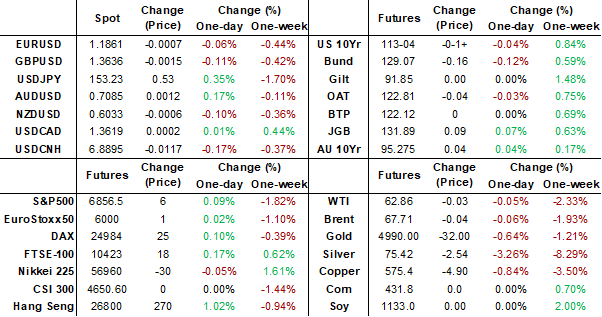

MNI EUROPEAN MARKETS ANALYSIS: USD/JPY Edges Back Above 153.00

- Japan Q4 GDP rose, but was not as strong as forecasts, with key components in terms of consumption and business spending managing only marginal increases. NZ Data was mixed with card spending figures dipping, while the services PMI remained above the expansion point.

- Otherwise, it was a quiet start for Asia Pac markets, with a number of countries already out for the lunar new year, including China. A US holiday later also means that there has been no cash US Tsy trading.

- In the FX space, USD/JPY is a little higher, but under Friday highs. USD/CNH has tested under 6.8900, even with onshore markets out (Hong Kong doesn't start the LNY break until tomorrow).

MARKETS

US TSYS: Bond Market Awaits FED Minutes as CPI Miss Raises Cut Hopes

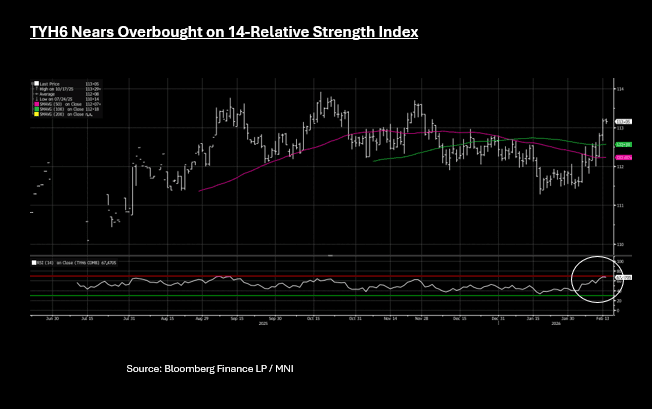

An unsurprisingly quiet day in US bond futures given much of Asia out and US on holiday Monday (no cash trading). The US 10-Yr future had a modest amount of volume for a quiet day and traded in a range of 113-03 to 113-07+. Currently at 113-05 sees TYH6 flat on the day.

The run up in bonds last week has the TYH6 consolidate above all major moving averages and nearing overbought on the 14-day relative strength index. This suggests that in the short term (as markets await FED minutes) further rallies could be capped.

- A push pull last week for bonds with strong employment data followed by a weaker January CPI reigniting rate cut hopes. Headline CPI / core were below expectations albeit with some (very modest) signs of early stage inflation in the detail. Rate cut expectations remain muted with a full rate cut not priced in until July and -63bps by year end.

- FED minutes are out this week and will be watched for any signs of discussion on raising the bar for rate cuts.

Cash unsurprisingly finished Friday strong with yields lower across the curve and curves flatter.

For the week last week:

- The 2-Yr finished at 3.41% - down 9.9bps

- The 5-Yr finished at 3.606% - down 15.4bps

- The 10-Yr finished at 4.05% - down 15bps

- The 30-Yr finished at 4.697% - down 15.6 bps

JGBS: Twist-Steepener Leaves YC Hovering At Bottom Of Range

JGB futures are stronger, +10 compared to settlement levels, but off session bests.

- MNI AU - Japan Q4 GDP Edges Up But Barely Positive, Key Drivers Close To Flat: The data showed Japan's economy only grew marginally in Q4 last year, signalling more needs to be done to boost economic growth, which is a key goal for the Takaichi regime. From a BoJ standpoint, it shouldn't add to near term expectations around tightening.

- The US is out today for the Presidents' Day Holiday.

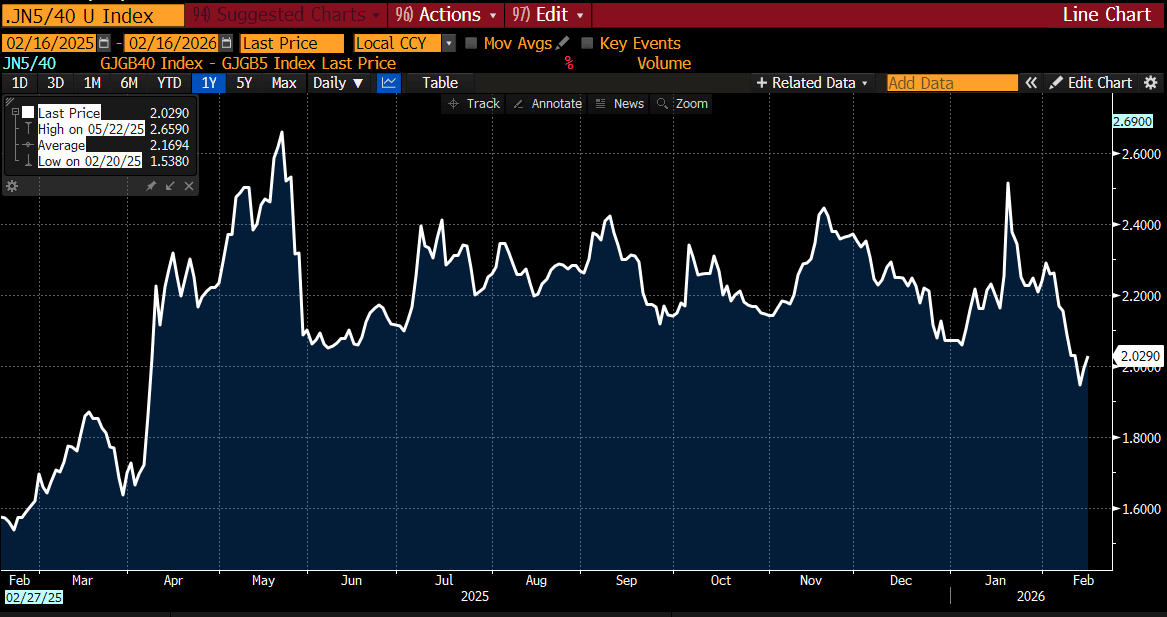

- Cash JGBs have twist-steepened across benchmarks, with yields 1-2bps lower out to the 10-year and 2-3bps higher beyond.

- After reaching a record steepness in mid-January, the 2/40 yield curve tested on Friday the lower bound of the well-defined range that has contained price action since mid-year.

- Notably, while the 2/5 segment has flattened, it was the 5/40 curve which broke through the bottom of the range on Friday, albeit retesting the breakdown level today.

- Swap rates are 1bp lower to 6bps higher, with a steepening bias.

- Tomorrow, the local calendar will see Tertiary Industry Index data alongside 5-year supply.

