MNI EUROPEAN MARKETS ANALYSIS:China To Continue Policy Support

- Oil prices spiked higher at the open following reports of Israel striking Iranian energy assets, as the conflict continued. We sit off earlier highs for the oil benchmarks in latest dealings.

- US equity futures initially dipped, but now sit back in the green, while US yields have risen. The USD was firmer against the majors, but hasn't been able to sustain positive momentum.

- China data was mixed, with retail sales better than forecast, but property indicators are still struggling. The authorities said they will continue with active macro policies.

- Looking ahead, the US Empire manufacturing print is due, in what is a quiet start to the week data wise.

Source: Bloomberg Finance L.P./MNI

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher

The TYU5 range has been 110-18 to 110.26 during the Asia-Pacific session. It last changed hands at 110-18+, down 0-01 from the previous close.

- The US 2-year yield moved higher; it is currently trading around 3.969%, up 0.02 from its close.

- The US 10-year yield has moved higher, it is trading around 4.428%, up 0.03 from its close.

- MNI FED: Two Cuts Priced This Year Headed Into FOMC Week. As we head into the June Fed meeting week, market pricing is reflective of the FOMC’s messaging : The next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability of bringing the next 25bp reduction. Exactly 50bp of cuts are priced through end-2025, implying two Q4 cuts. That’s a shift from just after the May meeting, after which the next cut was fully priced by September, and there were closer to three cuts priced for the rest of the year.

- Bloomberg - “Even before this geopolitical flare-up, it was unlikely that Fed Chair Jerome Powell would validate dovish market pricing at Wednesday’s press conference. The FOMC has consistently emphasized the need for sustained progress and “greater confidence” that inflation is on track to return to the 2% target, and this weekend’s developments only further complicate an already uncertain path.”

- The 10-year yield has bounced strongly off its 4.30/35% support, this area needs to hold if yields are to move higher. A sustained break back below 4.30% and you would think more shorts will be pared back. It seems traders for the moment are more concerned with the move in oil and the implications it has for inflation than buying treasuries as a safe haven.

- Data/Events: Empire Manufacturing

JGBS: Cheaper, BoJ Decision Tomorrow, Ueda Presser & Taper Program In Focus

JGB futures are weaker, -52 compared to the settlement levels, and hovering near the session’s worst level.

- Cash US tsys are 2-3bps cheaper in today's Asia-Pac session. As we head into the June Fed meeting week, the next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability.

- The BoJ is expected to keep its policy rate unchanged at 0.50% tomorrow. The key area of interest will be Governor Kazuo Ueda’s post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes. If the BoJ begins to hint at stronger underlying inflationary trends or shows greater optimism about the economy, it could stoke expectations of a rate hike in the autumn.

- The second area of market focus is on the BoJ’s JGB purchase program. Market expectations suggest a slower pace of reductions during fiscal year 2026. If the BoJ chooses to maintain the current pace of ¥400 billion reductions per quarter in FY2026, this would be interpreted as a mildly hawkish move. (See MNI BoJ Preview here)

- Cash JGBs are flat to 4bps cheaper across benchmarks, with the 5-7-year zone leading.

- The swaps curve has twist-flattened, with rates 1bp higher to 1bp lower.

BOJ: MNI BoJ Preview - June 2025: Focus On Future Rate Hikes & QT

EXECUTIVE SUMMARY

- The Bank of Japan (BoJ) is set to hold its Monetary Policy Meeting (MPM) on June 16–17, and although no changes are expected to the current policy rate of 0.50%, the meeting may still prove impactful for both domestic and global markets.

- The key area of interest will be Governor Kazuo Ueda’s post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes.

- If the BoJ begins to hint at stronger underlying inflationary trends or shows greater optimism about the economy, it could stoke expectations of a rate hike in the autumn.

- The second area of market focus is on the BoJ’s Japanese Government Bond (JGB) purchase program.

- Currently, the BoJ is reducing its JGB purchases by ¥0.4 trillion per quarter, aiming for a pace of ¥2.9 trillion. This reduction is expected to continue without change through the first quarter of 2026. The real uncertainty lies in what happens beyond that point. Most analysts anticipate the BoJ will continue reducing purchases, but the pace is up for debate.

- Market expectations suggest a slower pace of reductions during fiscal year 2026. If the BoJ chooses to maintain the current pace of ¥400 billion reductions per quarter in FY2026, this would be interpreted as a mildly hawkish move.

- Full preview here:

AUSSIE BONDS: Cheaper, Jobs Report On Thurs, BoJ & FOMC Decisions Beforehand

ACGBs (YMU5 -8.0 & XMU5 -9.0) are weaker and hovering at/near Sydney session lows on a data-light day.

- Cash US tsys are 2-3bps cheaper in today’s Asia-Pac session. As we head into the June Fed meeting week, the next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability. Exactly 50bp of cuts are priced through end-2025, implying two Q4 cuts.

- Cash ACGBs are 6-8bps cheaper with the AU-US 10-year yield differential at -19bps.

- The bills strip has cheapened, with pricing -2 to -7.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given an 83% probability, with a cumulative 78bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty. The highlight of the week will be May jobs data on Thursday. Bloomberg consensus sees a 20k rise in new jobs, in line with the 3-month average, with the unemployment and participation rates stable at 4.1% and 67.1% respectively.

- The AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond tomorrow, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

BONDS: NZGBS: Bear-Steepens, Global Bond Yields Push Higher, Q1 GDP On Thu

NZGBs closed at the session’s worst levels, showing a solid bear-steepening of the 2/10 curve. Benchmark yields rose by 3-8bps higher.

- BNZ’s manufacturing and services PMIs both deteriorated in May and are below the breakeven-50 level. Senior economist Steel warned that they are consistent with a return to a recession. With rates now in the “neutral zone” and the RBNZ Governor Hawkesby saying the MPC doesn’t have a bias, it looks like the RBNZ will be on hold on July 9.

- The focus of the week will be on Thursday’s Q1 GDP release. Bloomberg consensus is forecasting another 0.7% q/q increase in production-based GDP. Expenditure-based GDP should see a significant contribution from agricultural and services (tourism) exports.

- Swap rates closed 3-8bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed 1-5bps firmer across meetings. 4bps of easing is priced for July, with a cumulative 28bps by November 2025.

- Tomorrow, the local calendar will see Food Prices.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.

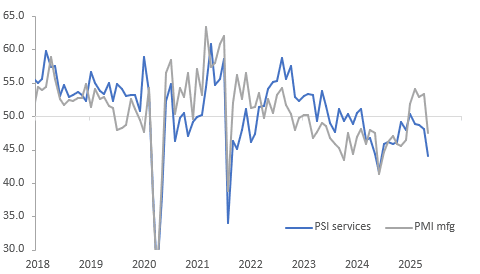

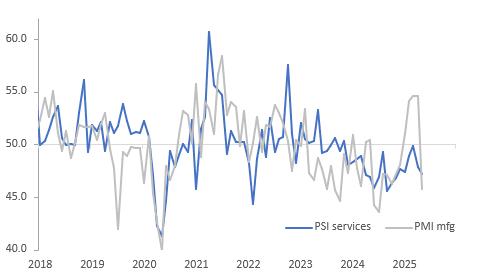

NEW ZEALAND: BNZ Indices Signal Economic Slowdown & Job Shedding

BNZ’s manufacturing and services PMIs both deteriorated in May and are below the breakeven-50 level and senior economist Steel warned that they are consistent with a return to a recession. With rates now in the “neutral zone” and the RBNZ Governor Hawkesby saying the MPC doesn’t have a bias, it looks like the RBNZ will be on hold on July 9 as it waits for more data, but it does monitor these indices and they suggest that the meeting will be “live”. The June PMIs are not released until July 10 & 13.

NZ BNZ PMI vs PSI

Source: MNI - Market News/BNZ/LSEG

- The performance of services index fell 4.1 points to 44.0 in May, the lowest since June 2024 signalling that the sector contracted at its fastest rate in almost a year. The decline was driven by sharp drops in new orders and activity/sales. All components are in negative territory.

- BNZ noted that negative comments from services businesses rose to 65.6% in May from 61.8% in April and 56.7% in March. They cited “rising costs, economic uncertainty and low consumer confidence” as reasons for the increase and that customers remain cautious.

- Services employment fell at a slightly faster pace in May at 47.2 than April’s 47.9. There was also job shedding in the manufacturing sector with the employment index falling to 45.7 from 54.6, the lowest since July 2024 and suggesting that recent global developments have impacted hiring plans. This does not bode well for Q2 employment with both sectors so weak.

- The manufacturing PMI in May shifted into contractionary territory for the first time in 2025 at 47.5 with all components except inventories contracting. New orders deteriorated to 45.3 from 50.8.

NZ BNZ PMI vs PSI - Employment

Source: MNI - Market News/BNZ/LSEG

FOREX: Asia FX Wrap - USD Consolidates

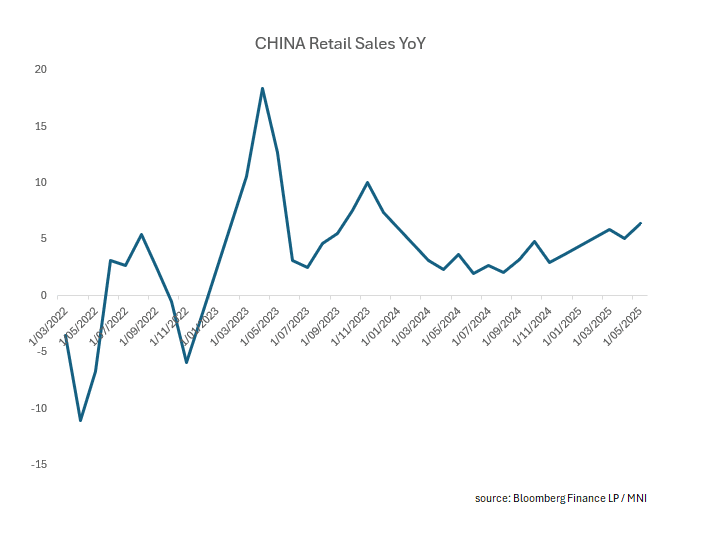

The BBDXY has had a range of 1202.92 - 1204.92 in the Asia-Pac session, it is currently trading around 1204. Japan and the EU plan to step up defense-industry cooperation, with officials and private-sector representatives set to meet Monday, Nikkei reported“(BBG). CHINA Retail Sales Strong with Urban Leading: The retail sales figures for May confirm the strength of the consumer that supports an improving domestic economy. Urban retail sales grew strongly, expanding by +6.5% whilst rural increased to +5.4%.

- EUR/USD - Asian range 1.1524 - 1.1548, Asia is currently trading 1.1535. EUR has rejected the move above 1.1600 but dips should continue to find demand, first support back towards the 1.1400 area then 1.1100/1200. EUR/USD looked to have broken the pivotal 1.1500 area last week, this needs to be sustained to signal a larger move higher.

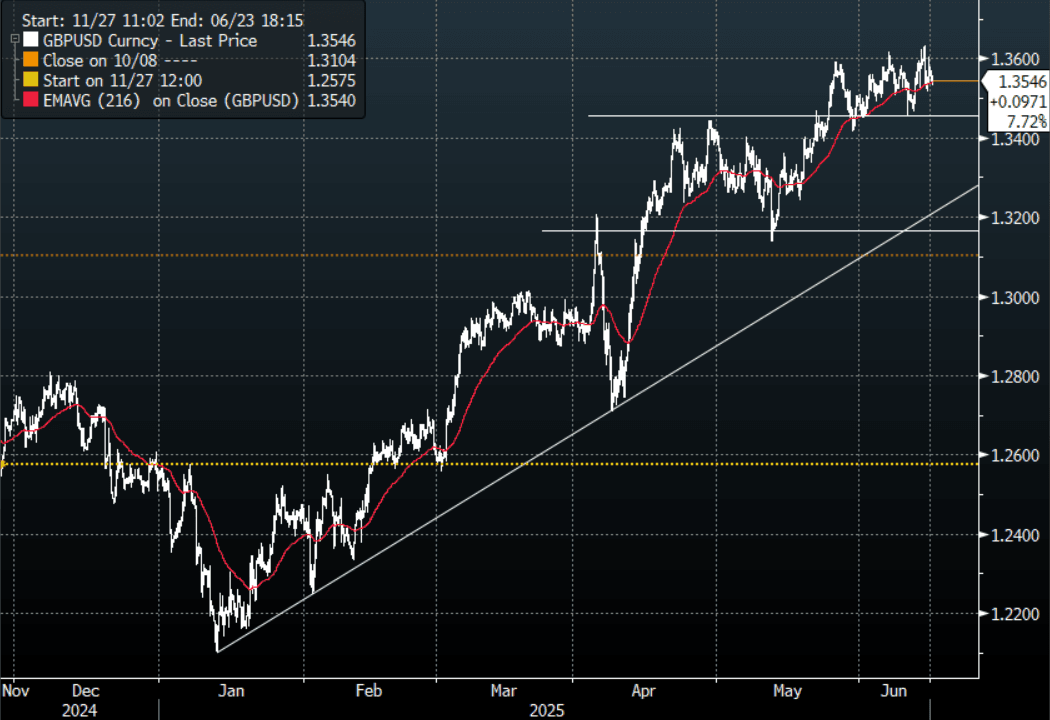

- GBP/USD - Asian range 1.3535 - 1.3567, Asia is currently dealing around 1.3545. The GBP looks to have failed to hold onto its upward momentum as it attempts to sustain a break above its pivotal Weekly resistance. First support seen back towards 1.3400/50.

- USD/CNH - Asian range 7.1843 - 7.1904, the USD/CNY fix printed 7.1789. Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX +0.15%, Gold $3430, US 10-Year 4.425%, BBDXY 1204, Crude oil $73.80

Data/Events : Italy CPI, EZ Labour Costs

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: CAD Shorts Pared Last Week - Per CFTC

The CFTC positioning update from last Friday (for the week ending June 10) once again saw mixed trends.

- Leveraged investors trimmed net longs for both JPY and GBP. AUD shorts were modestly added too. In contrast, CAD shorts were trimmed by leveraged investors.

- In the asset manager space, investors also trimmed CAD shorts. Trimming of CAD shorts was the biggest relative positioning shift per CFTC last week. This of course came ahead of Friday's oil price surge after Israel launched strikes on Iran.

- For EUR, we saw little aggregate change across either leveraged investors or asset managers.

- For asset managers, the GBP position flipped to a net long last week. This is the first time the investor base has been long since Oct 2024.

Table 1: CFTC Weekly Positioning Change & Outright Position - By Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -7624 | 15691 | 1484 | 111404 |

| EUR | 2820 | -12535 | 33 | 344913 |

| GBP | -3946 | 42529 | 4895 | 3612 |

| AUD | -2340 | -21833 | -1268 | -33624 |

| NZD | 1074 | -7160 | 1245 | -17162 |

| CAD | 6789 | -36616 | 10120 | -57376 |

| CHF | 3341 | 6310 | -5588 | -36779 |

| MXN | -371 | -9972 | 2106 | 39357 |

Source: Bloomberg Finance L.P./CFTC/MNI

JPY: Asia Wrap - Tries Higher Finds Offers Back Towards 145.00 Again

The Asia-Pac USD/JPY range has been 143.97 - 144.75, Asia is currently trading around 144.35. USD/JPY has been better bid for most of our session as US yields extend their move higher and US Equity futures turn positive again after initially trying lower.

- “Japan and the EU plan to step up defense-industry cooperation, with officials and private-sector representatives set to meet Monday, Nikkei reported.”(BBG)

- The BoJ is expected to keep its policy rate unchanged at 0.50% at its June 16-17 meeting. The key area of interest will be Governor Kazuo Ueda's post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes. If the BoJ begins to hint at stronger underlying inflationary trends or shows greater optimism about the economy, it could stoke expectations of a rate hike in the autumn.

- "JAPAN, US LEADERS ARRANGING TO MEET ON 17TH: KYODO" - BBG

- USD/JPY held its support back towards the 142.00 area once more, with oil surging again and US yields bouncing this pair has drifted back to the middle of its recent range.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. The larger interest around 145.00 looks to be rolling off tonight.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($4.87b). Upcoming Close Strikes : 143.00($692m June 18).

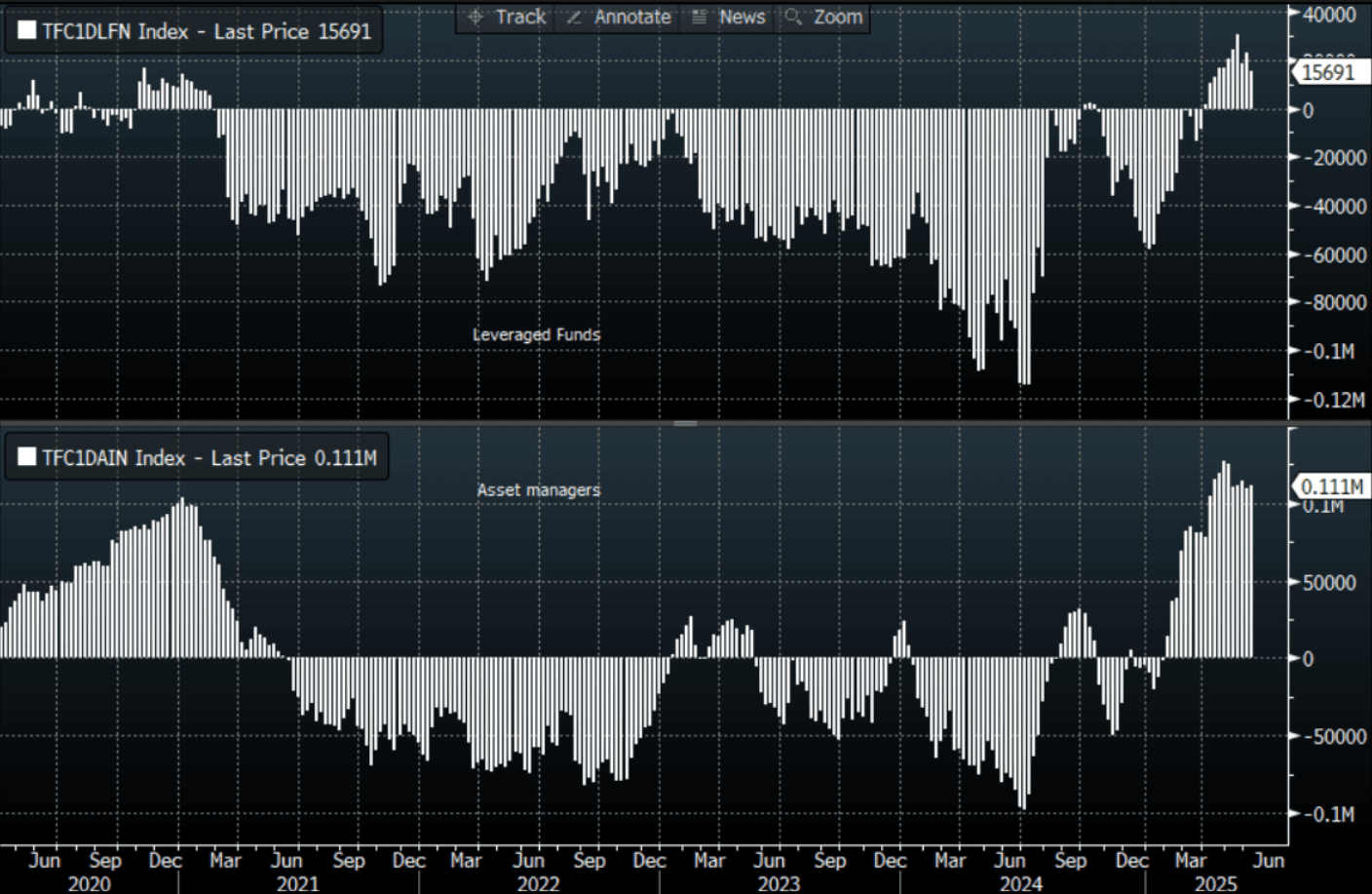

CFTC data shows Asset managers maintained their already extensive JPY longs, leveraged funds looked to have pared back their own longs once more.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

The AUD/USD has had a range of 0.6467 - 0.6496 in the Asia- Pac session, it is currently trading around 0.6475. The AUD has drifted a little lower for most of our session, -0.2%.

- Consensus Expects Labour Market Remained Tight In May. The highlight of the week, which doesn’t include many events, will be May jobs data. Bloomberg consensus is expecting that the status quo continued last month with Australia’s labour market remaining tight. A 20k rise in new jobs is forecast, in line with the 3-month average, with the unemployment and participation rates stable at 4.1% and 67.1% respectively.

- The AUD did well to hold above 0.6450 as risk came under pressure during the Friday session. The USD is still struggling to find any traction and as a result it still probably makes more sense to express any AUD weakness via the crosses until that changes.

- Price remains in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate.

- Expect buyers to continue to be around on dips while the support in the AUD/USD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6560(AUD549m), 0.6455(AUD476m). Upcoming Close Strikes : 0.6600(AUD 974m June 18)

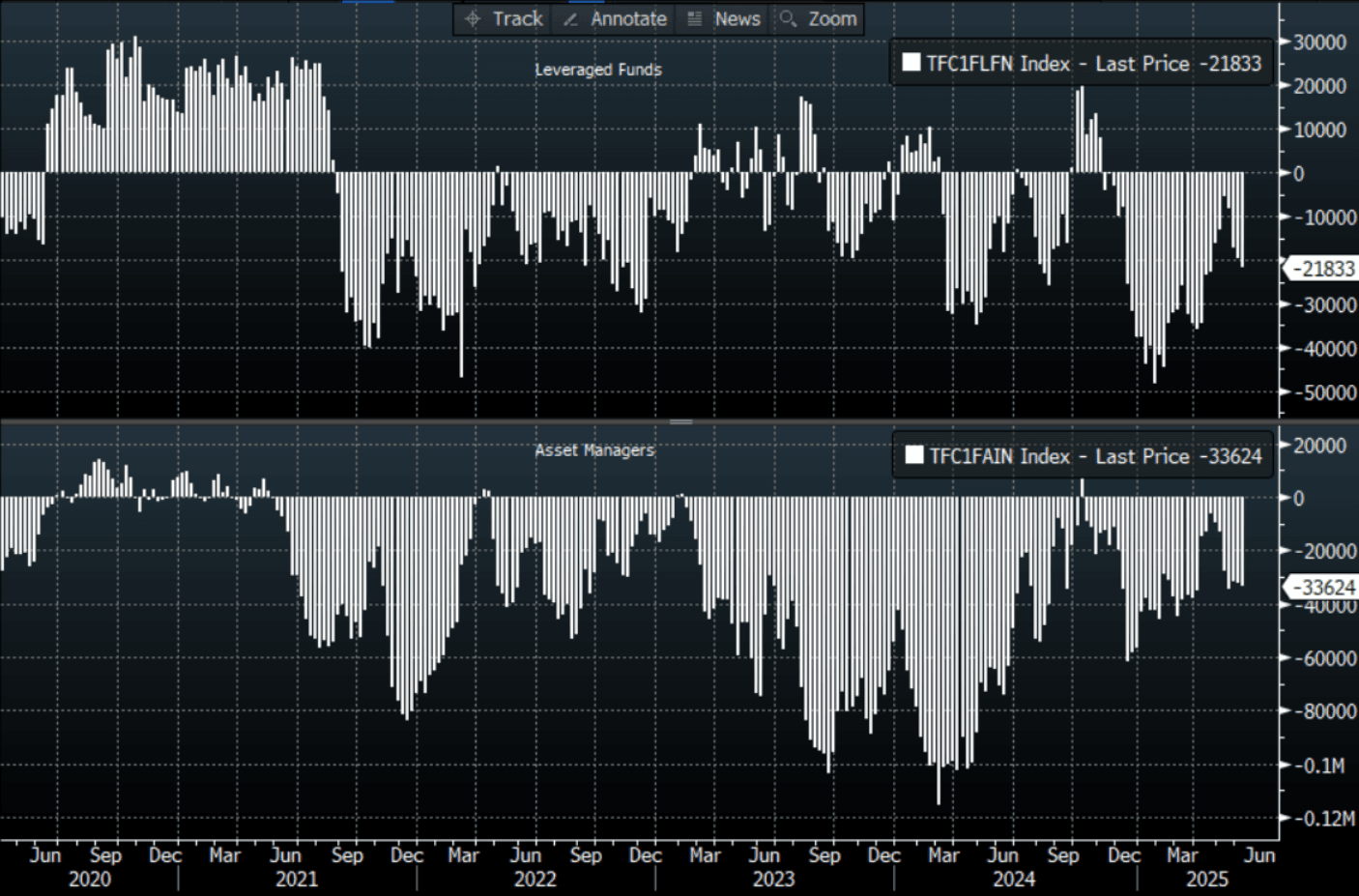

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to build up their shorts again.

AUD/JPY - Today's range 93.34 - 93.89, it is trading currently around 93.45. The price has topped out again towards 94.00 this morning after a big bounce off 92.50 overnight. A break back below 91.50/92.00 is needed to see the move lower regain momentum and the focus turn back to the year's lows again.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - Quiet Asian Session

The NZD/USD had a range of 0.6004 - 0.6026 in the Asia-Pac session, going into the London open trading around 0.6010. A very quiet session for the NZD, it continues to cling to its foothold above 0.6000.

- NZ Data - Slower Growth Expected But Inflation Eases To Band Mid-Point. The NZIER June survey of forecasters has been published and is showing a downward revision to NZ growth this financial year and next compared with the March results. FY25 is down 0.3pp to 1.1% and FY26 0.2pp to 1.9%, the recovery remains in place supported by lower rates.

- BNZ Indices Signal Economic Slowdown & Job Shedding. BNZ’s manufacturing and services PMIs both deteriorated in May and are below the breakeven-50 level and senior economist Steel warned that they are consistent with a return to a recession. With rates now in the “neutral zone” and the RBNZ Governor Hawkesby saying the MPC doesn’t have a bias, it looks like the RBNZ will be on hold on July 9 as it waits for more data, but it does monitor these indices and they suggest that the meeting will be “live”.

- The USD’s muted reaction to the events on Friday have the market again questioning the role it has as a safe haven ?

- The NZD continues to find solid support around the 0.6000 area. The upward momentum though has stalled for now and the market will be watching if risk can continue to hold up as impressively as it did on Friday night.

- While the support around 0.5850 holds in NZD/USD there should be buyers around on dips. A clear break above 0.6050/0.6100 and the move could start to accelerate.

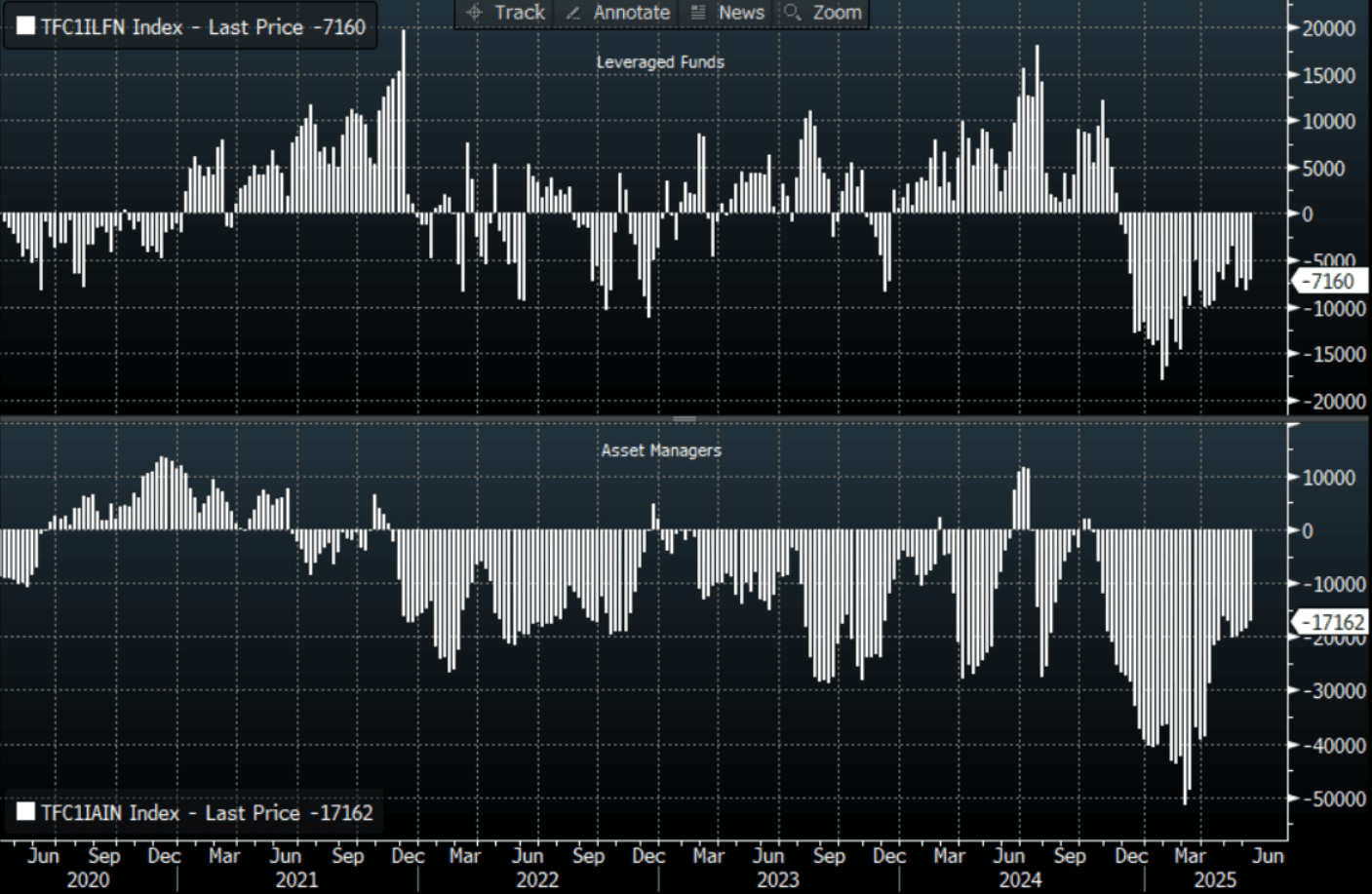

- CFTC Data showed Asset managers paring back their shorts slightly over the week, the leverage community did likewise.

AUD/NZD range for the session has been 1.0761 - 1.0798, currently trading 1.0770. A top looks in place now just above 1.0900, the cross topped out last week towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD CFTC Data

- Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Major Markets Mixed with KOSPI Leading

Despite the Israel - Iran conflict driving volatility across financial markets, there was an even mix of results across major Asian bourses today with the KOSPI one of the best performers. China's bourses struggled as data released showed the struggle for housing continues.

- The Hang Seng was down -0.12% and remains lower over the last week. The CSI 300 followed its lead, lower by -0.06%. The Shanghai Comp struggled into positive territory rising +0.05% and Shenzhen was the best performer rising +0.34% yet too remains lower over the last week.

- The KOSPI is strong, up over 1% as is the best performer of the major bourses over the last week.

- The FTSE Malay KLCI is down -0.27% and the Jakarta Composite flat.

- The FTSE Straits Times in Singapore is lower by -0.30% and the PSEi in the Philippines lower by -0.56%.

- Having finished Friday down -0.68%, the NIFTY 50 in India is eking out gains Monday rising by +0.20%

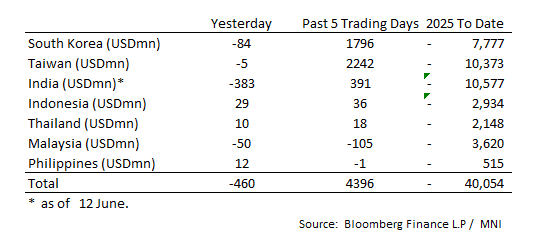

ASIA STOCKS: Large Outflow for India Thursday

Large inflows across major markets was the theme last week, despite India seeing large outflow on Thursday and flows tapering off on Friday for other markets.

- South Korea: Recorded outflows of -$84m Friday, bringing the 5-day total to +$1,796m. 2025 to date flows are -$7,777. The 5-day average is +$359m, the 20-day average is +$184m and the 100-day average of -$85m.

- Taiwan: Had outflows of -$5m as of Friday, with total inflows of +$2,242 m over the past 5 days. YTD flows are negative at -$10,373. The 5-day average is +$448m, the 20-day average of +$63m and the 100-day average of -$112m.

- India: Had outflows of -$383m as of the 12th, with total inflows of +$391m over the past 5 days. YTD flows are negative -$10,577m. The 5-day average is +$78m, the 20-day average of -$24m and the 100-day average of -$86m.

- Indonesia: Had inflows of +$29m Friday, with total inflows of +$36m over the prior five days. YTD flows are negative -$2,934m. The 5-day average is +$7m, the 20-day average +$14m and the 100-day average -$29m.

- Thailand: Recorded inflows of +$10m as of Friday, with inflows totaling +$18m over the past 5 days. YTD flows are negative at -$2,148m. The 5-day average is +$4m, the 20-day average of -$23m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$50m as of Friday, totaling -$105m over the past 5 days. YTD flows are negative at -$3,620m. The 5-day average is -$24m, the 20-day average of -$28m and the 100-day average of -$24m.

- Philippines: Saw inflows of +$12m yesterday, with net outflows of -$1m over the past 5 days. YTD flows are negative at -$515m. The 5-day average is $0m, the 20-day average of -$15m the 100-day average of -$5m.

OIL: WTI Continues to Rise as Brent Moderates

- Supply concerns are driving oil prices higher as the Israel-Iran conflict continues to escalate and fears rise on the possibility that Iran could block the Straits of Hormuz.

- The Straits of Hormuz sees 30% of oil shipped by sea transiting through it.

- WTI is up +1.05% today at US73.93 bbl in the Asia trading day.

- Brent has given back some of Friday’s gains and is down by -0.17% at US$75.06 bbl.

- WTI rose 7.6% to $73.18 bbl on Friday after reaching a high of $77.62 early in APAC trading. It is now up 24.6% this month.

- Brent was 8.4% higher at $75.18 bbl but off the intraday high of $78.50 and has started today up 3.4% to about $76.74 after rising to $78.32 initially. It is around 22% higher in June. The bull cycle remains in play and Friday’s intraday high is now initial resistance. Technicals are signalling that the trend is currently in an extreme overbought position.

- Abu Dhabi National Oil Co. “Adnoc” has made an $18bn bid for Australian fossil fuel producer Santos Ltd. to expand its footprint in the liquefied natural gas market.

- The bid represents a premium over over 25% to Santos' closing price on Friday, and the company's board intends to unanimously recommend the bid to shareholders.

GOLD: Off Earlier Highs, But Uptrend Remains Intact

Gold made highs of $3451.31 in the first part of trade, but we sit lower now, last back close to $3431, down slightly from end levels last week. Early gains were driven by the spike in oil from the open, which contributed to softer US equity futures. Sentiment has stabilized somewhat though, with US equity futures back modestly in the green. The USD has also ticked up against the majors, likely providing an additional headwind to gold.

- Still, recent gains reinforce the bullish trend with the bull trigger at $3500.1. Moving average studies are in a bull mode and highlight a dominant uptrend. Further risk off episodes can't be ruled out, with the on-going Israel-Iran conflict.

- Continued pessimism towards the USD should also support gold demand.

- On the downside, note the following support: $3325.3/3249.9 - 20- and 50-day EMA.

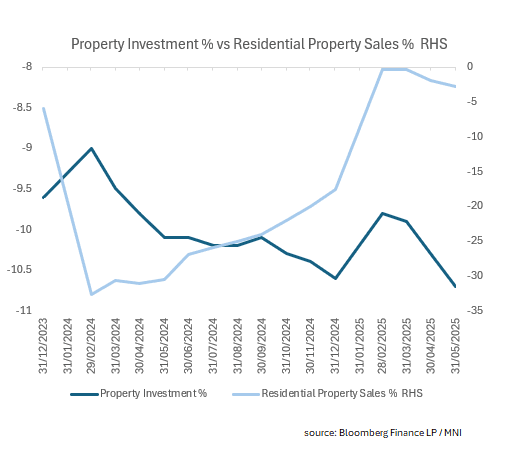

CHINA: Property Data Turns Down Again

- As new and used home prices (ex Shanghai) continue in their deflationary spiral, other data is showing signs of turning downwards after periods of improvement.

- China's Residential Property Sales and Property Investment YTD turned down again in May.

- Residential Property sales YTD YoY fell -2.8% (from -1.9% in April), the worst result this year.

- Property Investment YTD YoY declined -10.7% in May, from -10.3% in April and the worst result in over five years.

- There has been speculation as to the need for further policy stimulus with bond markets rallying post the data release.

CHINA: Retail Sales Strong with Urban Leading

- The retails sales figures for May confirm the strength of the consumer that supports an improving domestic economy.

- Urban retail sales grew strongly, expanding by +6.5% whilst rural increased to +5.4%.

- Strong expansion in household electronics which expanded by +53%

- Online retail sales jumped +8.5% YoY

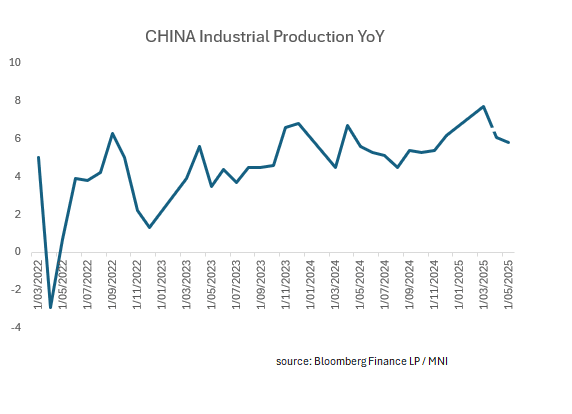

CHINA: Industrial Production Expands +5.8% YoY in May

- For a second consecutive month, China's industrial production grew less than the prior month.

- Peaking in March just prior to the implementation of tariffs at +7.7% May's result was lower at +5.8%.

- The 3 year average for Industrial Production expansion is +4.5%

- Mining was flat on last month at +5.7%.

- Manufacturing was lower at +6.2% (from +6.6%)

- Auto manufacturing rose by +11.2%

SOUTH KOREA: Country Wrap: Extra Budget Expected Soon

- The government soon plans to announce an additional extra budget bill worth at least 20 trillion won (US$14.6 billion) to spur domestic consumption and support the economic recovery, officials said Sunday. The Ministry of Economy and Finance was in the final stages of drafting the second supplementary budget plan, according to the officials familiar with the matter. The envisioned budget will likely include a cash handout program to support the livelihoods of the people, along with support measures utilizing local currency vouchers. (source Yonhap)

- Housing prices in Seoul are showing signs of overheating, and the new government is in a situation where it has to review regulatory cards as soon as it is launched. The market's attention is drawn to the government's announcement that it will "cover up all available policy measures." Attention is focusing on whether policies to curb demand for purchases, such as expanding regulatory areas and strengthening loan regulations, and ways to expand supply, such as designating new housing sites in the Seoul metropolitan area, will be evenly prepared. (source MAEIL)

- The KOSPI is strong, up over 1% as is the best performer of the major bourses over the last week.

- The Won is one of the best regional performers up +0.15% at 1,361.20

- Bonds are higher in yield though have taken back some of earlier losses. At one point the 10YR was almost +6bps higher but is now +4bps higher at 2.86%

ASIA FX: CNH Little Changed Post Data, USD/KRW Upticks Sold

In North East Asia, USD/CNH is little changed post mixed May activity data. USD/KRW is off earlier highs, while USD/TWD found support ahead of 29.50. USD/HKD remains close to the top end of the peg band.

- USD/CNH last tracked close to 7.1860, down slightly for the session. This has outperformed slightly stronger trends seen for the USD against the majors (BBDXY +0.13%). The pair remains comfortably within recent ranges. Earlier data showed renewed weakness in house prices, whilst May activity figures were mixed. Retail sales showed better trends, but IP slowed modestly. Fixed asset investment also moderated, with property related indicators on the activity side not showing much improvement. China equities are little changed in the first part of Monday trade.

- Spot USD/KRW was firmer in the first part of trade, but topped out at 1368.55. We last tracked near 1363.50, little change versus end Friday levels in the pair. Onshore equities have been supported on dips, the Kospi back above 2900, +1% firmer.

- USD/TWD was weaker in the first part of trade but couldn't test sub 29.50, which marked Friday lows in the pair. There may be some support around this region, given a fresh break lower would be multi year lows in USD/TWD. Still, this looks to be the main risk for the pair. We were last near 29.60, up around 0.15% in TWD terms for the session.

- USD/HKD is little changed, holding close to 7.8500 so far today.

ASIA FX: Peso Underperformance Continues, Steady Trends Elsewhere

In South East Asia FX, outside of a PHP fall, trends have been relatively steady to start the week. Equity trends are mixed, with Thailand weakness the one notable standout.

- The Philippines peso is comfortably the worst EM Asia FX performer since oil prices surged on Friday as the Israel-Iran conflict commenced. The pair is up 0.55% so far today, last near 56.49. Earlier session highs were at 56.57. The firmer oil price backdrop has weighed on PHP, with the pair now above its 50-day EMA resistance. Unlike elsewhere in the region, PHP doesn't have a positive trade surplus to help offset the spike in oil prices.

- USD/THB is a touch higher, last in the 32.45/50 region, which is still close to recent lows. Crossing the wires has been comments from Thailand's Commerce Ministry stating the desire for a weaker currency (37-38 versus the USD) per Rtrs. The comments were were added that the next BoT Governor should make baht weaker.

- USD/MYR was last near 4.2440, little changed for the session, while USD/SGD was under 1.2820, also relatively steady.

- USD/IDR is holding close to 16300 so far in Monday trade.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 16/06/2025 | 0800/1000 | *** | HICP (f) | |

| 16/06/2025 | 1030/1230 | ECB Cipollone At Osservatorio Banca Impresa 2030 Meeting | ||

| 16/06/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/06/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 16/06/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 17/06/2025 | 0600/0800 | ** | Unemployment | |

| 17/06/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production |