MNI EUROPEAN OPEN: Metals Sell-off Continues

EXECUTIVE SUMMARY

- GOLD PLUNGE DEEPENS AS TRADERS UNWIND 'CROWDED' BETS ON RALLY - BBG

- TRUMP SAYS EXPECTS WARSH TO CUT FED RATES - MNI BRIEF

- JAPAN'S TAKAICHI CLARIFIES WEAK YEN REAMRKS FROM ELECTION RALLY - BBG

- XI CALLS FOR YUAN TO BECOME ‘STRONG CURRENCY’: QIUSHI - BBG

- JAN RATING DOG CHINA MFG. PMI RISES TO 50.3 - MNI BRIEF

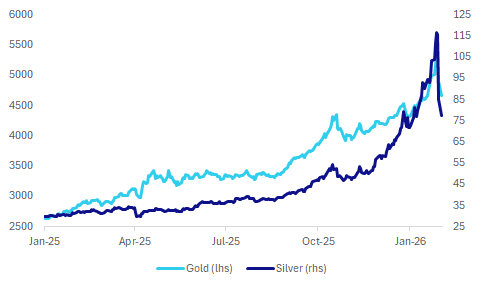

Fig 1: Metals Plunge Continues

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

EU/UK (BBG): "Prime Minister Keir Starmer said he still wants the UK to join the European Union’s flagship €150 billion ($178 billion) defense fund after negotiations last year ended in failure."

EU

BANKING (MNI BRIEF): The next chair of the Paris-based European Banking Authority will be decided by EU diplomats next Wednesday, officials said Friday, with the candidates including former Governor of the Central Bank of Cyprus Constantinos Herodotou and EBA Executive Director Francois-Louis Michaud.

ITALY (BBG): "Italy’s credit rating outlook was raised to positive from stable by S&P Global Ratings, the latest victory for Prime Minister Giorgia Meloni."

US

FED (MNI BRIEF): President Donald Trump Friday said his pick to be the next chair of the Federal Reserve, Kevin Warsh, did not make any promises to lower interest rates, but the president expects the next chair to lower rates.

FED (MNI BRIEF): Federal Reserve Governor Stephen Miran on Friday said interest rates remain too restrictive, but because the fed funds rate is closer to neutral then the central bank can ease rates at a slower pace than his preferred 50 basis point clips months earlier.

FED (MNI): Former Fed officials Friday welcomed the nomination of Kevin Warsh as Federal Reserve Chair, telling MNI he is a seasoned central banker who knows the instituation but he will need to work to persuade the FOMC on his policy ideas and earn the institution's trust as a leader.

FED (MNI BRIEF): Federal Reserve Governor Chris Waller said Friday he dissented in favor of a quarter-point rate cut this week to head off the significant risk of substantial deterioration in the labor market.

POLITICS (RTRS): "A Democratic candidate won a special election for the Texas state senate by a double-digit margin, taking control from Republicans for the first time in decades in a result the losing candidate on Sunday called "a wake-up call" for the midterm elections."

TECH (BBG): "Oracle Corp. plans to raise $45 billion to $50 billion this year through a combination of debt and equity sales to build additional cloud infrastructure capacity, reflecting the scale of financing needed to feed AI’s growth."

JAPAN

BOJ (MNI): Several Bank of Japan board members saw the need to raise the policy interest rate relatively early, with one favouring hikes at intervals of a few months, according to the summary of opinions from the Jan. 22-23 meeting released Monday.

GDP (MNI BRIEF): Japan’s economy is expected to have expanded in the October-December quarter for the first time in two quarters, supported by strong capital spending and public investment, according to forecasts from eight private-sector economists.

FX (BBG): "Japanese Prime Minister Sanae Takaichi sought to clarify her comments about the weak yen, emphasizing that she only intended to argue for a need to create an economy that can withstand currency fluctuations. "

ELECTION (BBG): "Japanese Prime Minister Sanae Takaichi’s public support remains solid while a new opposition alliance is struggling to resonate with voters, opinion polls over the weekend showed, positioning the ruling party for a comfortable majority in the upcoming lower house election."

OTHER

US/IRAN (BBG): “Iran’s supreme leader warned of a “regional war” as tensions continued to mount over potential US strikes on Tehran and top Israeli military officials visited Washington. “

GOLD (BBG): " Gold fell, following its biggest plunge in more than a decade, and silver whipsawed in choppy trading after a dramatic reversal of a record-breaking rally that ran too far, too fast."

INDIA (BBG): "The Indian government’s budget proposal to increase taxes on equity derivatives trading without providing measures to immediately stem foreign outflows is set to pressure domestic shares in the near-term, according to analysts and fund managers."

CHINA

YUAN (BBG): “China needs to build a “strong currency” that can become widely used in international trade, investment and foreign exchange markets and reach the status of a global reserve, according to an article published by Qiushi on Saturday, citing President Xi Jinping’s speech in 2024.”

COMMODITIES (BBG): "In the history of the silver market, prices had traded above $40 an ounce for only a handful of brief periods before last year. On Friday, exhausted traders watched in shock as the precious metal plunged by that much in less than twenty hours."

PMI (MNI BRIEF): China's RatingDog manufacturing PMI, previously known as the Caixin manufacturing PMI, came in at 50.3 in January, up from December's 50.1, remaining in the expansionary zone above the 50 mark, the publisher said on Monday.

PMI (MNI BRIEF): China's Manufacturing Purchasing Managers Index dropped by 0.8 points to 49.3 in January from December, falling below the breakeven 50 mark, mainly due to traditional off-season and insufficient demand, data from the National Bureau of Statistics showed on Saturday.

MNI: PBOC Net Drains CNY75.5 Bln via OMO Monday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY75 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY75.5 billion after offsetting the maturity of CNY150.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4770% at 10:04 am local time from the close of 1.5926% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Friday, compared with the close of 48 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 6.9695 Mon; +4.91% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.9695 on Monday, compared with 6.9678 set on Friday. The fixing was estimated at 6.9718 by Bloomberg survey today.

MNI: China CFETS Yuan Index Down 1.25% In Week of Jan 30

The CFETS Weekly RMB Index was 96.99 on Jan 30, down 1.25% from 98.24 on Jan 23.

MARKET DATA

AUSTRALIA JAN F S&P GLOBAL PMI MFG 52.3; PRIOR 52.4

AUSTRALIA JAN MELBOURNE INSTITUTE INFLAITON Y/Y 3.6%; PRIOR 3.5%

AUSTRALIA JAN ANZ-INDEED JOB ADS M/M 4.4%; PRIOR -0.8%

JAPAN JAN F S&P GLOBAL PMI MFG 51.5; PRIOR 51.5

CHINA JAN RATINGDOG PMI MFG 50.3; MEDIAN 50.0; PRIOR 50.1

MARKETS

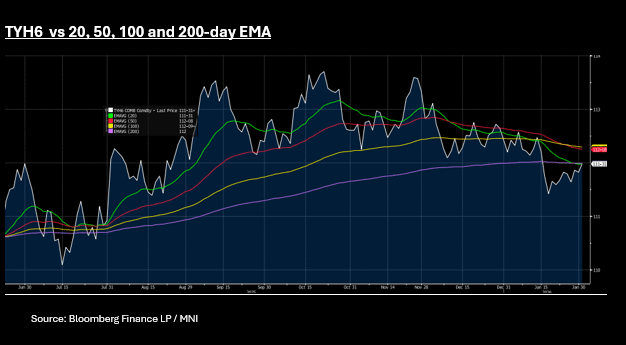

US TSYS: Weak Global Sentiment Builds Case for Lower Yields

US treasury futures trended lower during the morning, but as the afternoon progressed and equities got heavier turned positive. The move lower could be reflective of portfolio re-balancing on account of the huge falls in commodities, but the trend was clear in the afternoon as all major futures turned up. The 10-Yr is up +04+ at 111-31+ and is near to the 20-day EMA of 111-31 and the 200-day EMA of 112. A sustained break above could bring the 50-day EMA into play at 112-08.

Market sentiment continues to be weak with US equity futures pointing to a weak start tonight and could feed into further gains for bonds.

Cash is strong with yields down by -.07bps to -2.0bps with the front end outperforming.

- The 2-Yr is down -2bps 3.506%

- The 5-Yr is down -1.9bps at 3.771%

- The 10-Yr is down -1.6bps at 4.224%

- The 30-Yr is down -0.7bps at 4.867%

The risks are that Warsh's previous comments about rates are the playbook, despite what the White House wants. The uncertainty around a balance sheet unwind will create volatility but for now as risk sentiment weakens, the bias for lower yields seems building.

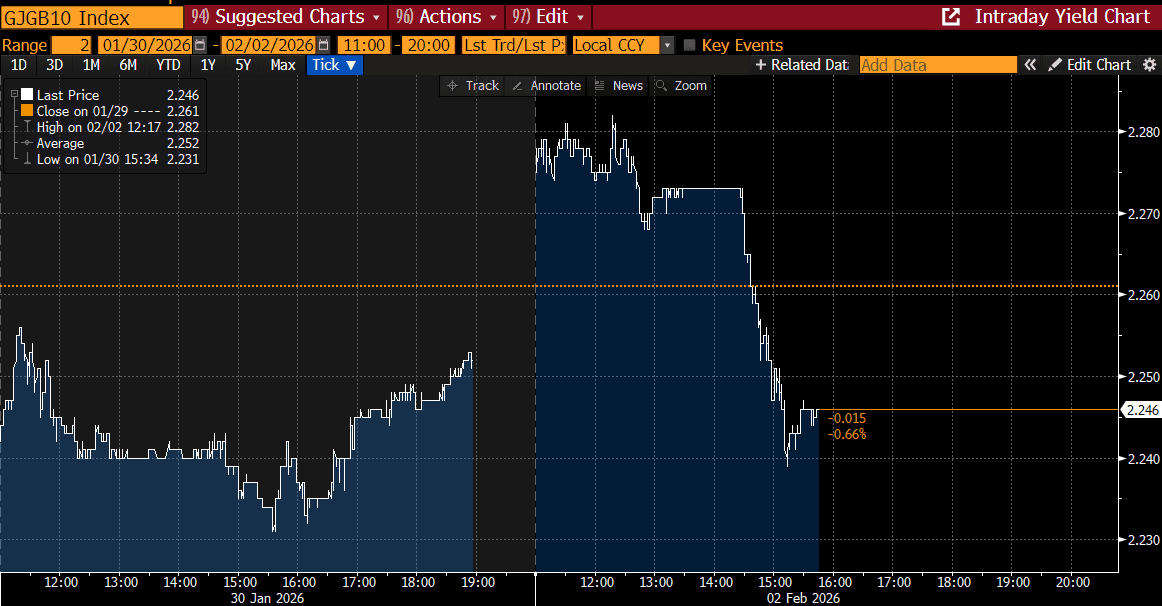

JGBS: Reverse Stronger Amidst Risk-Off Sentiment, 10Y Supply Tomorrow

JGB futures are stronger after reversing early weakness, +6 compared to settlement levels.

- MNI: BOJ Opinions: Early Rate Hikes, Upside Risks to Prices. Several Bank of Japan board members saw the need to raise the policy interest rate relatively early, with one favouring hikes at intervals of a few months, according to the summary of opinions

- Bloomberg - "Japan's ruling bloc is poised to win 300 out of 465 seats in the upcoming election, an Asahi poll showed."

- Cash US tsys are flat to 2bps cheaper, with a steepening bias, in today's Asia-Pac session. US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed's Powell and Warsh ahead. The employment report for January on Friday.

- Cash JGBs have reversed early weakness across benchmarks, with the 10-year yield now 0.7bp lower at 2.245% after the morning’s high of 2.282% amidst risk off sentiment.

- Swap rates are flat to slightly higher, with a flattening bias.

- Tomorrow, the local calendar will see Monetary Base data alongside 10-year supply.

Source: Bloomberg Finance LP

AUSSIE BONDS: Subdued Trading Ahead Of Tomorrow's RBA Policy Decision

ACGBs (YM +1.5 & XM -0.5) are slightly mixed after a relatively subdued start to the trading week.

- Cash US tsys are flat to 2bps richer, with a steepening bias, in today's Asia-Pac session.

- Cash ACGBs are slightly richer with the AU-US 10-year yield differential at +58bps, a few bps below its recent high.

- The bills strip has bull-steepened across contracts, with pricing flat to +2.

- RBA-dated OIS pricing has firmed by around 11–20bps across meetings since the release of December’s stronger-than-expected labour market data on 22 January.

- Last week’s firmer-than-expected Q4 trimmed mean CPI print reinforced the repricing ahead of tomorrow’s RBA policy decision.

- The combination of a resilient labour market and stronger than expected Dec/Q4 inflation has the sell-side consensus expecting an RBA rate hike tomorrow. If delivered, focus will be on how much follow up action the central bank sees as needed to ensure inflation returns to target (see MNI RBA Preview here)

- A 25bp hike tomorrow is priced at a 76% probability, with cumulative tightening probability of 161% by June and 223% by December 2026.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

Bloomberg Finance LP

BONDS: NZGBS: Little Changed, Global Bonds Buoyed By Risk Off Sentiment

NZGBs closed little changed across benchmarks, with yields flat to 1bp higher.

- Cash US tsys are flat to 2bps richer, with a steepening bias, in today's Asia-Pac session after reversing early weakness amidst risk-off sentiment. US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed's Powell and Warsh ahead. The employment report for January on Friday.

- "NZ TREASURY SAYS INFLATION DATA DOESN'T SUGGEST OVERSTIMULATION" - BBG

- The 2-year swap rates closed slightly higher at 3.16%, the highest since July. For context, the rate sits some 70bps higher than mid-October levels.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 51bps.

- Tomorrow, the local calendar will see Building Permits data, ahead of Q4 Employment data on Wednesday.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

FOREX: USD - Trying To Push Higher, BBDXY Eyes 1195-1200

The BBDXY has had a range today of 1187.52 - 1190.03 in the Asia-Pac session; it is currently trading around 1189. The Dollar continued to pull back on Friday night as the move in Metals resulted in biblical pullbacks and the so-called “debasement trade” was put under pressure. The nomination of Warsh to Fed Chair has been of particular interest to the market due to his strong views on a smaller balance sheet and echoing Bessent's belief that the Fed has been involved in matters way outside of its purview. Warsh believes he can reduce the balance sheet and get interest rates lower, the market will be eagerly watching how he performs this magic trick. For the USD the market is left scratching its head a little as the break below 1180 proved to be false, it looks an ugly rejection below there and could imply the pullback has further to go. I suspect though that a bounce will find sellers again as the USD still has few friends. On the day, the first resistance is in the 1190-1195 area and then back towards 1200 where I suspect sellers would return in earnest.

- EUR/USD - Asian range 1.1840-1.1875, Asia is currently trading 1.1865. Price action has left an ugly bearish shadow on the weekly chart, and we might still get further retracements. On the day, the first support is between the 1.1800-1.1840 area initially a move through here would open up a deeper reversion back to the important 1.1700 area where I suspect buyers would again return. I suspect a bounce back toward the 1.19220-1.1950 area would find sellers first up as some risk is pared back across the board after such a big move.

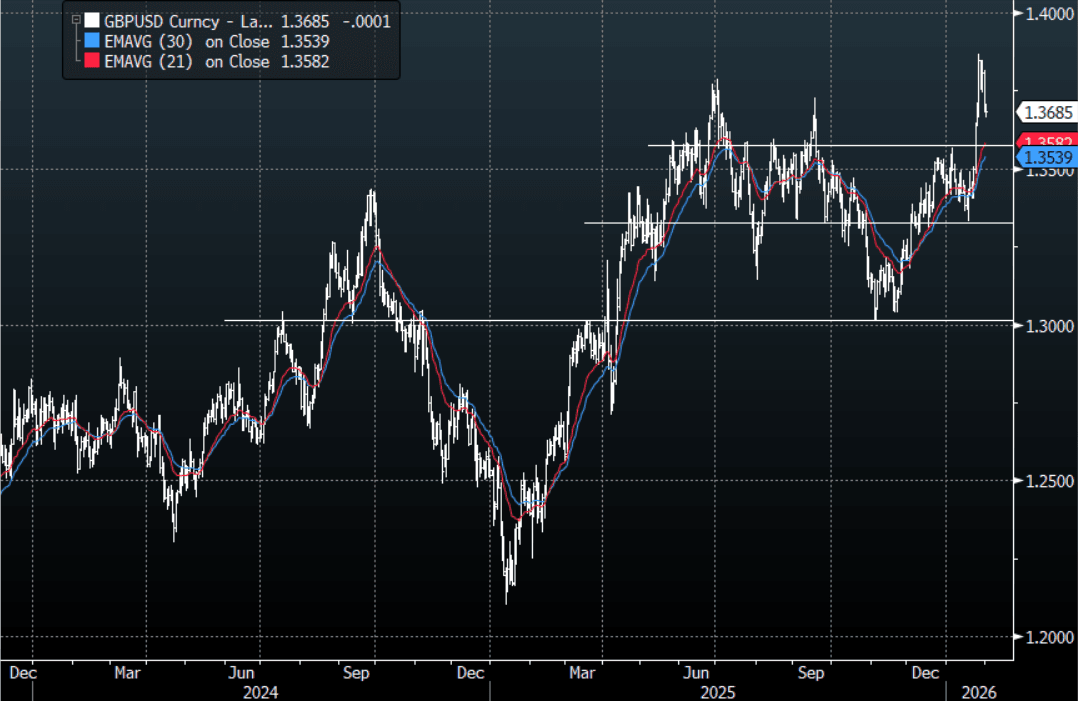

- GBP/USD - Asian range 1.3662-1.3706, Asia is currently dealing around 1.3685. The pair like everything else had an ugly weekly close leaving a clear rejection of the 1.3850 area. The price action suggests we could see some further retracements but I suspect buyers could reemerge on any decent dip. On the day, first support is 1.3600-1.3650 then the 1.3500 area.

- Cross asset : SPX -1.05%, Gold $4700, US 10-Year 4.23%, BBDXY 1189, Crude Oil $62.14

- Data/Events : Germany Retail Sales/HCOB Germany Manufacturing PMI, Italy HCOB Italy Manufacturing PMI/Budget Balance, Spain HCOB Spain Manufacturing PMI, EZ HCOB Eurozone Manufacturing PMI, France HCOB France Manufacturing PMI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Struggles Toward 155.50 As Takaichi Clarifies Yen Comments

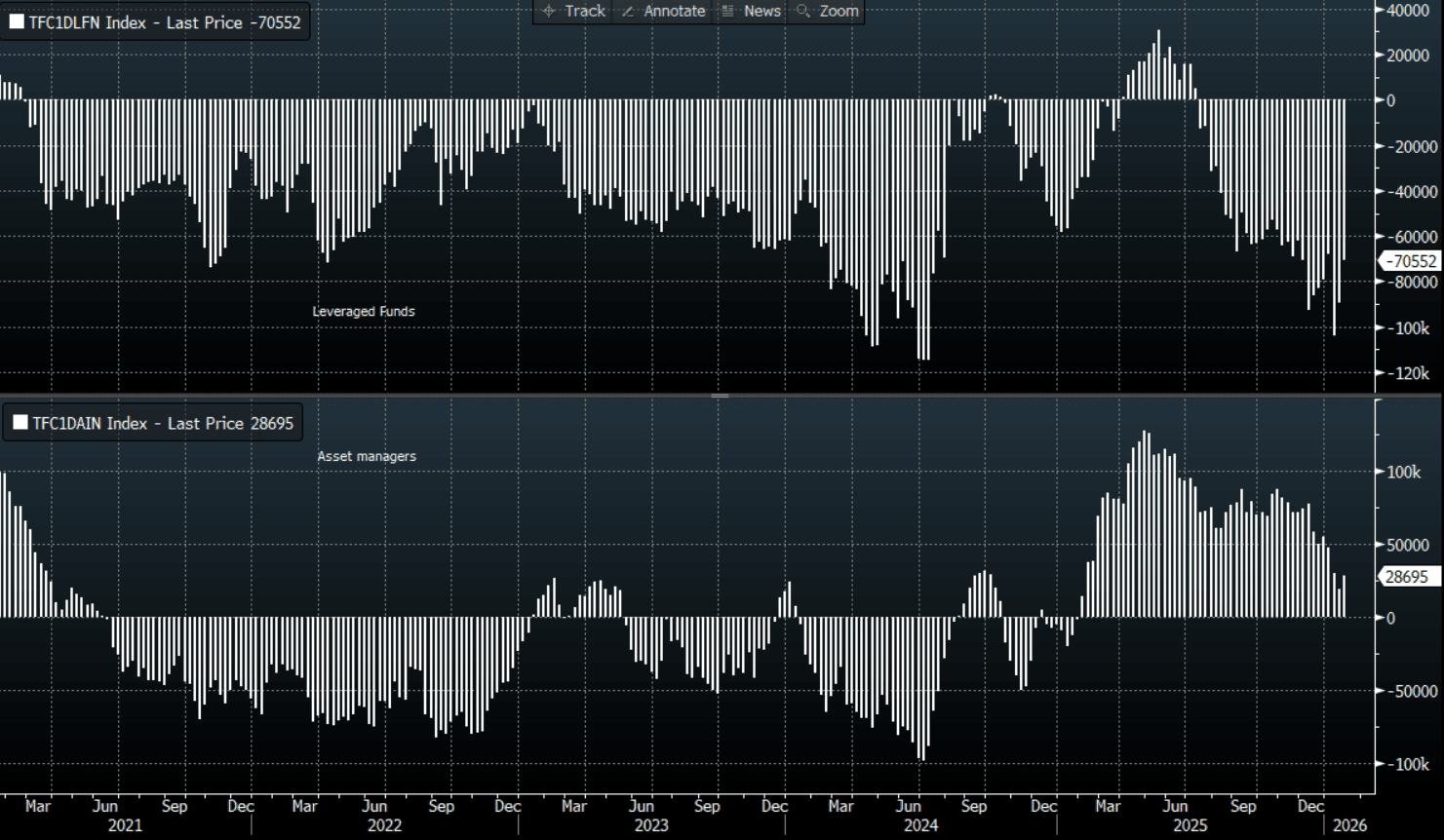

The USD/JPY range today has been 154.82 - 155.51 in the Asia-Pac session, it is currently trading around 154.90, +0.05%. The USD/JPY move higher seemed to stall toward 155.50 today as risk turned meaningfully lower. CFTC data up until last Tuesday shows leveraged funds paring back large Yen shorts, this bounce back to 155-156 might provide good levels to further reduce positioning for CTA/Momentum type players. In today's session, watch to see if these positions are further reduced into the 155.00-156.00 area. The juggernaut speed it was building to the topside looks to have been broken for now and we might need to consolidate and do some work before embarking on a clear trend again.

- MNI: BOJ Opinions: Early Rate Hikes, Upside Risks to Prices. Several Bank of Japan board members saw the need to raise the policy interest rate relatively early, with one favouring hikes at intervals of a few months, according to the summary of opinions

- Bloomberg - "Japan's ruling bloc is poised to win 300 out of 465 seats in the upcoming election, an Asahi poll showed.”

- “Sanae Takaichi sought to clarify her earlier comments about the yen, saying Japan needs to create an economy that can withstand currency fluctuations.”

- CFTC Data up to 27/01/2026 shows Asset Managers started to add back to their reduced JPY longs, +28695(Last +19404). The Leveraged community continued to pare back their large shorts after the BOJ, –70552(Last -89657).

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($570m), 155.70($530m). Upcoming Close Strikes : 153.00($1.23b Feb 5), 151.50($1.11b Feb 4) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 142 Points

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD/USD - An Ugly Weekly Close As Risk Starts The Week Under Pressure

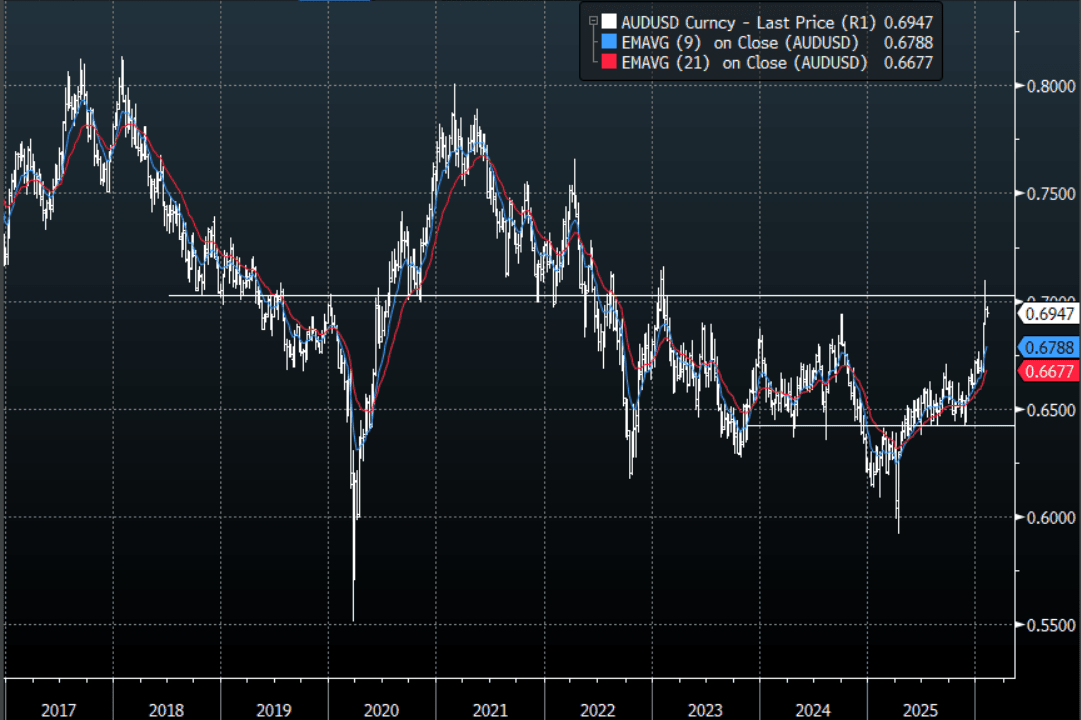

The AUD/USD has had a range today of 0.6921 - 0.6971 in the Asia- Pac session, it is currently trading around 0.6945, -0.30%. Risk starts the week under some decent pressure, the AUD is consolidating around 0.6950 after the collapse in Metals and the bounce in the USD saw it put in an ugly rejection on the weekly chart. The AUD has been outperforming across the board as leveraged funds increase their longs anticipating a potential RBA hike tomorrow, but when we see an event like Friday night, the repercussions tend to cascade as traders are forced to pare back and deleverage risk across the board. My first instinct is to look for dips to be supported in the AUD but we might need to see how risk fares over the next couple of days as the move in metals could have some contagion and it could take a few days for its full implications to be seen. On the day, the first buy-zone is back toward the 0.6885-0.6915 area, if this does not hold we could see a deeper pullback toward 0.6800-0.6850. I suspect a bounce towards 0.7000-0.7030 could see sellers return initially as the market waits for the dust to settle. There looks to be some decent optionality between 0.6900-0.6950 which should see it do some work.

- MNI AU - OIS now reflects materially tighter policy expectations across the curve. A 25bp hike tomorrow is priced at a 77% probability (up from 32% pre-jobs data), with cumulative tightening probability of 166% by June (vs 88% pre-jobs) and 229% by December 2026 (vs 152% pre-jobs).

- CFTC Data up to 27/01/2026 shows Asset managers continued to reduce their shorts, -18983(Last -31659). The Leveraged community was again aggressively adding to newly built longs, +39860(Last +24741).

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6900(AUD474m), 0.6925(AUD304m), 0.6930(AUD325m). Upcoming Close Strikes : 0.6850(AUD886m Feb 5), 0.6950(AUD1.81b Feb 4) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 73 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD-Consolidates Above 0.6000 As Risk Starts The Week Under Pressure

The NZD/USD had a range today of 0.5993-0.6034 in the Asia-Pac session, it is currently trading around 0.6020, -0.02%. The NZD is holding just above 0.6000 for now even with risk starting the week under serious pressure. The NZD failed again just ahead of 0.6100, the collapse in Metals and the bounce in the USD saw it retrace on Friday. Like the AUD my first instinct is to look for dips to be supported in the NZD but we might need to see how risk fares over the next couple of days as the move in metals could have some contagion and it could take a few days for its full implications to be seen. On the day, the first support is right here 0.5980-0.6010 and then 0.5900-0.5950. I suspect a bounce back toward 0.6050-70 could now see some sellers first up. I was surprised by the CFTC data as the price action suggested there had been much more paring back of shorts but as of yet the bears seem to be holding on.

- "NZ TREASURY SAYS INFLATION DATA DOESN’T SUGGEST OVERSTIMULATION" - BBG

- MNI AU - China PMI MFg Cools View of Imminent Rate Cuts: China's PMI Manufacturing for private and export companies expanded more than expected in January. Following on from the strong rebound in Industrial Profits in December, this for some is further support for the view that there are no imminent changes in policy to support the economy. PMI Mfg was forecast to stay just in expansion at +50, and whilst +50.3 does not suggest the expansion is significant it may be enough to cool expectations on policy ahead of lunar new year.

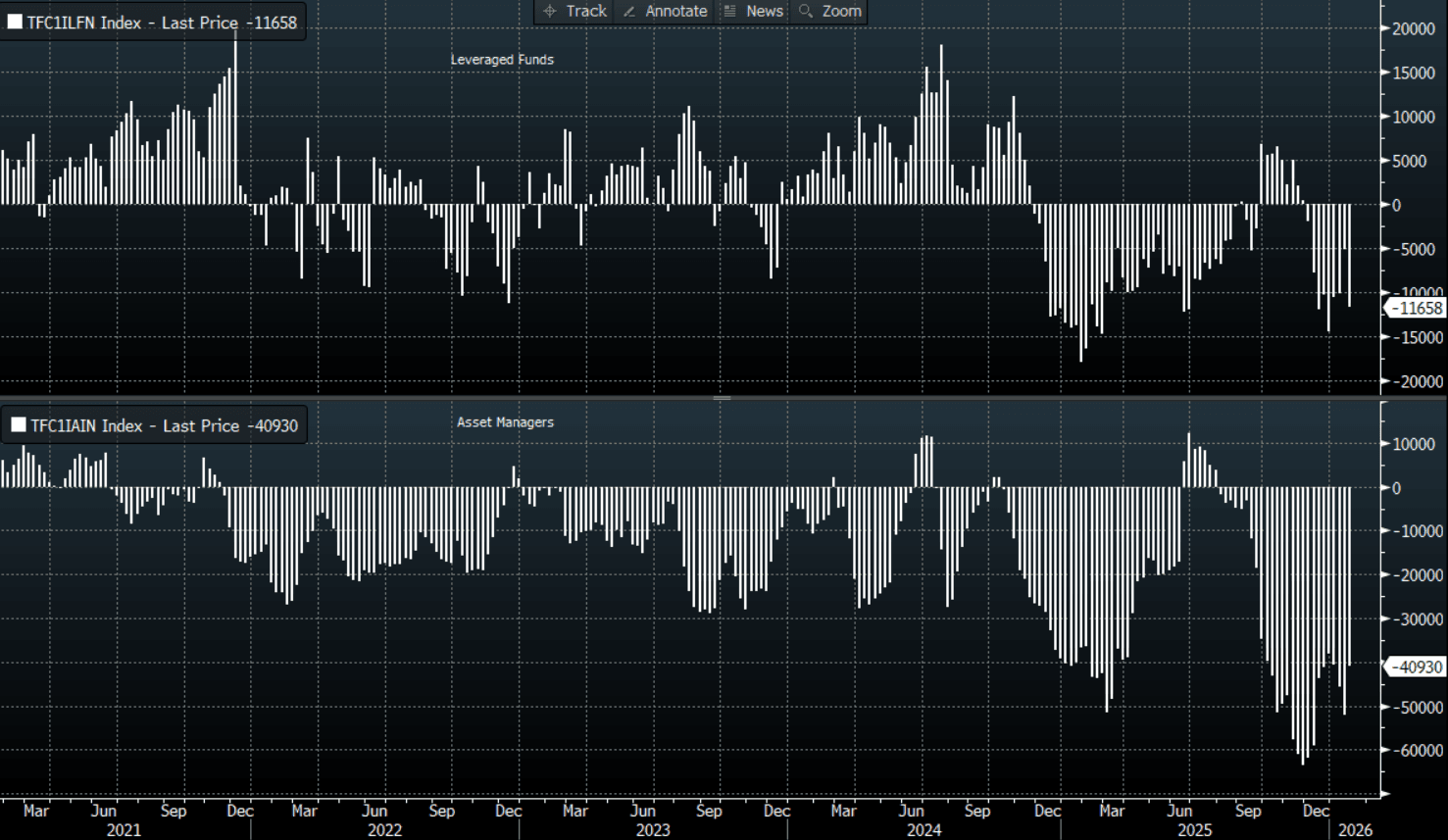

- CFTC Data up to 27/01/2026 shows Asset Managers paring back their short positions in the NZD, -40930(Last -52099). The Leveraged community surprisingly added back to their own shorts which they had just started to wind down, -11658(Last -5119).

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD887m Feb 3), 0.5975(NZD746m Feb 4) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 58 Points

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

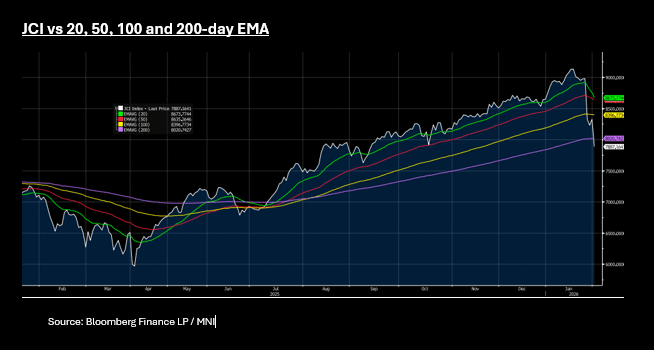

ASIA STOCKS: Ripple Effect Through Stocks, Profit Taking on AI Adding

The ripple effect of the new FED Chair markets has followed through to stocks, creating downward pressure amidst on over valued markets as losses mount. A huge day of losses Friday across precious metals included a 25% decline in silver and near 10% in gold, the knock on effects rippling through Aia stocks with all major markets lower. Tech stocks were in line today with headline names like Softhank (-2.7%), SK Hynix (-5.2%), Samsung (-4.1%) and TSMC (-1.4%) dragging their bourses lower as the Nvidea CEO clarified his investment forecasts for AI . Asia's equities are correlated to US interest rates and a historic analysis of new Fed Chair Warsh, shows him to be a hawk. This is at odds with Trump's desire for lower rates and that push pull is a further input to volatility. The NIKKEI was a standout earlier rising over 1% following polls suggesting PM Takaichi was likely to secure a lower house majority, though those gains fizzled out into the afternoon.

Sentiment appears fragile and with such positivity priced into many markets, with the possibility of further volatility as profit takers step in. Again the problems were focused in Jakarta as the JCI was the biggest faller, down over 5%, with the KOSPI down by -3.4% for its biggest one day decline since November. The JCI has fallen below all major moving averages over the course of four trading days, as outflows from stocks ramp up. News of regulatory changes to increase equity allocations for funds will do little for now to help.

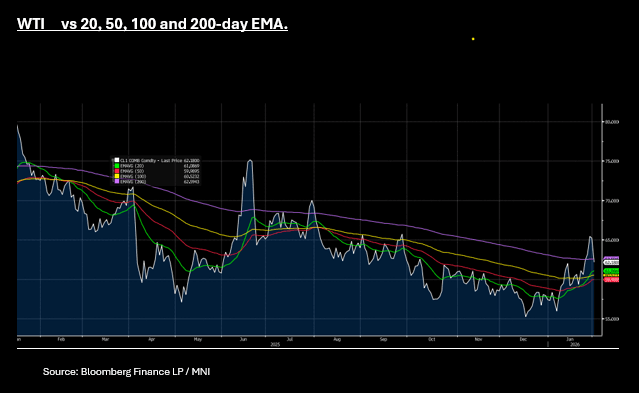

OIL: Geopolitics Sidelined as Risk-Off Hits Oil

- A global risk off sentiment followed through into oil Monday with WTI and Brent both down heavily.

- WTI is down -4.6% at US$62.16 bbl, trading through the 200-day EMA of $62.59. Below is downside resistance via the 20-day EMA of $61.08

- Brent is down -6.3% to $66.22, having held above $70 bbl only briefly. Brent is now near to the 200-day EMA and further falls below could bring the 20-day EMA into play at $65.74

- OPEC's decision to maintain its pause in supply when WTI / Brent are both c. 18% higher than their December lows comes at an interesting time in global oil politics.

- Investors are navigating a "Trump put" on energy, as the administration prioritizes lower prices (targeting $50/bbl or lower) to manage inflation in a world of tightened sanctions on Russia and redirected Venezuelan flows shifting global trade patterns.

- The underlying market narrative remains bearish due to a projected surplus. However adding to the supply considerations is severe weather related disruptions in the US, outages in Kazakhstan and Libya and investors who had loaded up on bearish bets for oil.

- The wash out in markets began with the FED Chair announcement and key markets like precious metals have been hit hard. This will have a knock on effect as portfolio adjust. Look for oil markets to re-focus on the mounting risks in the Middle East.

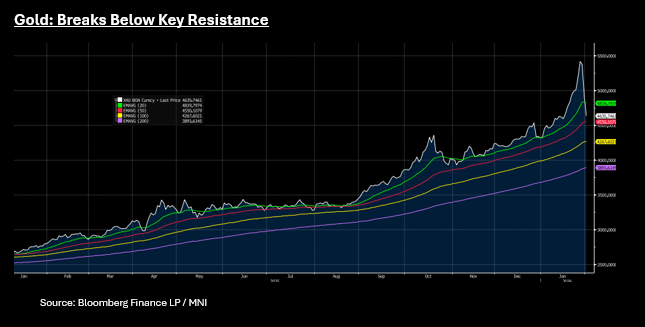

Gold's Vol to Stay as Portfolios Adjust

- Gold's decline continues Monday as the 'Warsh effect' as a saying now comes into being. Markets perceive Warsh as more hawkish, leading to expectations of a smaller Fed balance sheet and a focus on combating inflation, whilst uncertain about the path of interest rate.

- Gold is arguably one of the most crowded trades in markets at present following a surge in 2025 of more than 60% and a record-breaking start to 2026 taking bullions price on momentum indicators to the most over bought in more than a decade.

- Due for a correction, gold fell sharply post Warsh's announcement and that has followed on into Asia where it is down -5.7% currently.

- Gold's rise had reached over 20% year to date and has fallen 15% from the peak of US$5,417.21. Gold has fallen below the 20-day EMA of $4,819, with downside resistance via the 50-day EMA at 4,550.

- This will take several days to wash out as positioning was heavily skewed for further appreciation. This may cause knock on effects across other assets as portfolios are rebalanced even when the longer term structural reason for gold's ascent has not changed.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/02/2026 | 0700/0800 | ** | Retail Sales | |

| 02/02/2026 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0815/0915 | ** | Retail Sales | |

| 02/02/2026 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 02/02/2026 | 1145/1145 | BOE Breeden on Payments | ||

| 02/02/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/02/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/02/2026 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 03/02/2026 | 0030/1130 | * | Building Approvals | |

| 03/02/2026 | 0330/1430 | *** | RBA Rate Decision | |

| 03/02/2026 | 0700/0200 | * | Turkey CPI | |

| 03/02/2026 | 0745/0845 | *** | HICP (p) | |

| 03/02/2026 | 0745/0845 | Budget Balance | ||

| 03/02/2026 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 03/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/02/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 03/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index |