Source: Bloomberg Finance LP

JAPAN DATA: Q4 GDP Edges Up But Barely Positive, Key Drivers Close To Flat

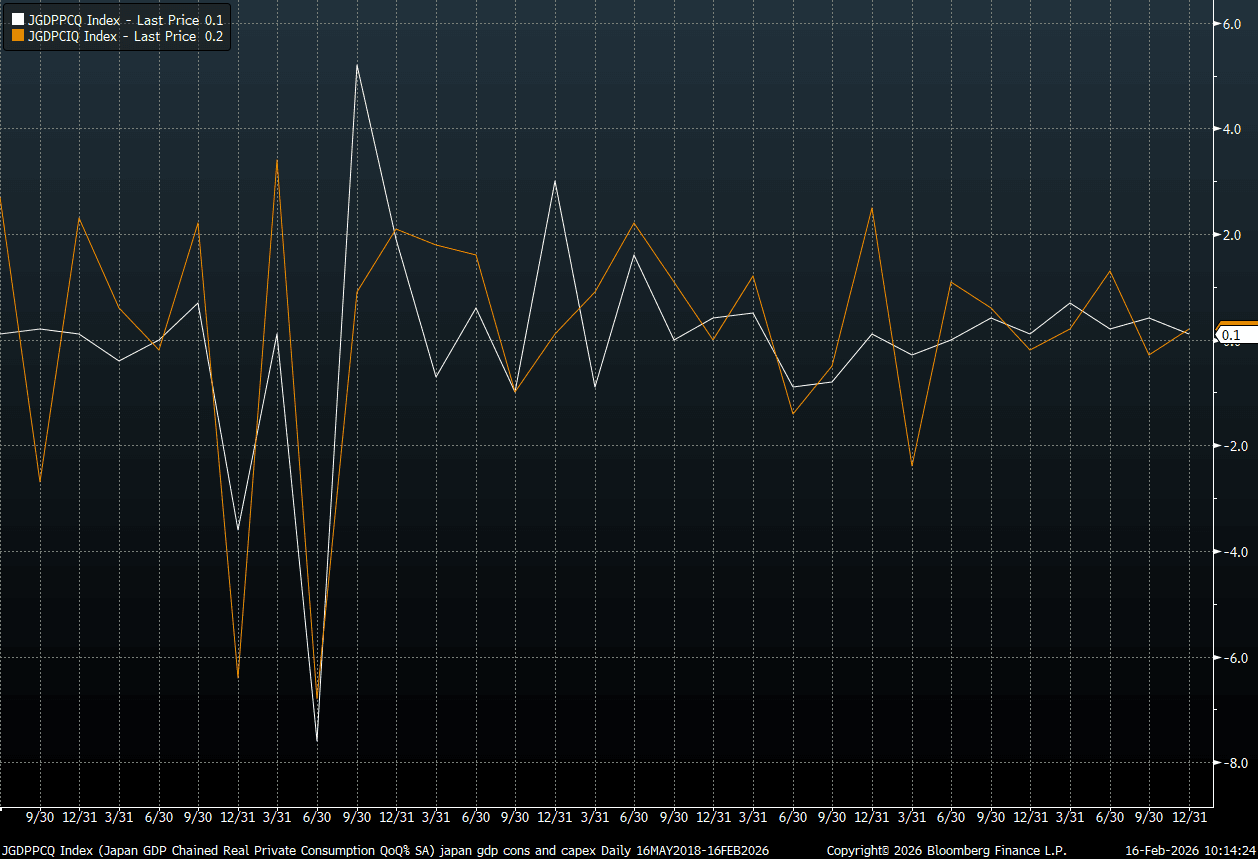

Q4 GDP in Japan was below market forecasts, printing at 0.1%q/q versus 0.4% forecast. The Q3 contraction was revised to -0.7%q/q (originally reported as -0.6%). In annualized terms we rose 0.2%q/q in Q4, versus 1.6% forecast and against a 2.6% decline in Q3. Nominal GDP rose 0.6%q/q, against a 1.0% forecast and flat outcome in Q3. Consumption was in line with forecasts, up 0.1%q/q, but business spending, and the net inventory and net export contributions were below market expectations. The data showed Japan's economy only grew marginally in Q4 last year, signalling more needs to be done to boost economic growth, which is a key goal for the Takaichi regime. From a BoJ standpoint, it shouldn't add to near term expectations around tightening.

- Real GDP was up only 0.1% in y/y terms for Q4. This is the weakest result since the first half of 2024 (when the economy was in contraction mode). Domestic demand rose 0.9%y/y (but was flat in the q/q terms), while private demand rose 1.3%y/y, (+0.1% in q/q terms).

- Private consumption rose 0.1%q/q after a revised 0.4% gain in Q3 (originally reported as up 0.2%).

- Business spending was up 0.2%q/q, against a 0.6% forecast (and revised 0.3% fall in Q3). Net inventories took -0.2ppts off growth (-0.1ppts was forecast), while the net export contribution was flat against a +0.1ppt forecast.

Fig 1: Japan Private Consumption (White Line) & Business Investment (Orange Line) Close To Flat Q/Q

Source: Bloomberg Finance L.P./MNI

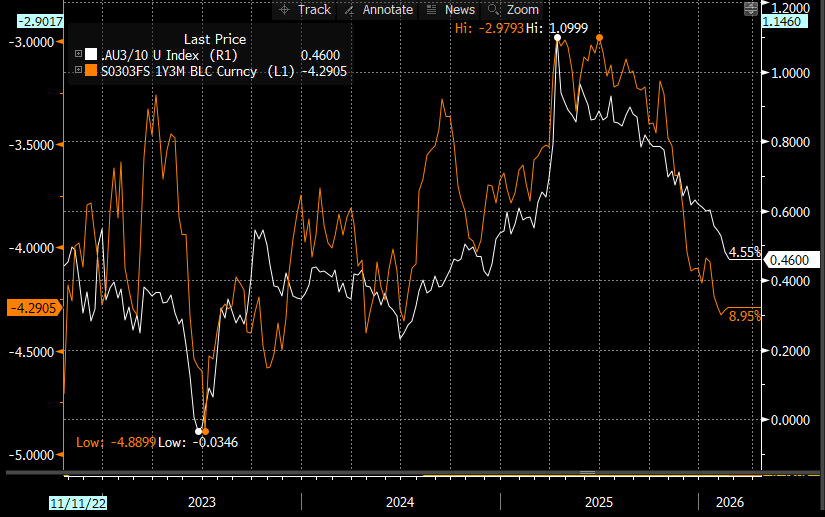

AUSSIE BONDS: Curve Continues To Flatten In Line With Expected Cash Rate

ACGBs (YM +2.0 & XM +4.5) are stronger after dealing in relatively narrow ranges in today’s session.

- Cash US tsys are out today for the Presidents' Day Holiday.

- Cash ACGBs are 2-4bps richer with the 3/10 curve flatter. At 46bps, the curve sits at its flattest since late 2024, some 70bps below its April high. The move has been consistent with the dramatic reversal for market expectations for the RBA policy rate 12-months forward (see chart).

- The bills strip is slightly richer, with pricing flat to +2.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 91% by June and 141% by December 2026.

- Tomorrow, the local calendar will see the RBA Minutes of Feb. Policy Meeting. The Q4 Wage Cost Index is due for release on Wednesday with the January Employment on Thursday.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond on Wednesday and A$800mn of the 3.25% 21 April 2029 bond on Friday.

Bloomberg Finance LP

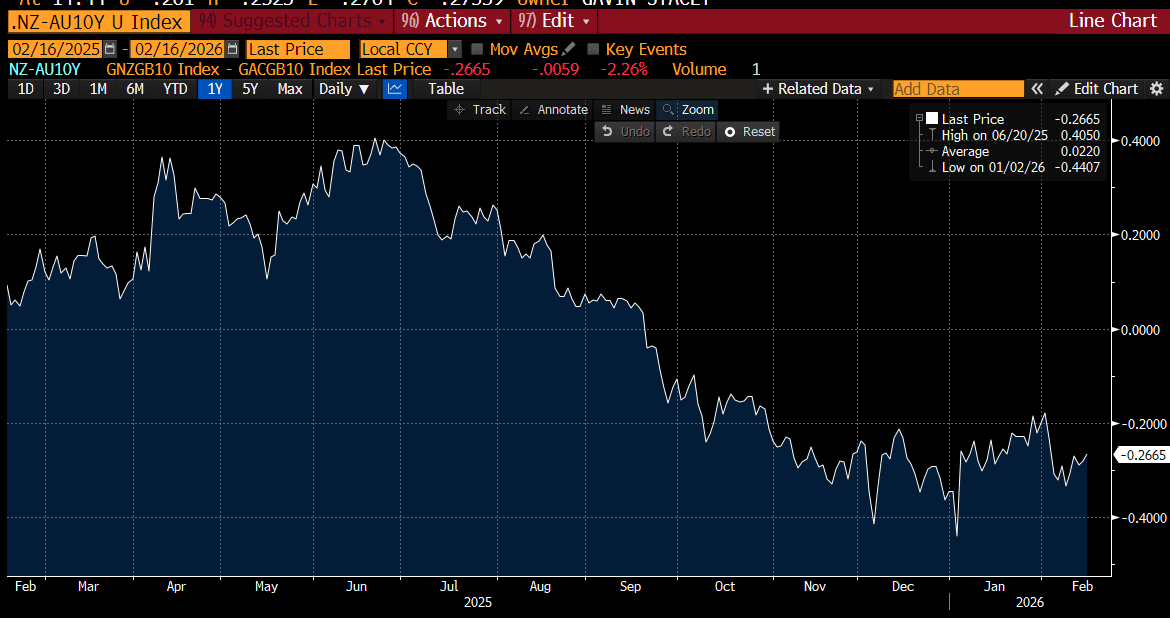

BONDS: NZGBS: Richer, PSI Holding Firm, RBNZ Policy Decision On Wed

NZGBs closed 3bps richer across benchmarks, with the NZ-AU 10-year yield differential little changed at -26bps.

- Cash US tsys are out today for the Presidents' Day Holiday.

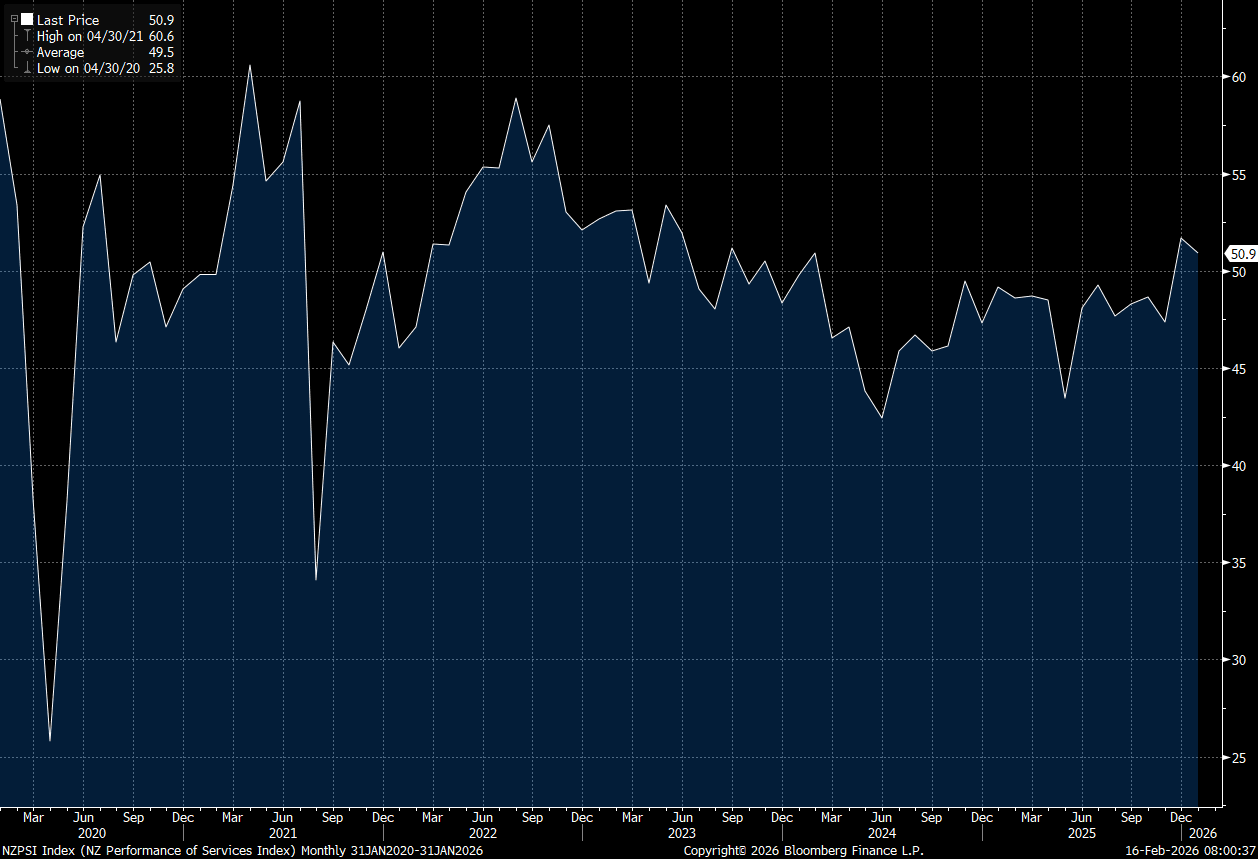

- The NZ Jan Performance of Services Index eased off Dec highs to 50.9. The Dec reading was revised up a touch to 51.7 (originally reported as a 51.5 outcome). That outcome was the firmest print since the first half of 2023. The index spent much of 2024 and 2025 sub 50.0, so in contraction territory before recovering. 2023 highs in the index were near 59.0, so whilst the index has recovered it isn't suggesting a return to the heady growth periods of 2021/2022.

- RBNZ published the Q1 Household Expectations Survey results, with mean expected inflation in two years at 3.4% down from 4.3% in Q4. Mean expected inflation in one year was 5.2% down from 5.5% in Q4.

- Swap rates closed 3bps lower.

- RBNZ-dated OIS pricing closed slightly softer across meetings. No tightening is priced for this week, while December 2026 assigns 40bps.

- Tomorrow, the local calendar will see Food Prices ahead of PPI data and the RBNZ Policy Decision on Wednesday.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 4.50% May-35 bond.

Bloomberg Finance LP

NEW ZEALAND: Services Index Edges Off Dec Highs, Activity Sub Index Improves

The New Zealand Jan Performance of Services Index eased off Dec highs to 50.9. The Dec reading was revised up a touch to 51.7 (originally reported as a 51.5 outcome). That outcome was the firmest print since the first half of 2023. The index spent much of 2024 and 2025 sub 50.0, so in contraction territory before recovering. 2023 highs in the index were near 59.0, so whilst the index has recovered it isn't suggesting a return to the heady growth periods of 2021/2022 (see the chart below of the headline index).

- The detail showed mixed trends across the sub indices. Firmer activity/sales, which rose to 54.2 from 52.5 in Dec. Employment edged down though to 49.1 from 49.6. New orders were 51.8 versus 52.7 prior as well.

Fig 1: New Zealand PSI, Edges Off Dec Highs

Source: Business NZ/Bank Of New Zealand/Bloomberg Finance L.P./MNI

NEW ZEALAND: Card Spending Further Unwinds Nov Bounce, Negative Y/Y

New Zealand Jan card spending figures showed further falls in total spending, down -0.7%m/m, after a revised 1.3% fall in Dec (originally reported as a -1.0% decline). Retail card spending fell -1.1% in Jan, after a -0.3% fall in Dec (also revised lower from the original -0.1% estimate). This continues to unwind the bounce in spending we saw in Nov last year (+2.1%m/m for total card spending and +1.3%m/m for retail spending). In y/y terms total card spending was -2.3% (versus -1.7% prior), while retail spend fell -0.6%y/y in Jan (versus -1.1% prior). At face value this data still points to a stop/start recovery pace in terms of consumer spending, although we often see volatility in the spending outcomes around the calendar new year period. Still, the central bank has time on its hands in terms assessing spending trends, particularly with the next move from the RBNZ seen as a hike.

- The detail was mixed, with services spending up 1.9%m/m in Jan, while weakness was seen in consumables, durables and fuel related spending.

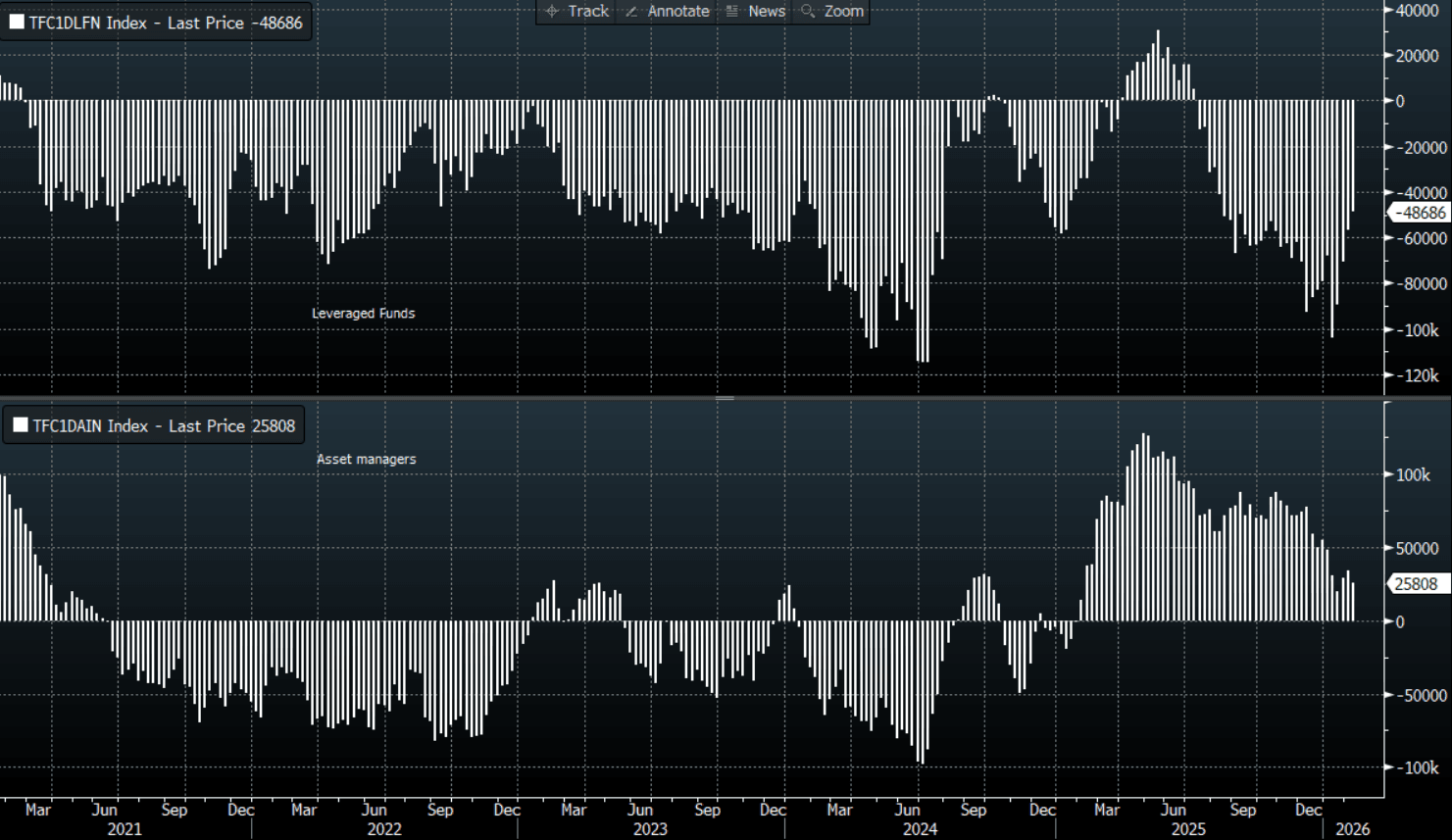

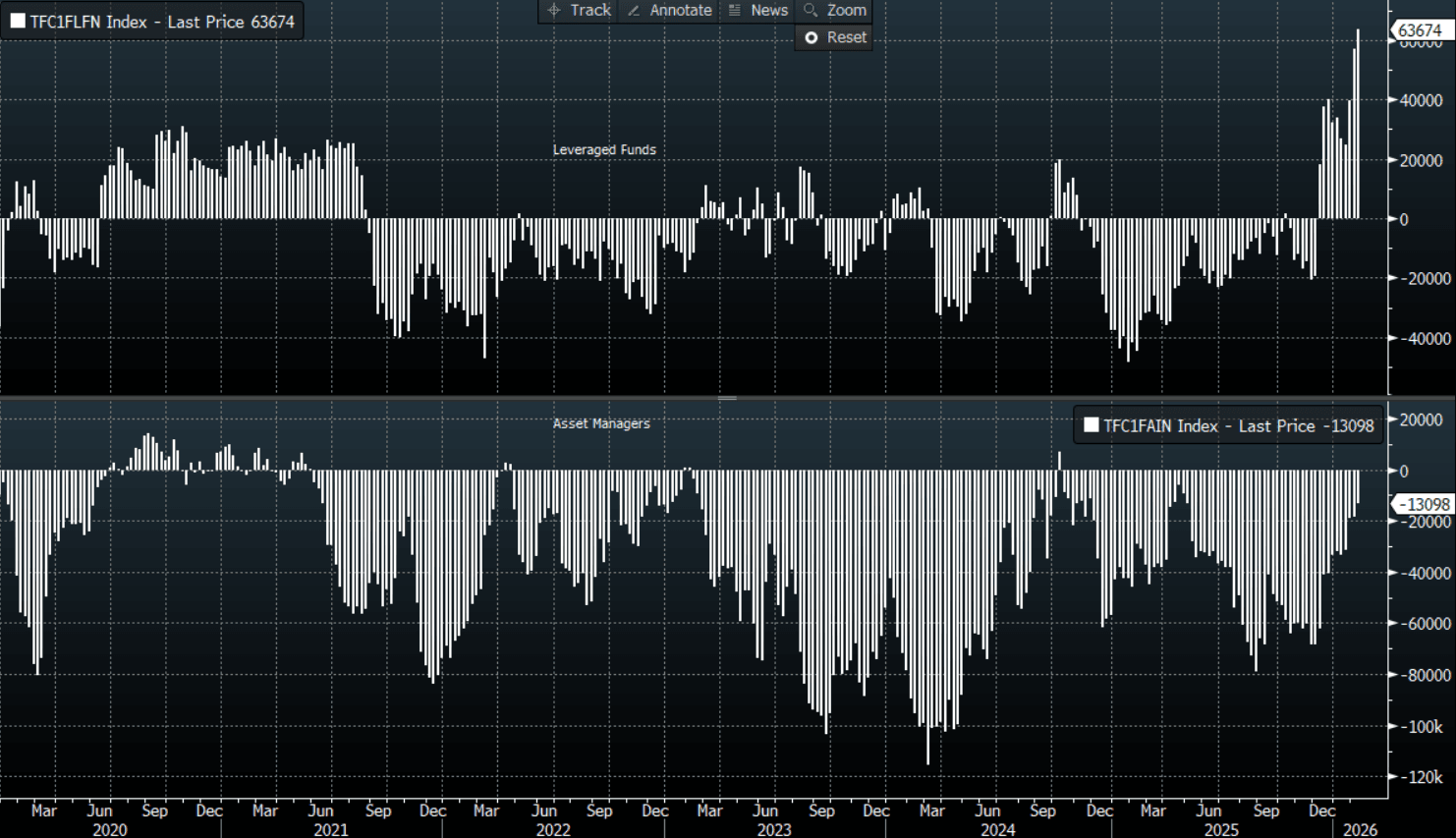

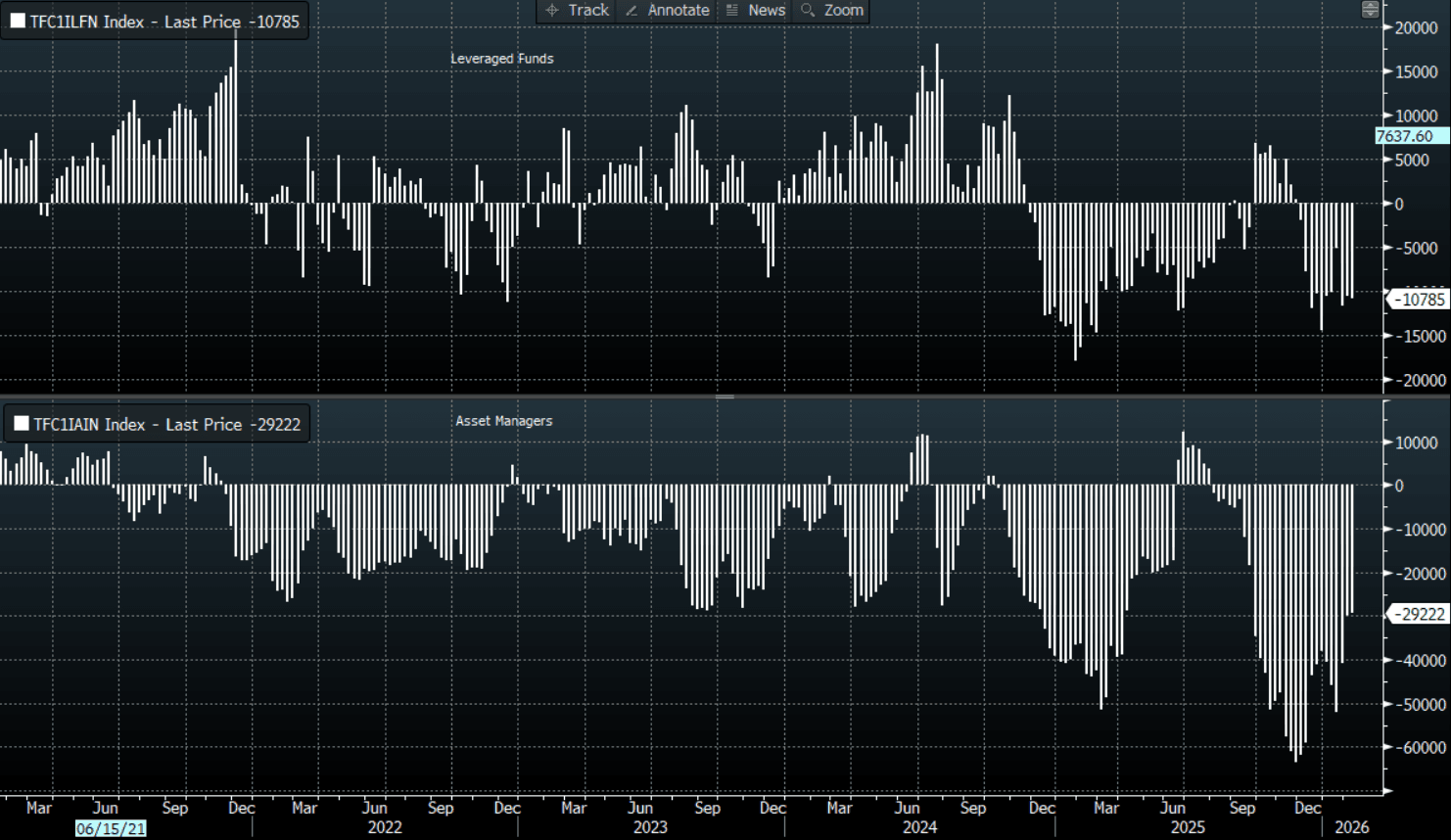

FOREX: Leveraged Contracts Sold USD, Asset Managers Mixed - CFTC

The weekly CFTC positioning update showed mixed trends between leveraged and asset manager contracts with respect to the USD. The leveraged contract bias was clearly against the USD. Only NZD and CHF saw modest net selling for leveraged contracts in the week ending Feb 10 (last Tuesday). In contrast, on the asset manager side, trends were more mixed, with JPY and GBP selling, but buying for EUR and AUD, along with CAD

- For USD/JPY, we didn't see a significant shift in net aggregate positioning, as net buying via leveraged contracts was largely offset by net selling in the asset manager space. Since mid Jan, the leveraged outright short has been roughly cut in half (from beyond -100k), while asset manager longs are down modestly. We may have seen a further curtailing in leveraged yen shorts as last week unfolded, given USD/JPY price action continued to correct off highs. Support for yen came via calming rhetoric from the Takaichi regime around the fiscal outlook (post the LDP's strong election victory), along with weaker US yields.

- Elsewhere, EUR/USD net longs were added to even as EUR/USD couldn't revisit late Jan highs above 1.2000.

- AUD/USD has the largest net longs in the leveraged space, while asset managers continued to cut back on shorts. The A$ is looking to consolidate its break above 0.7000.

Table 1: CFTC FX Positioning Update - Weekly Change & Outright Positioning (As At Feb 10)

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 8164 | -48686 | -7675 | 25808 |

| EUR | 2773 | 17308 | 11043 | 434334 |

| GBP | 2908 | 50127 | -8515 | -78360 |

| AUD | 6559 | 63674 | 5609 | -13098 |

| NZD | -188 | -10785 | 660 | -29222 |

| CAD | 3746 | -45706 | 8857 | 57948 |

| CHF | -853 | -911 | -1298 | -52570 |

| MXN | 1570 | 45945 | -1207 | 87146 |

Source: CFTC/Bloomberg Finance L.P./MNI

FOREX: USD - BBDXY Holds Below 1185-1187

The BBDXY has had a range today of 1181.54 - 1182.53 in the Asia-Pac session; it is currently trading around 1182. The USD stalled toward 1185 and drifted lower as US yields continued to price in rate cuts. Risk steadied itself and recency bias tends to dismiss it evolving into anything more. The market is very bearish the USD so if we should get some form of a deeper correction in risk and the USD finds demand as a hedge, the market is not positioned for this. On the day, the first resistance remains toward the 1185-1187 area and then 1195 where I suspect we could see sellers return. A sustained break below 1175-1180 is needed to potentially signal the start of another leg lower.

- EUR/USD - Asian range 1.1859-1.1878, Asia is currently trading 1.1865. The pair continues to trade sideways below 1.1900 albeit with a slightly heavy tone. Price action remains constructive, can it build a base above 1.1800 and then find the momentum to push on? On the day, the first support is back toward 1.1820-1.1840 and then the 1.1750 area. A sustained move back above 1.1925-1.1940 is needed to give it the thrust it needs to have another look toward the 1.2000 area.

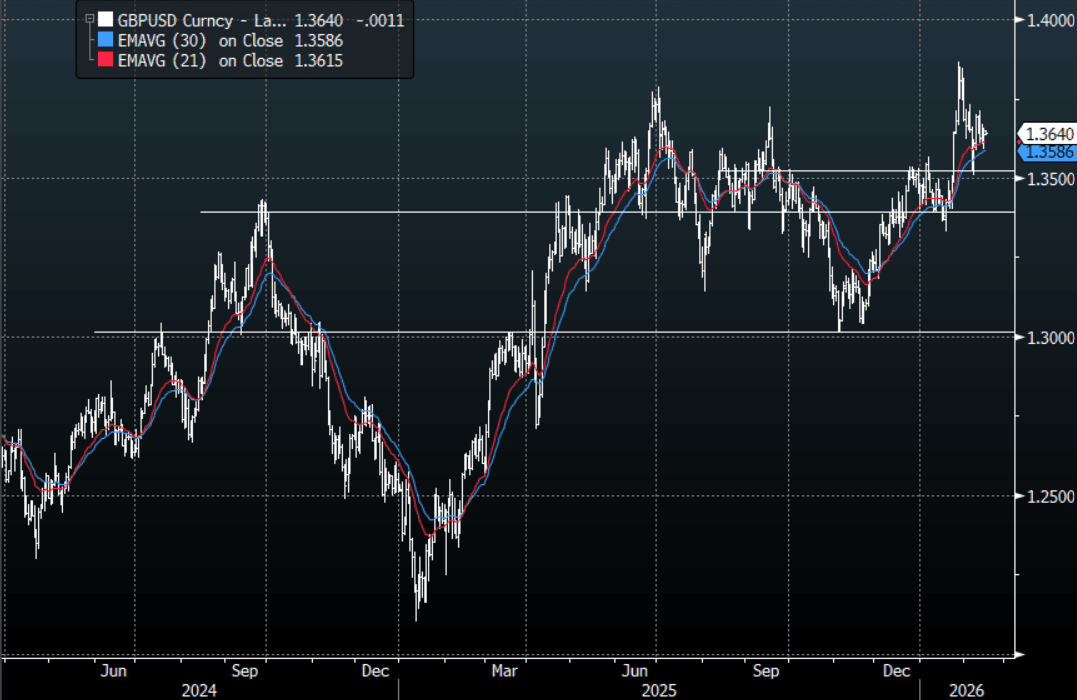

- GBP/USD - Asian range 1.3637-1.3650, Asia is currently dealing around 1.3640. GBP continues to look like 1.3580-1.3730 to me for now as we wait to see how the big USD trades when the US returns from its day off.

- Cross asset : SPX +0.20%, Gold $4975, US 10-Year 4.05%, BBDXY 1182, Crude Oil $62.76

- Data/Events : Germany Bloomberg Feb. Germany Economic Survey, Spain Bloomberg Feb. Spain Economic Survey, EZ Bloomberg Feb. Eurozone Economic Survey/Industrial Production, France Bloomberg Feb. France Economic Survey, Italy Bloomberg Feb. Italy Economic Survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Consolidating Around 153.00

The USD/JPY range today has been 152.64-153.16 in the Asia-Pac session, it is currently trading around 153.03, +0.22%. USD/JPY was faded on Friday night again on a bounce back toward 154.00 as US yields continued to extend lower after the US CPI. The headwinds for Yen shorts are growing and putting pressure on the leveraged funds. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone. On the day, the first resistance is back towards 153.50-154.00 and then the 155.00 area as the market pares back its overextended USD longs and looks for another base to form from which to potentially move higher again.

- MNI AU - Japan Q4 GDP Edges Up But Barely Positive, Key Drivers Close To Flat: The data showed Japan's economy only grew marginally in Q4 last year, signalling more needs to be done to boost economic growth, which is a key goal for the Takaichi regime. From a BoJ standpoint, it shouldn't add to near term expectations around tightening.

- CFTC Data up to 10/02/2026 shows Asset Managers still reducing their JPY longs, +25808(Last +33483). The Leveraged community continues to pare back their large shorts after the failure to extend higher, –48686(Last -56850).

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.90($545m), 154.40($599m), 155.00($518m). Upcoming Close Strikes : 153.00($2.68b Feb 19), 155.00($1.41b Feb 19),156.00($1.87b Feb 17) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 126 Points

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD/USD - Drifts Higher Thanks To CNH Strength

The AUD/USD has had a range today of 0.7057 - 0.7087 in the Asia- Pac session, it is currently trading around 0.7085, +0.15%. The AUD drifted higher in our day as USD/CNH came under pressure moving below 6.8900 with China out for Lunar New Year. With the US also out today I suspect it could be a very quiet start to the week. Crypto has started the week back under pressure so worth keeping an eye on. CFTC data shows leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is again back toward 0.7020-0.7050, a break below here could signal a deeper pullback as the 0.7100-0.7200 continues to cap the move higher, how risk holds up when the US returns will be a key factor.

- CFTC Data up to 10/02/2026 shows Asset managers continuing to pare back shorts, -13098(Last -18707). The Leveraged community was again adding to its longs, +63674(Last +57115). These longs will be looking for risk to stabilise in order to challenge 0.71-0.72.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7110(AUD360m). Upcoming Close Strikes : 0.6980(AUD694m Feb 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 63 Points

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Holding Above 0.6000 As Risk Steadies

The NZD/USD had a range today of 0.6013-0.6041 in the Asia-Pac session, it is currently trading around 0.6030, -0.15%. The NZD found demand back towards 0.6000 and this support will need to continue to hold if we are to get an eventual test of the 0.6100 area. Risk has stabilised for now and we should have a quiet start to the week with both the US and China out. On the day, the first support remains in the 0.5985-0.6015 area; a break below here could signal a deeper pullback toward 0.5900. For now the 0.6100 area continues to cap but the bulls will be hoping for risk to firm up to have another go

- MNI AU - NZ Card Spending Further Unwinds Nov Bounce, Negative Y/Y: At face value this data still points to a stop/start recovery pace in terms of consumer spending, although we often see volatility in the spending outcomes around the calendar new year period. Still, the central bank has time on its hands in terms of assessing spending trends, particularly with the next move from the RBNZ seen as a hike employment index printed at 52.9 (versus 53.7 prior), but we are above 2025 lows.

- (Bloomberg) - "The RBNZ Shadow Board recommends the Official Cash Rate should remain on hold at 2.25% this week, the NZ Institute of Economic Research says. "Members agreed that New Zealand's economic recovery is starting to gain traction, but there remains a considerable degree of spare capacity in the economy, while headline inflation has increased."

- "NZ Mean Household 2Y Inflation Expectations 3.4%: RBNZ Survey. Mean expected inflation in two years is 3.4% down from 4.3% in 4q. Median expected inflation rate in two years is 3%. Unchanged for eighth straight quarter." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD308m), 0.6050(NZD395m). Upcoming Close Strikes : 0.5700(NZD400m Feb18), 0.5860(NZD420m Feb 19), 0.6000(NZD308m Feb 19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 47 Points

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

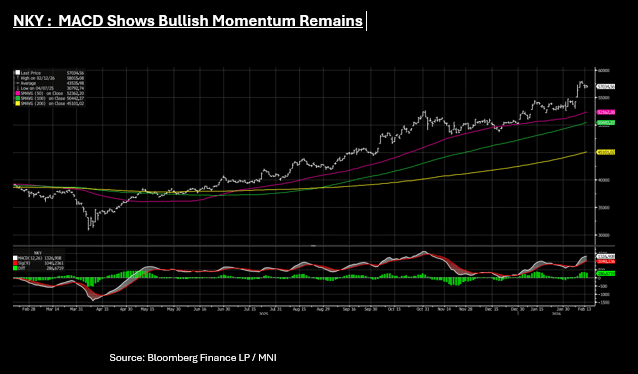

ASIA: NKY Regains from Losses Earlier After GDP Shock

With much of Asia closed Monday, all eyes were on the NIKKEI which had reached new highs early last week post election. The NKY posted modest gains early to reach 57,219 but gave back those gains following the weaker than expected Q4 GDP release. Japan's economy grew by a mere +0.2% YoY in 4Q, significantly missing the median forecast of +1.6%. This underscored persistent weaknesses in business spending and private consumption, dampening investor sentiment and sending the NKY to lows of 56,748. The NKY is staging a modest comeback in the afternoon session up +0.15% on the day.

The NKY remains up over 5% following the February 8 election and some investment houses now appear to be happy to lock in profits and wait for further clarity on policy. With expectations of further stimulus growing the next key data release is the January National CPI Friday and expectations are for a moderation from the December result. The momentum for the NKY remains positive with the MACD (white) line trending above the Signal (red) line, a bullish indicator. This suggests pullbacks could continue to see dip buyers emerge as hopes of stimulus support investor sentiment.

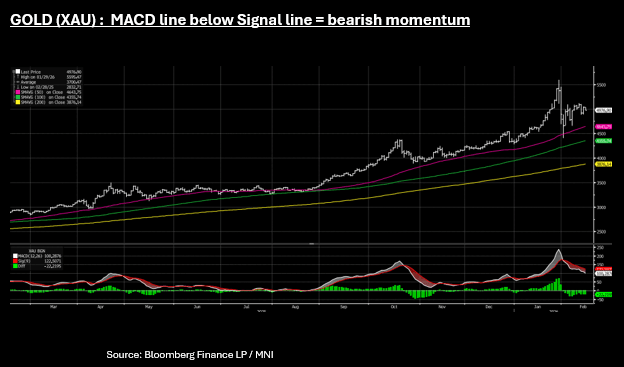

COMMODITIES: Oil Flat Ahead of US Iran Meeting, Gold Back Below $5,000

- With much of Asia out today oil markets were quiet, watching news flow from US Iran talks.

- A second round of nuclear negotiations between the US and Iran is to take place on Tuesday in Geneva. Discussions are expected to focus on a potential suspension of uranium enrichment for three to five years and the removal of highly enriched uranium from Iran in exchange for sanctions relief.

- Iranian officials stated Sunday that any agreement must include mutual economic benefits via joint investments in oil, gas, mining, and aircraft purchases. Iranian lawmakers have insisted they will not accept a total ban on enrichment or the transfer of their entire nuclear stockpile abroad.

- U.S. Secretary of State Rubio emphasized that Trump prefers a diplomatic settlement, even though he said Friday that regime change was the best outcome for Iran.

- WTI traded in a tight range Monday of $62.76 - $63.30, last near US$63.30 where it opened.

- Brent traded in a range of $67.62 - $68.13 and is at US$67.76 bbl, where it opened.

- Gold has given back some of Friday's gains Monday with falls of -1.2% and back below US$5,000 at US$4,974.75.

- Momentum indicators like the moving average convergence divergence (MACD) show that bearish momentum still remains, given the MACD (white) line remains below the Signal (red) line. This could limit rallies in the short term until the after shocks of the sell off are no longer.

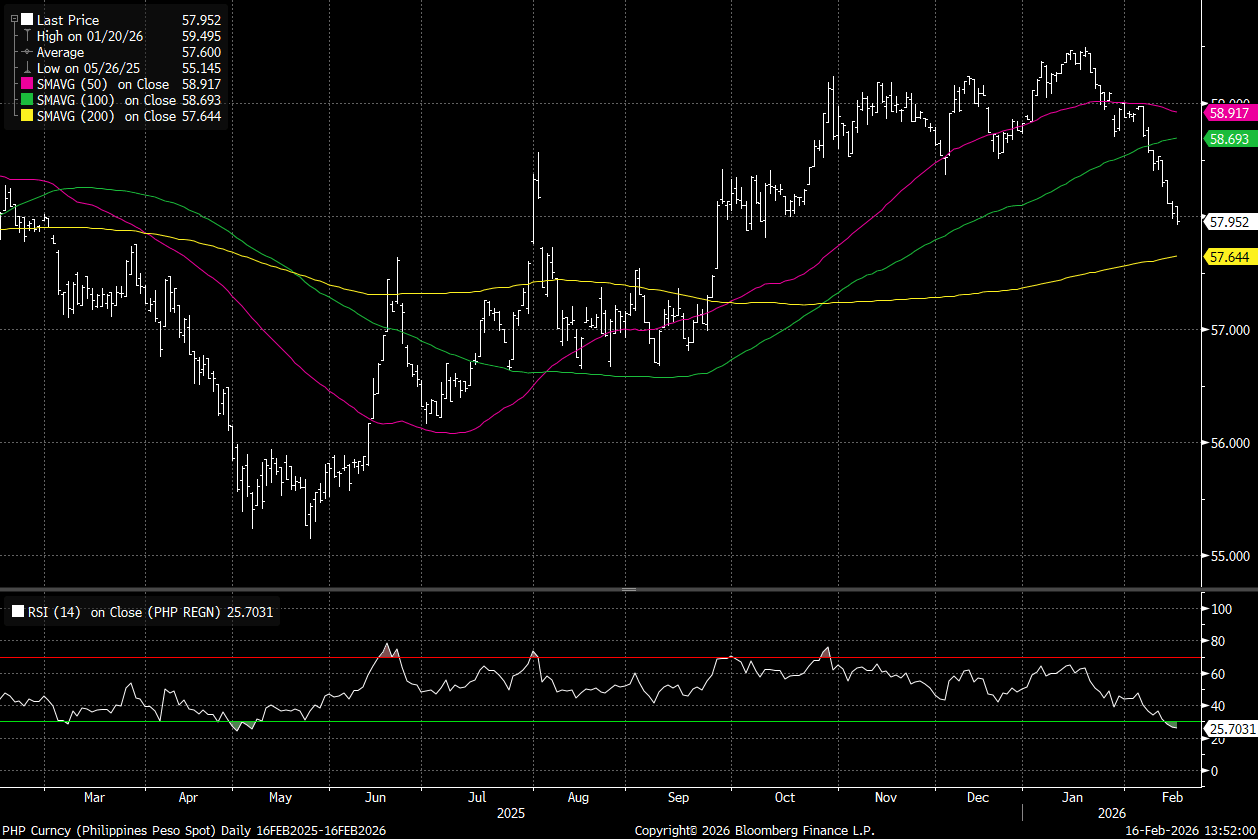

PHP: USD/PHP Testing Under 58.00, But Oversold On RSI & Some Sell-Side Caution

Spot USD/PHP is holding under 58.00, fresh lows back to the first half of Oct last year. The pair is comfortably under all key EMAs (58.15 is the 200-day point, which may now act as an upside resistance point). Interestingly though, we are now oversold per RSI (14), for the first time since early May last year, see the chart below. The simple 200-day MA is further south near 57.64.

- Broader USD softness is likely in play for PHP, as the US real 10yr yield sits under 1.80% now, fresh lows back to late Nov 2025. As we noted late last week, the directional correlation between this series and USD/PHP has been quite firm in recent weeks.

- While today USD/CNH is also tracking under 6.8900, fresh cycle lows back to 2023. Earlier on the local data front we had better than forecast overseas remittances as well, up 4.2% to $3522mn.

- Still the 1 month NDF is sitting around 58.00, slightly up from end Friday levels last week, so this doesn't suggest much shift in sentiment, so far today, with spot playing catch up to end moves from last week.

- Also via BBG: "The Philippine peso's current rally may prove short-lived as slowing economic growth and potential central bank interest-rate cuts erode recent gains, analysts say." (see this link for details). The central bank meeting outcome is due this Thursday, with the consensus expecting a 25bps cut.

Fig 1: USD/PHP Now Oversold Per RSI (14)

Source: Bloomberg Finance L.P./MNI

ASIA FX: USD/CNH Tests Under 6.8900, Fresh Lows Even With Onshore Out

It has been a relatively quiet start to the week with a number of countries in region closed for the lunar new year, including China, South Korea and Taiwan. Still, with Hong Kong and Singapore open today (they are shut tomorrow) we have seen some moves. Notably USD/CNH has tested under 6.8900, to fresh lows of 6.8868, before support emerged. We were last near 6.8890. Carry over positive momentum from last week for the yuan, including firm FX settlement data for Jan on Friday evening, has likely aided the move.

- There isn't much in the way of downside support points to not until we reach 6.8500 for USD/CNH. April 2023 lows were near 6.8300 in the pair. All key EMAs are trending lower with the 20-day around 6.9310. Via BBG, has also been seen as constructive for the yuan: “While exchange rate volatility remains possible, current trends indicate the yuan is increasingly viewed as a currency for trading, investment and financing, according to a report from Yuyuantantian, a social media account affiliated with state broadcaster China Central Television.”

- Elsewhere we had better than expected Thailand Q4 GDP, keeping the recent positive news flow around Thailand continuing. USD/THB has tested under 31.00, but couldn't get beyond 30.967 on the downside. We were last 31.025. The rise in local equities will likely aid further offshore inflow momentum, so we may see further tests sub the 31.00 level. The authorities want to see stronger growth though, the FinMin stating a 3% desire, but noting we may see around 2% growth this year.

- USD/PHP is under 58.00, but for the first time since May last year is oversold per RSI (14). The combination of a weaker USD, aided by lower US real yields, is driving PHP sentiment at the moment. We also better than expected remittances data for Dec today.

- USD/MYR has again tested under 3.9000, but there appears to be some support at this stage. From session lows of 3.8970, we were last around 3.9015. Broader macro trends and onshore macro support still appear supportive for MYR gains though.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 16/02/2026 | 0430/1330 | ** | Industrial Production | |

| 16/02/2026 | 0700/0800 | ** | Unemployment | |

| 16/02/2026 | 0800/0900 | * | CH Flash GDP | |

| 16/02/2026 | 1000/1100 | ** | EZ Industrial Production | |

| 16/02/2026 | - | ECB Lagarde and Cipollone at Eurogroup meeting | ||

| 16/02/2026 | 1315/0815 | ** | CMHC Housing Starts | |

| 16/02/2026 | 1325/0825 | Fed's Michelle Bowman | ||

| 16/02/2026 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0900/1000 | Foreign Trade | ||

| 17/02/2026 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI |