MNI EUROPEAN OPEN: Equity Jitters Continue Ahead Of US Data

EXECUTIVE SUMMARY

- US OFFERS UKRAINE SECURITY GUARANTEE BUT TERRITORY STILL KEY - BBG

- FED’S COLLINS NEEDS MORE INFLATION CLARITY TO CUT - MNI BRIEF

- MNI ECB WATCH: RATES ON HOLD, EYES ON PROJECTIONS, LANGUAGE - MNI

- MNI BOE WATCH: MPC FRACTURED, WITH GOVERNOR BAILEY KEY TO CUT - MNI

- TWO OF AUSTRALIA'S MAJOR BANKS NOW SEE RBA RATE HIKE IN FEBRUARY - BBG

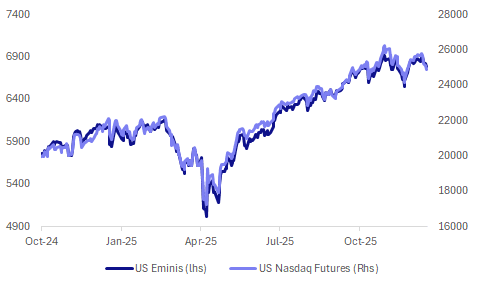

Fig 1: US Equity Futures

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

BOE (MNI BOE WATCH): The Bank of England's nine strong Monetary Policy Committee looks set to fracture once again over a rate cut, with Governor Andrew Bailey widely expected by analysts to deliver the key swing vote in favour of easing policy.

TRADE (BBG): “The UK finalized a long-awaited free trade agreement with South Korea that the government said would boost exporters from automaker Bentley to beverages firm Diageo."

EU

ECB (MNI ECB WATCH): The European Central Bank is set to hold its key deposit rate at 2% on Thursday, extending the ‘good place narrative’ as it presents a new set of projections that are unlikely to depart significantly from the September version. (ECB To Hold Again, Eyes On Language Changes).

UKRAINE (BBG): “US negotiators offered more significant security guarantees to Kyiv as part of President Donald Trump’s renewed push to end the Russia-Ukraine war, but the effort still appeared part of a bid to pressure President Volodymyr Zelenskiy on territory.”

UKRAINE (RTRS): "European leaders said they had agreed on Monday any decisions on potential Ukrainian territorial concessions to Russia could only be made once robust security guarantees were in place which should include a European-led multinational force"

FRANCE (BBG): "French Finance Minister Roland Lescure said the senate’s version of the 2026 budget would lead to an unacceptably wide deficit and called for major changes as lawmakers struggle to stabilize financial plans before year-end."

SWEDEN (MNI RIKSBANK WATCH): The Riksbank looks near certain to leave its policy rate unchanged at 1.75 percent at its December meeting with the focus on whether or not it tilts its rate path up, aligning it better with market pricing that the first hike could come at some point in 2026.

US

FED (MNI BRIEF): Federal Reserve Bank of Boston President Susan Collins said Monday she needs more evidence that inflation is cooling before supporting another interest rate cut.

FED (MNI BRIEF): The Federal Reserve's interest rate cuts this year leave the central bank in a good position against the backdrop of a cooling labor market and inflation that remains elevated but does not appear to be resurging due to tariffs, New York Fed President John Williams said Monday.

FED (MNI BRIEF): Federal Reserve Governor Stephen Miran argued again Monday for lowering interest rates faster, citing underlying inflation pressures close to target and the risk of rapid job market deterioration.

FED (MNI BRIEF): The Federal Reserve's standing repo facility hasn't performed up to expectations to cap money market rate pressures, Fed Governor Stephen Miran said Monday.

NASDAQ (BBG): “Nasdaq Inc., the second-largest exchange in the US, is looking for regulatory approval to extend trading hours on its stock venues to 23 hours during the work week."

CORPORATE (BBG): "Ford Motor Co. will take $19.5 billion in charges tied to a sweeping overhaul of its electric vehicle business after struggling for years to make it profitable."

OTHER

MEXICO (MNI EM BANXICO WATCH): The Central Bank of Mexico is widely expected to cut its overnight interbank rate by 25 basis points to 7.00% at its final meeting of the year, the lowest level since May 2022. It would be the fourth reduction in a row of this size, following four 50-basis-point reductions in the first half of the year. Banxico cut rates by 25bp to 7.25% in a split decision last month, with Deputy Governor Jonathan Heath dissenting in favor of a hold. Expectations point to an even more divided board at this week's meeting, especially after the latest inflation data came in worse than expected.

AUSTRALIA (BBG): " Two of Australia’s top lenders said on Tuesday they expect the Reserve Bank will return to interest-rate increases in February in order to tackle persistent price pressures in the economy."

NEW ZEALAND (BBG): "The New Zealand government will head into an election year facing deeper budget deficits and a delayed return to surplus as an economic recovery takes longer to gather momentum."

CHINA

HOUSING (ANJUKE): “The proportion of people searching for second-hand homes reached 65.8% in November, rising for five consecutive months, according to data from Anjuke, a real-estate research firm. However, the popularity did not raise prices as a surge in supply diluted demand enthusiasm, with listing volumes in some cities increasing significantly, according to Zhang Bo.”

DEPOSITS (YICAI): “The latest central bank data indicated that in November the growth rate of yuan deposits slowed markedly, experts told the Yicai news agency. Non-bank deposits rose by CNY80 billion, representing a year-on-year decline of CNY100 billion, with most institutional analyses suggesting that the pace of residents’ “deposit migration” had temporarily eased, largely reflecting reduced activity in capital markets.”

YUAN (BBG): "In well-connected circles within China, the yuan’s persistent weakness is increasingly being seen as an obstacle to the country’s growth. A rising number of Chinese economists and former central bank officials are arguing a stronger currency is needed if the country is to rebalance the economy away from exports, boost tepid consumer demand and reduce trade conflicts."

MNI: PBOC Net Injects CNY18.0 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY135.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY18 billion after offsetting maturities of CNY117.3 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4019% at 09:25 am local time from the close of 1.4440% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 47 on Monday, compared with the close of 49 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0602 Tues; +3.52% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0602 on Tuesday, compared with 7.0656 set on Monday. The fixing was estimated at 7.0495 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND NOV FOOD PRICES -0.4%; PRIOR -0.3%

NEW ZEALAND NOV NON-REISDENT BOND HOLDINGS 59.5%; PRIOR 60.3%

AUSTRALIA DEC P S&P GLOBAL PMI MFG 52.2; PRIOR 51.6

AUSTRALIA DEC P S&P GLOBAL PMI SERVICES 51.0; PRIOR 52.8

AUSTRALIA DEC P S&P GLOBAL PMI COMPOSITE 51.1; PRIOR 52.6

AUSTRALIA DEC WESTPAC CONSUMER CONFIDENCE INDEX 94.5; PRIOR 103.8

JAPAN DEC P S&P GLOBAL PMI MFG 49.7; PRIOR 48.7

JAPAN DEC P S&P GLOBAL PMI SERVICES 52.5 PRIOR 53.2

JAPAN DEC P S&P GLOBAL PMI COMPOSITE 51.5; PRIOR 52.0

SOUTH KOREA OCT MONEY SUPPLY M2 SA M/M 0.9%; PRIOR 0.7%

MARKETS

US TSYS: Yields Grind Lower as Equities Fall, Attention Turns to Data

Bond futures opened up this morning in Asia but with limited follow on. The US 10-Yr opened at 112-10+ and got to 112-12+ where it has stayed all day as it nears the topside resistance being the 100-day EMA of 112-14+.

Cash was stronger with yields -0.2 - 1.00bps lower across the curve with intermediate maturities the best performers.

- The 2-Yr is down -0.6bps at 3.497%

- The 5-Yr is down -0.9bps at 3.717%

- The 10-Yr is down -0.6bps at 4.17%

- The 30-Yr is down -0.2bps at 4.846%

US Non Farm Payrolls are the next focus for markets. Here is the MNI US Payrolls Preview: Double NFPs And A Single Unemployment Update

https://media.marketnews.com/USNFP_Nov2025_Preview_postshutdown_392dffc2d3.pdf

Tonight there is a US$75bn 6-week auction as the primary focus.

JGBS: Subdued Session, BOJ Hike On Friday Is Fully Priced

JGB futures are little changed compared to settlement levels.

- The BOJ is widely expected to raise its policy interest rate by 25 basis points to 0.75% at the upcoming December 18-19 Monetary Policy Meeting.

- Some analysts, however, caution that a December hike is not guaranteed. A 26 November Reuters article described a December move as merely “possible.” Goldman Sachs has emphasised that with only a limited number of companies having announced wage plans so far, there is a risk that insufficient information will be available by the December meeting. In that scenario, the BOJ may delay a hike until wage announcements by large firms later in December and the January Branch Managers’ meeting.

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session ahead of today's heavy US data schedule that includes headline NFP for November, weekly ADP, Retail Sales and S&P Global flash PMIs.

- Cash JGBs are little changed across benchmarks out to the 20-year, and ~2bps richer (30-year) beyond. The benchmark 10-year yield is 0.3bp lower at 1.956% versus the cycle high of 1.976%.

- Swap rates are little changed.

- Tomorrow, the local calendar will see Trade Balance and Core Machine Orders data alongside 1-year supply.

Source: Bloomberg Finance LP

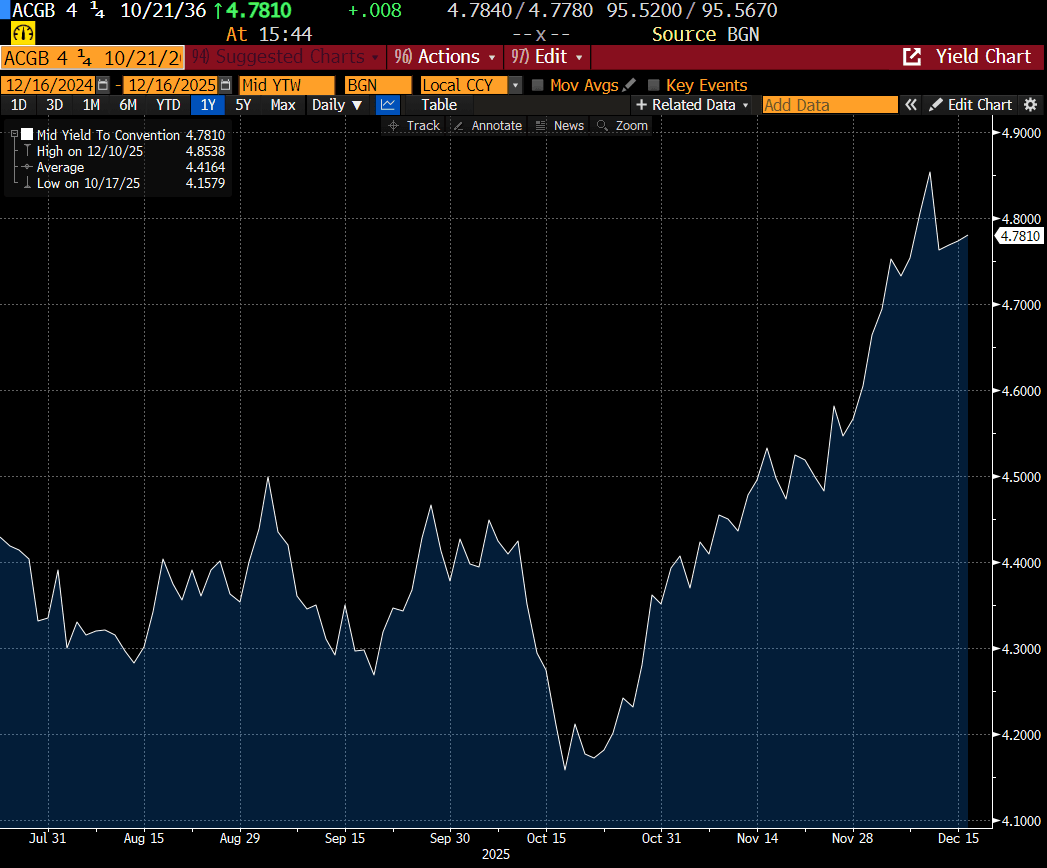

AUSSIE BONDS: Modestly Weaker, Con Conf Up, Oct-36 Supply Tomorrow

ACGBs (YM -3.0 & XM -1.0 ) are modestly weaker and hovering near the session’s worst levels.

- The Westpac Consumer Sentiment Index fell back sharply in Dec, off 9% to 94.5. Recall that we saw a surge in the Nov print to 103.8, which was the highest sentiment reading since early 2022. This latest move corrects somewhat for that, but we remain above 2025 lows for sentiment, which were around 90.0.

- Cash US tsys are slightly richer, with a steepening bias, in today’s Asia-Pac session ahead of today’s heavy US data schedule that includes headline NFP for November, weekly ADP, Retail Sales and S&P Global flash PMIs.

- Cash ACGBs are 1-3bps higher with the AU-US 10-year yield differential at +56bps, ~6bps lower than its recent high.

- The bills strip has bear-flattened, with pricing -3 to -7.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 41% for February to 98% by June and 153% by December 2026.

- Tomorrow, the local calendar will see Westpac Leading Index data.

- The AOFM plans to sell A$1000mn of the 4.25% 21 October 2036 bond on Wednesday. The new Oct-36 bond was issued at a yield to maturity of 4.36% versus its current level of 4.78%.

Bloomberg Finance LP

BONDS: NZGBS: Richer But Off Session Bests Sparked By Bond Program Revisions

NZGBs closed stronger but well off the session’s best levels, seen around the release of revisions to the government bond program.

- NZ Treasury's half-year fiscal and economic update projects the operating balance will return to surplus in the year ending June 2030, a year later than the May Budget, which expected a surplus in 2029.

- The update projects a 2025-26 deficit of NZ$13.9bn (up from NZ$12.1bn in May), with deficits gradually declining to NZ$945mn in 2028-29 before reaching a NZ$2.3bn surplus in 2029-30. Net core Crown debt is expected to peak at 46.9% of GDP in 2027-28.

- NZDM has revised the government bond program, with planned issuance of NZ$35bn in 2025-26, down NZ$3bn from the Budget, and NZ$34bn in 2026-27, down NZ$2bn, before rising in later years.

- NZGB yields, led by the 5-year, declined as much as 12bps, before ending the session 4-7bps richer. The NZ-US and NZ-AU 10-year yield differentials closed 3bps lower.

- Swap rates close 2-4bps lower, with the 2s10s curve steeper.

- RBNZ-dated OIS pricing closed softer across meetings. No tightening is priced for February, while November 2026 assigns 44bps.

- Tomorrow, the local calendar will see Q3 Current Account Balance and Westpac Consumer Confidence. The RBNZ will also publish Decisions on Capital Settings.

Bloomberg Finance LP

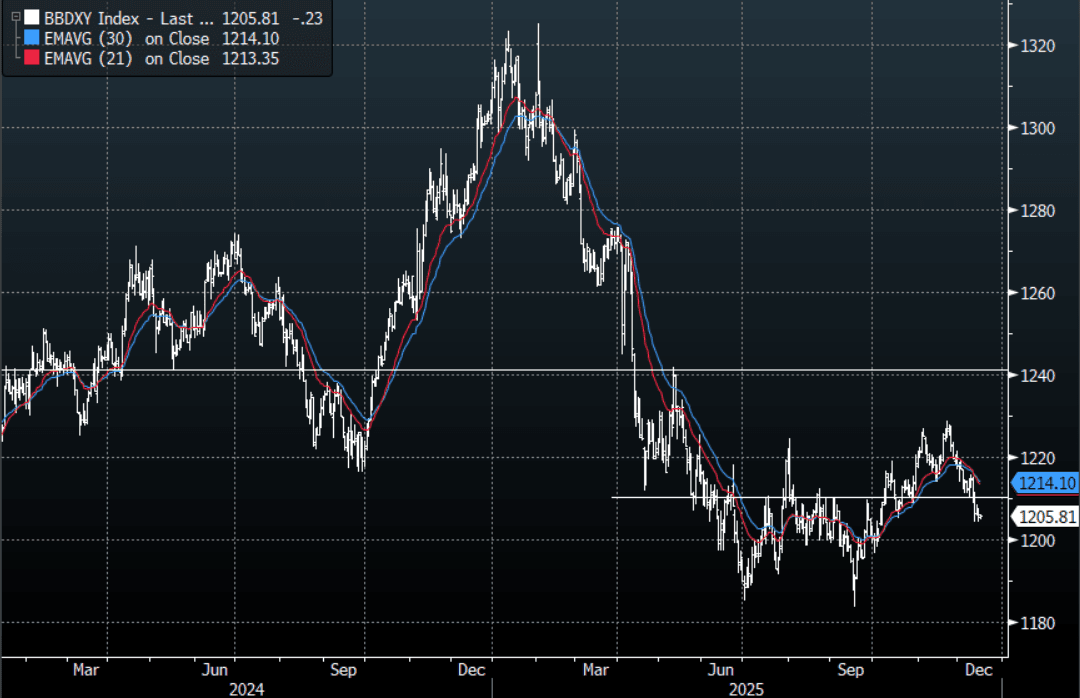

FOREX: USD - BBDXY Holds Above 1204-1205 For Now

The BBDXY has had a range today of 1205.04 - 1206.29 in the Asia-Pac session; it is currently trading around 1205, -0.05%. The USD continues to find support between 1204-1205 but has still failed to react to a weakening risk backdrop. Is it lagging or is it waiting for clarity from postponed US data tonight. The supreme court decision regarding tariffs looks like it might now be a problem for early 2026 but the tail risk of an early decision does still exist. On the day look for initial resistance again back towards the 1208-110 area and above here the more important 1213-1216 area where sellers should remerge initially. Support is in the 1204/05 area; a move below here would target 1198-1200.

- EUR/USD - Asian range 1.1747-1.1759, Asia is currently trading 1.1750. The pair is trading sideways trying to hold onto its gains above 1.1700. On the day, first support is toward 1.1710-1730 initially, if this does not hold, look for demand to then return in the 1.1640-1.1670 area.

- GBP/USD - Asian range 1.3362-1.3383, Asia is currently dealing around 1.3365. The pair stalled above 1.3400 at the end of last week. On the day GBP has initial support around the 1.3325-1.3345 area, if this does not hold look for a pullback to the more important 1.3250/80 area. I continue to watch for signs of GBP potentially topping out.

- Cross asset : SPX -0.50%, Gold $4287, US 10-Year 4.17%, BBDXY 1205, Crude Oil $56.48

- Data/Events : Germany HCOB Germany PMI’s/ZEW Survey Expectations, France HCOB France PMI’s, Spain Labour Costs YoY, Italy CPI, EZ HCOB Eurozone PMI’s/ZEW Survey Expectations/Trade Balance

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

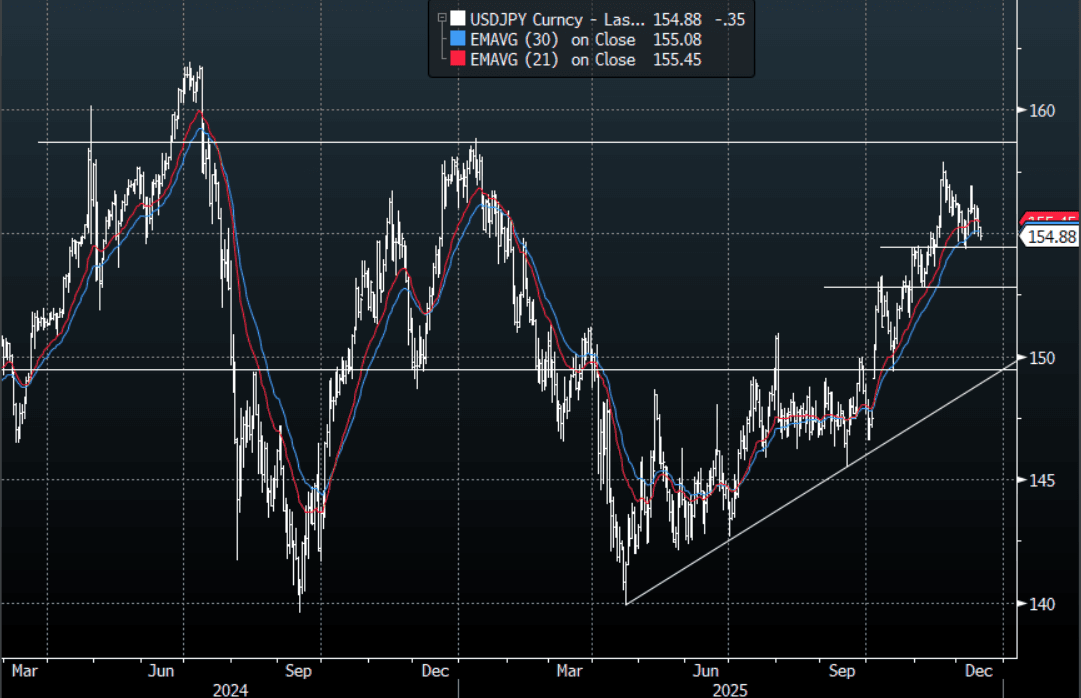

JPY: USD/JPY - Breaks Overnight Lows But Stops Short of Testing 154.30-154.50

The USD/JPY range today has been 154.71 - 155.26 in the Asia-Pac session, it is currently trading around 154.85, -0.25%. The pair has slid lower in our sessions as risk lurched lower in Asia. The market is pricing in a hike by the BOJ for this week, for the time being this is keeping the JPY contained and confined to a wider 154.50-157.00 range having capped its upward momentum. The market is awaiting the US data dump tonight which could increase the volatility. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. On the day, can the pair hold below 155.00 ahead of the data and challenge the 154.30-154.50 support, if not then look for sellers to reemerge back toward the 155.40-155.70 area.

- MNI AU - BoJ Hike 95% Priced For This Week With Two By September-2026

- MNI AU - PMIs Mixed, But Manufacturing Rises, Back Close To 50.0 : Japan S&P global preliminary PMIs for December were mixed. Most focus will likely rest with the manufacturing outcome, which rose to 49.7 from 48.7 prior. The services PMI eased to 52.5, from 53.2, while the composite reading was 51.5 (52.0 prior). On the manufacturing side, while still in contraction territory it is back near highs from the middle of this year. This fits with broader sentiment measures, like the Tankan survey, which have held up reasonably well. Fears of a significant negative impact (global slowdown etc) from higher US tariff levels haven't materialized. The higher PMI reading should support IP output all else equal, although IP growth has been outperforming softer PMI trends in recent months.

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.00($1.08b), 157.00($714m), 158.00($814m). Upcoming Close Strikes : 157.00($3.95b Dec 18 ), 158.00($4.78b Dec 18 ), 159.00($6.46b Dec 18 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 105 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

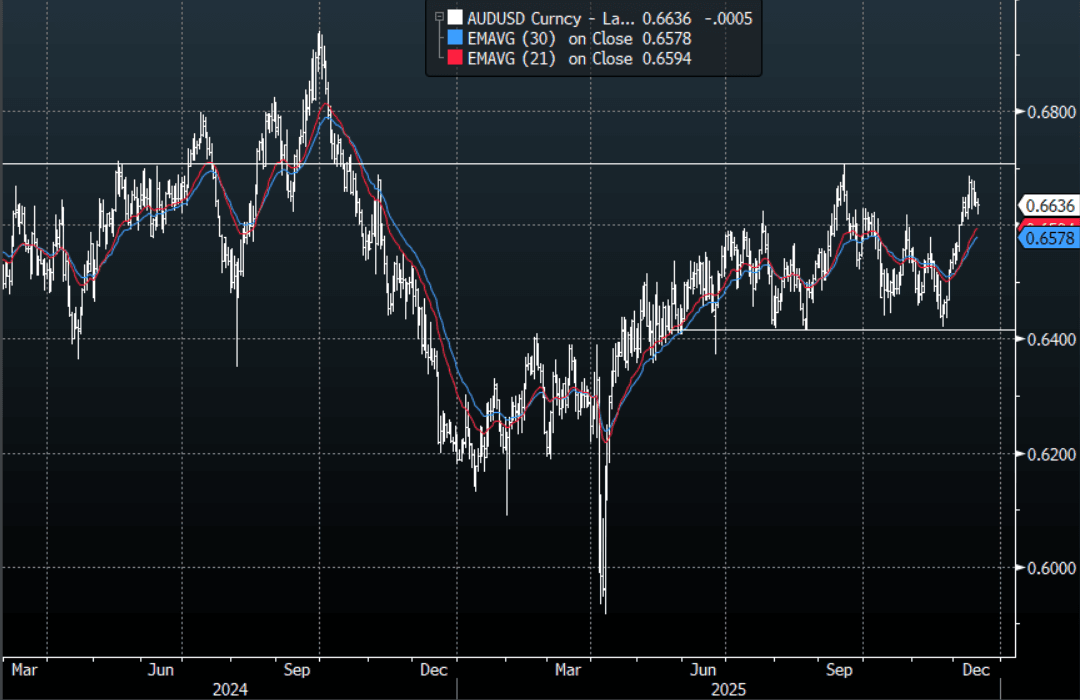

AUD/USD - Slips Lower With Risk

The AUD/USD has had a range today of 0.6618 - 0.6648 in the Asia- Pac session, it is currently trading around 0.6635, -0.10%. The AUD slipped lower as risk took a turn for the worst in Asia. The US stock market continues to show signs of exhaustion but the USD remains heavy as we approach some key US data. This data is old so I am not sure how relevant it is, but the market seems to think it could be important. The AUD price action remains very constructive but the wobble in risk has seen it slip. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. On the day, the 0.6600-0.6630 area should continue to find demand. If this area does not hold it could signal a deeper pullback toward the 0.6550 area.

- Bloomberg reports: “Two of Australia’s top lenders expect the Reserve Bank to return to interest-rate increases in February to tackle persistent price pressures in the economy. Commonwealth Bank of Australia predicts one rate rise next year to 3.85%, while National Australia Bank Ltd. expects two hikes for a terminal rate of 4.1%.” {NSN T7CBO6KK3NYE <GO>}

- MNI AU - Consumer Sentiment Dips, Inflation/Interest Rate Outlook Weigh: The Westpac Consumer Sentiment Index fell back sharply in Dec, off 9% to 94.5. While this marks a clear improvement from the prolonged, deep pessimism that defined much of 2024, a sustained move into outright optimism remains elusive for the Australian consumer." Adding, "Overall, the sentiment mix and responses to questions on news recall suggests stronger results on inflation have sparked a renewed angst over the trajectory for interest rates, which is feeding more broadly into concerns over the economic outlook."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD439m), 0.6640(AUD488m). Upcoming Close Strikes : 0.6550(AUD1.07b Dec 18 ), 0.6675(AUD1.1b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

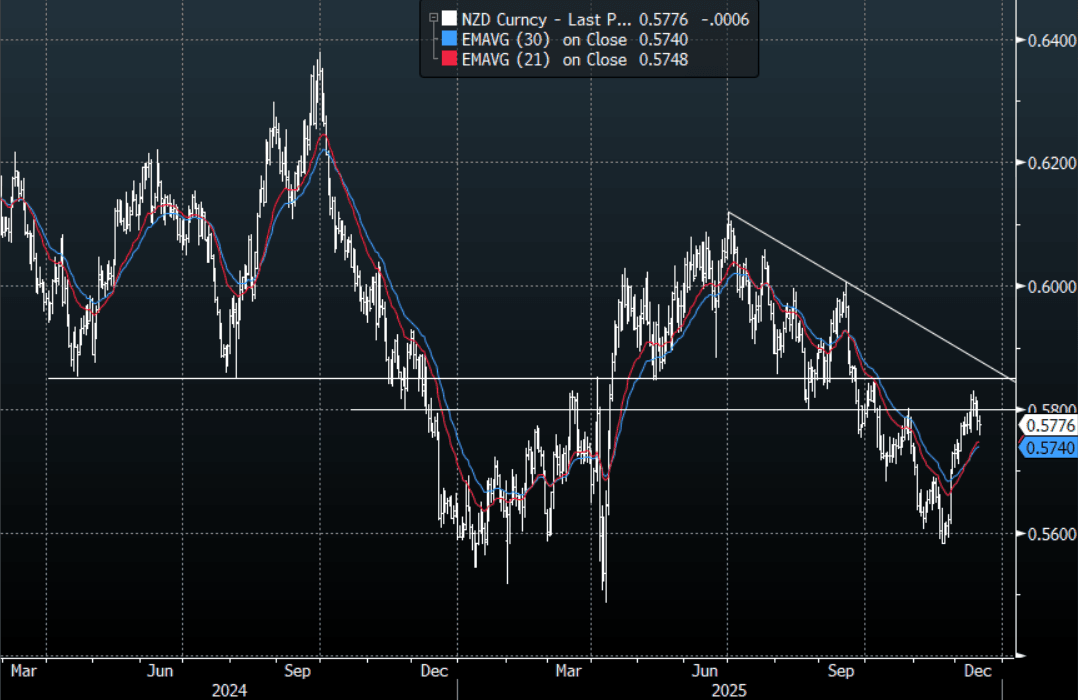

NZD/USD - Slips Lower, Finds Demand Again Toward The 0.5750 Area

The NZD/USD had a range today of 0.5758-0.5789 in the Asia-Pac session, going into the London open trading around 0.5775, -0.10%. The NZD has slid lower again in our day driven by risk moving lower ahead of some important US data. The NZD underperformed yesterday as well on the back of comments from the RBNZ’s Breman, but demand continues to be seen toward the 0.5750 area. On the day, I suspect we will consolidate in a range ahead of the US data dump, something like 0.5740 - 0.5810 should keep it contained until then.

- MNI AU - NZGBS: Sharp Rally As NZDM Revises Down Debt Issuance Outlook: The NZ government faces deeper budget deficits and a slower path back to surplus as the economic recovery lags. New Zealand Debt Management has revised the government bond program, with planned issuance of NZ$35bn in 2025-26, down NZ$3bn from the Budget, and NZ$34bn in 2026-27, down NZ$2bn, before rising in later years.

- Bloomberg - “The New Zealand government will head into an election year facing deeper budget deficits and a delayed return to surplus as an economic recovery takes longer to gather momentum.” {NSN T7C5DLT96OTD <GO>}

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5850(NZD304m). Upcoming Close Strikes : 0.5630(NZD594m Dec 19), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA: Tech Falls Weighing on Investor Sentiment

Asia equities are down again today with many key AI / Tech stocks dragging bourses lower. Ahead of anticipated US data (NF Payrolls) markets are cautious as the path for US interest rates remains uncertain. For the AI / Tech space, what started with Oracle's warning last week has grown into something more, exacerbated by highly stretched valuations. In China, mixed views on the economy are keeping equities at bay given what weak raft of data released yesterday and some strategists suggesting that more policy intervention is required. Stocks in Japan are under pressure ahead of the BOJ interest rate decision this week and an expected 25bps rate rise alongside tech weakness.

- The NIKKEI is down -1.30%, following yesterday's fall of -1.31% with key tech stock Softbank Group down -1.5%

- The KOSPI is down -1.65% after falls of -1.84% yesterday with leading AI Tech stock SK Hynix down -7% today alone. The losses sees the KOSPI at 4025 and dip below the 20-day EMA of 4046. Downside resistance in the form of the 50-day EMA is at 3,908.

- China's bourses are all down -1.50% - 2.00% with the Hang Seng the biggest faller. Down -1.9% the HSI leads the CSI 300 down -1.35% and Shenzhen down -1.77%. The HSI is near the 25,000 resistance level that it last traded below in August

- Taiwan's TAIEX is down -1.5% as TSMC drags the index down with falls of -1.7%

- India's NIFTY 50 closed near flat yesterday after falling earlier in the day but has opened down -0.34% today, breaking below 26,000 to be at 25,935

- The FTSE Malay KLCI continues to appear lowly correlated to its Asian peers, rising today by +0.15% whilst the JCI in Indonesia is down -0.20%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | Italy Final HICP | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 16/12/2025 | 1000/1100 | * | Trade Balance | |

| 16/12/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 16/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 16/12/2025 | 1000/1100 | Foreign Trade | ||

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1745/1245 | BOC Gov Macklem speech in Montreal | ||

| 17/12/2025 | 2350/0850 | * | Machinery orders | |

| 17/12/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 17/12/2025 | 0700/0700 | *** | Producer Prices | |

| 17/12/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 17/12/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities |