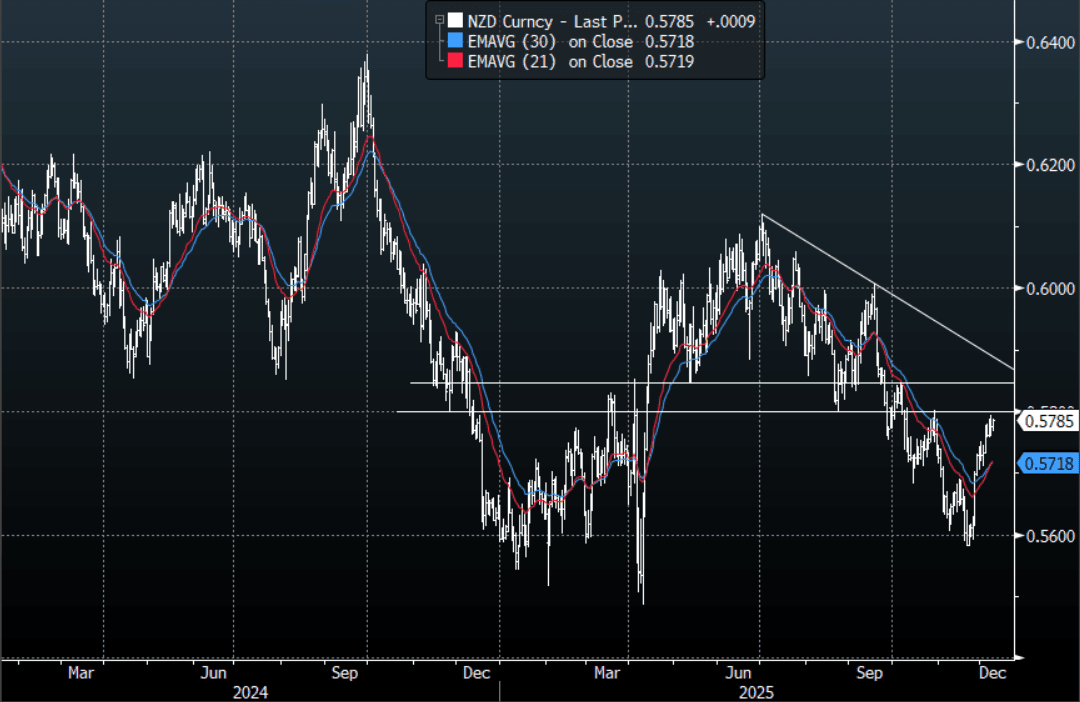

NZD/USD - A Little Higher Looking To Test 0.5800 Again

The NZD/USD had a range today of 0.5767-0.5788 in the Asia-Pac session, going into the London open trading around 0.5785, +0.15%. The NZD/USD has drifted a little higher having a look back toward the 0.5800 area once again in our session. On the day, watch the price action back toward 0.5780-0.5800 if price cannot retake the highs we could see a potential reversion back to the mean. Support is around 0.5735-0.5755 area first up and then the more important 0.5670/0.5700 area. Some tough resistance approaching in the 0.5800-0.5850 area, I suspect sellers could fade a move here initially.

- Bloomberg - “Westpac New Zealand is raising interest rates on fixed-term home loans of two years or longer, the lender says in an emailed statement. Effective Wednesday, a two-year special home loan will carry a 4.75% rate up from 4.45%. Five-year special rate rises to 5.29% from 4.49%. Says fixed rates are mainly driven by movements in wholesale interest rates rather than the OCR and wholesale rates have lifted materially.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD557m Dec 10), 0.5700(NZD306m Dec 12) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 33 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

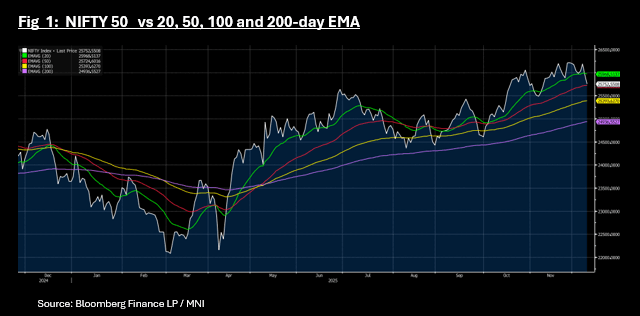

ASIA STOCKS: FOMC Stalls Markets, NIFTY 50 Through Key Tech Level

A generally weak day for Asia's equity markets today with the biggest falls from Hong Kong and India. As the world awaits the FOMC decision on rates, attention turns to the forward guidance as the markets are now set for a December cut. The pathway for rates in 2026 has become less certain now with investors set to pour over every part of the FOMC output. This uncertainty has given rise to profit taking / de-risking ahead of the FOMC. Even the tech sector took a breather today with key names like SK Hynix in Korea and TSMC in Taiwan falling. In Japan, expectations of a potential interest-rate hike have pushed up bond yields and strengthened the yen , which tends to weigh on export competitiveness and investor sentiment in nearby markets.

- The NIKKEI has managed to stay positive today, gaining by +0.07% whilst the KOSPI fell by -0.36% with key tech stocks lagging.

- China's bourses were heavy with the Hang Seng leading the falls, down -0.85% as other indexes falls were muted in a generally risk off day with some local commentators suggesting that profit taking was evident.

- India's NIFTY 50 finished Monday on the back foot and has started Tuesday with galls of -0.75% to be at 25,758. The falls in recent days has seen the NIFTY trade through the 20-day EMA of 25,968 and is now near the 50-day EMA of 25,724. It last traded below the 50-day EMA in early October.

- The FTSE Malay KLCI is down -0.20% and the Jakarta Composite -0.40% on a generally weak day whilst the SE Thai bucked the trend and rose 0.45%

OIL: Crude In Narrow Range But Holds Losses As Waits For Outlook Updates

Oil has held onto Monday’s losses of just over 2% during today’s APAC trading but has moved in a very narrow range. WTI is down 0.3% to $58.72/bbl after rising to $58.90 earlier, while Brent is 0.2% lower at $62.36/bbl close to the intraday low. With a Ukraine peace deal again looking elusive and Russia likely to continue to find ways around sanctions, the market is focused on the supply outlook with a record market surplus forecast for 2026. Updated projections are published this week.

- The EIA short-term energy outlook is published later today with OPEC & IEA reports on Thursday. The IEA is already projecting a record surplus in 2026 and oil prices are likely to be pressured by an upward revision. OPEC and non-OPEC supply is forecast to grow and recent reports indicated elevated seaborne crude.

- Key risks stem from ongoing Ukrainian attacks on Russian fuel facilities and India succumbing to US pressure to cut its imports of Russian crude which would increase demand for non-sanctioned supplies.

- This week US officials are in India to negotiate a trade deal and its imports of Russian crude will be on the agenda given the US’ punitive 25% tariff due to its purchases. Refiners have signalled that the latest sanctions make it harder to purchase Russian crude.

- US industry-based inventory data are also released Tuesday.

- Later US September/October JOLTS jobs data, September lead index, November NFIB small business sentiment, as well as Germany October trade print. The ECB’s Buch speaks and BoE Board members appear before parliament.

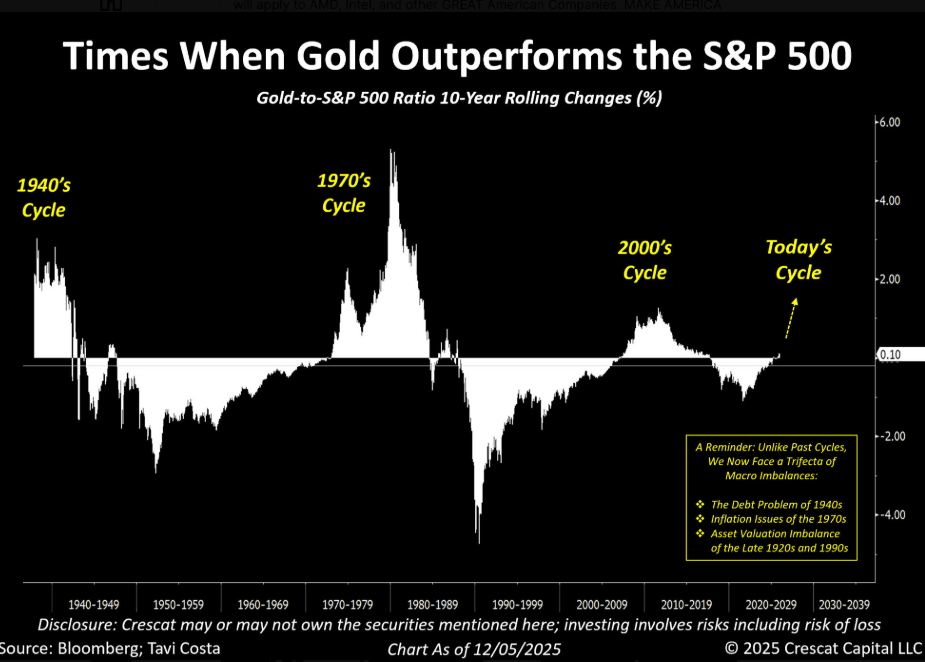

PRECIOUS METALS: Gold - Drifts Lower As The USD Finds A Bid Approaching The FOMC

The range overnight for gold was $4,176.42/oz - $4,217.28/oz, Asia is currently trading around $4,190/oz, +0.05%. Gold slipped lower overnight with the USD rebounding as we approach the FOMC this week. Gold has been chopping around sideways within a $4,140 - $4,260/oz range. The market is trying to regain the momentum to once again test higher but for now it seems to be stalling above $4,200/oz. Support lies back toward the $4,130-$4,150/oz area; a break below here could signal a deeper pullback toward the more important $4,050-$4,100/oz support.

- Otavio Costa of Crescat Capital via X argues the cycle higher is just beginning, “Some argue that gold’s recent outperformance relative to the S&P 500 was a temporary anomaly. I disagree. This dynamic follows very long-term cycles, and I believe we’re likely only in the early stages of this one. A key reminder: Unlike past cycles, however, we now face a trifecta of macro imbalances:”

- “The Debt Problem of the 1940s”

- “Inflation Issues of the 1970s”

- “Asset Valuation Imbalance of the Late 1920s and 1990s”

- The XAU Average True Range(ATR) for the last 10 Trading days: $48.96

Fig 1 : Gold to S&P 500

Source: MNI - Market News/Bloomberg/@TaviCosta

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 09/12/2025 | 0700/0800 | ** | Trade Balance | |

| 09/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 09/12/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 09/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 09/12/2025 | 1415/1415 | BOE Lombardelli, Ramsden, Dhingra, Mann at TSC | ||

| 09/12/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 09/12/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 09/12/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/12/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/12/2025 | - | Bank of Canada Meeting | ||

| 10/12/2025 | 0130/0930 | *** | CPI | |

| 10/12/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/12/2025 | 0700/0800 | *** | CPI Norway | |

| 10/12/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/12/2025 | 0900/1000 | * | Industrial Production | |

| 10/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/12/2025 | 1000/1000 | Chancellor Reeves Testifies at TSC on Budget | ||

| 10/12/2025 | 1045/1045 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 10/12/2025 | 1055/1155 | ECB Lagarde Interview on Currencies/Digital Euro | ||

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI |