MNI EUROPEAN MARKETS ANALYSIS: USD Rallies Post BoJ & RBA Decisions

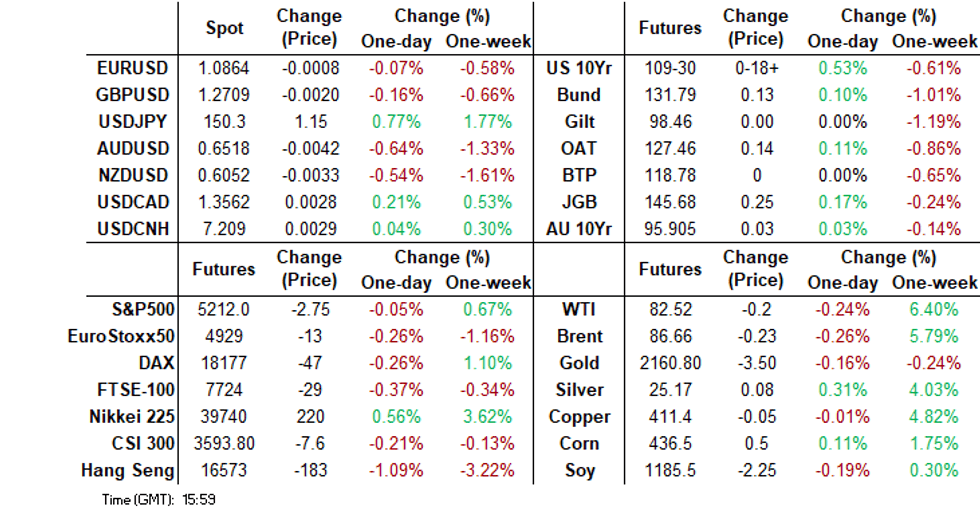

- USD/JPY has spiked higher post the BoJ decision to hike rates and end YCC. The decision to keep bond purchases largely unchanged and ready to act to curb sharp yield rises, has weighed on yen sentiment. In terms of JGBs, futures are higher, +13 compared to settlement levels. The BoJ also noted that financial conditions are likely to remain supportive. Coming up soon is Governor Ueda's press conference.

- The RBA’s March statement shifted to a neutral bias but following Governor Bullock’s press conference the change may be to give the Board more flexibility. Still, we saw the AUD down sharply and local bonds sharply richer post the decision.

- Broader USD sentiment has remained firm. The BBDXY pushing to multi-week highs. Weakness in terms of tech equities has also aided the USD at the margins, while oil holds close to recent highs.

- Looking ahead, there are US February housing and Canadian CPI data.

MARKETS

US TSYS: Treasury Futures edge Higher As BoJ Lifts Rates

- Jun'24 10Y futures pushed higher after the BoJ lifted rates, hitting a high of 110-01 we now trade just off those levels at 109-30+, up + 04+ since NY closed

- Looking at technical levels, initial support is 109-25+ (Feb 23 and the bear trigger), below here 109-14+ (Nov 28 low). While to the upside, initial resistance is 110-30+ (Mar 14 high) above here 111-03+( 50-day EMA).

- Treasury yields curves are slightly steeper today with the 2Y is -0.8bp to 4.723%, 10Y -0.6bp to 4.318%, while the 2y10y is +.253 to -40.727.

- Earlier, US lawmakers reached a funding deal to avert a shutdown through until Sept 30, with law makers now in a race to pass the bill before the midnight Friday deadline for a partial shutdown.

- Looking ahead the US calendar is empty today, with Building Permits & Housing starts on Tuesday focus this week will be on the FOMC on Thursday

JGBS: Futures Higher After BoJ Ends NIRP, Scraps YCC But Signals Further Bond Buying

JGB futures are higher, +13 compared to settlement levels, after initially gapping lower on news that the BoJ had ended its negative interest rate policy (NIRP) and scrapped Yield Curve Control (YCC).

- The BoJ hiked rates to 0.0% (lower bound) to 0.1% (upper bound) from negative territory. This is the first rise in interest rates since 2007.

- The short-term rate will now be the primary monetary policy tool. Still, the central bank expects financial conditions to remain accommodative.

- In terms of votes it was 7-2 to raise rates (to 0-0.1%), while JGB purchases will continue largely as before (in 8-1 vote). Currently the bank purchases around 6trln yen per month. It was a unanimous vote to end ETFs and J-REITS purchases. The bank will also gradually reduce the amount of CP and corporate bond purchases (looking to end such purchases in a year).

- On the economy, the virtuous cycle between wages and prices has become more solid, thereby signifying the price stability target would be achieved.

- The cash JGB curve has maintained its twist-flattening, pivoting at the 2s, with yields 1bp higher to 2bps lower. The benchmark 10-year yield is 2.4bps lower at 0.743% versus its YTD high of 0.801%.

- The swaps curve has twist-steepened, with rates 2bps lower to 2bps higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar is empty.

BOJ: Hikes Rates, But Maintain Bond Purchases & Financial Conditions Expected To Stay Supportive

The BoJ has hiked rates to 0.0% (lower bound) to 0.1% (upper bound) from negative territory. This is the first rise in interest rates since 2007.

- Critically, the central bank stated that the price stability target of 2% came in sight, while QQE and YCC and NIRP have fulfilled their respective roles. The short term rate will be the primary monetary policy tool. Still, the central bank expects financial conditions to remain accommodative.

- In terms of votes it was 7-2 to raise rates (to 0-0.1%), while JGB purchases will continue largely as before (in 8-1 vote). Currently the bank purchases around 6trln yen per month. It was unanimous vote to end ETFs and J-REITS purchases. The bank will also gradually reduce the amount of CP and corporate bond purchases (looking to end such purchases in a year).

- On the economy the central bank noted that the economic recovery continues gradually, but there are some pockets of weakness. It continues to expect steady wage rises this year, following a firm increase last year. The virtuous cycle between wages and prices has become more solid, thereby signifying the price stability target would be achieved.

- In terms of market reaction, USD/JPY got to highs of 149.92, but is now back under 149.70. There is an option expiry at 150.00 today, which may be influencing sentiment. The stance around accommodation financial conditions and keeping bond purchases largely unchanged is likely weighing on the yen.

- Much of what the BoJ stated today has generally been in the local media over recent weeks.

- In terms of JGBs, JBM4 currently sits in the middle of the post-BoJ Decision range at +11 compared to settlement levels.

AUSSIE BONDS: Sharply Richer After RBA’s Decision To Remove Its Tightening Bias

ACGBs (YM +8.0 & XM +3.5) sit richer after the RBA decides to remove its explicit tightening bias. The Board maintained the cash rate target at 4.35. Key points from the accompanying statement:

- Inflation is moderating but remains elevated, driven by goods inflation while services inflation gradually decreases.

- The data are consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs.

- Tight labour market conditions persist, though wages growth is expected to moderate.

- Economic uncertainties persist, with inflation projected to return to the 2-3% target range by 2025.

- The RBA prioritises returning inflation to target, considering evolving data and global economic conditions.

- Measures will be adjusted as needed to achieve this goal, with a focus on price stability and full employment.

- Cash ACGBs are 3-7bps richer on the day, with the 3/10 curve steeper and the AU-US 10-year yield differential 5bps lower at -23bps.

- Swap rates are 3-7bps lower on the day.

- The bills strip has bull-flattened, with pricing +2 to +10.

- RBA-dated OIS pricing has shunted 3-7bps softer for late-24 meetings. A cumulative 43bps of easing is priced by year-end versus 36bps before the RBA Decision.

- Tomorrow, the local calendar is empty apart from the sale of A$800 million of the 2.75% Jun-35 bond.

RBA: Keeping Options Open In Face Of Significant Uncertainties

The RBA’s March statement shifted to a neutral bias but following Governor Bullock’s press conference the change may be to give the Board more flexibility. The point that she really made was the high degree of uncertainty facing the economy and thus the Board. Risks to inflation remain “finely balanced” and outcomes could move in either direction and currently the RBA needs more data to be confident that inflation will return to target as projected.

- Governor Bullock strongly conveyed the message that rates could still move in either direction depending on inflation outcomes and currently there are risks in both directions. If inflation is set to remain above target for more than four years, then the bank will need to be concerned but it can consider easing if it returns to the band earlier than forecast.

- Journalists omitted to ask about the third option that rates stay where they are for a prolonged period, as the inflation path may be “bumpy”. Uncertainties may mean that it will be a long time before the Board is certain enough to change rates. Bullock reminded us that inflation isn’t projected to reach the band mid-point until mid-2026, which is a long way out and thus there is considerable uncertainty around the forecast.

- The tightening statement was removed in response to recent data, but Bullock didn’t state which release and so it may have been the aggregate outcome. But she said that as more data become available, it should become clearer if the Board is on the “right trajectory”. Currently, it is not confident enough to rule out another rate hike and so it is cautious and watching.

- The governor was opaque when asked whether a rate hike was discussed and responded by saying that the Board considers a range of possibilities to judge whether it is at the right spot. It considered what was “best for the circumstances”.

- The RBA is monitoring inflation expectations to ensure they don’t get stuck around 3.5%. It wants to see them fall to 2-3%.

- China is a concern that the RBA is watching very closely.

NZGBS: Late Bullish Flurry After A Subdued Session

NZGBs closed with a late bullish flurry after a subdued local session ahead of a busy week of central bank meetings, including the FOMC, BoJ, BoE and the RBA. With the local market closed at the time of the RBA & BoJ decision and statement, any reaction is likely to be reflected in early dealings tomorrow.

- (Bloomberg) -- A range of indicators released over the past fortnight “confirm New Zealand is in the midst of a severe economic slowdown,” the Treasury Dept. says in a Fortnightly Economic Update. Data “implies there was another quarter of roughly flat GDP in December and ongoing declines on a per capita basis”. (See link)

- Cash US tsys were little changed in today’s Asia-Pac session ahead of the BoJ’s Policy Decision.

- Swap rates closed flat to 3bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed for meetings out to August and 2bps softer beyond. A cumulative 58bps of easing is priced by year-end.

- Tomorrow, the local calendar will see Q1 Westpac Consumer Confidence and Q4 Current Account Balance data, ahead of Q4 GDP on Thursday.

FOREX: Dollar Boosted By Dovish BoJ & RBA Signals

The BBDXY sits up close to 0.15%, last near 1239.4. Gains of close to 0.50-0.60% have been recorded against both JPY and AUD.

- The main focus was on the BoJ outcome. In the event, the central bank removed NIRP and raised rates to 0.0-0.1%, while it also abandoned YCC, but kept bond purchases largely unchanged.

- Importantly, the BOJ stated it will make "nimble responses," increasing its purchases, should long-term interest rates rise." Also, given the current outlook for economic activity and prices, the BOJ anticipates that accommodative financial conditions will be maintained for the time being," the board said.

- The bond purchases point and still accommodative policy settings has weighed on the yen. From near 149.30 prior to the outcome, we have spiked close to 150.00, holding close to this level in recent dealings. Note BoJ Ueda's press conference is due later at 3:30pm Japan time.

- For the AUD, the RBA removed its language around further rate hikes can't be ruled out, instead replacing it with the board would not rule anything in or out. RBA Governor Bullock is currently holding her press conference, but largely reiterating what the earlier statement said.

- Governor Bullock played down any shift to neutral. Still, AUD/USD is close to session lows, last near 0.6530, off nearly 0.50%. Weaker equity tones in HK and China have has also likely weighed.

- NZD/USD has been dragged lower, last near 0.6060/65, off around 0.35%. The AUD/NZD cross has moved away from recent highs of 1.0795 to 1.0765/70.

- Looking ahead, there are US February housing and Canadian CPI data. ECB’s de Guindos speaks today too.

ASIA EQUITIES: HK & China Equities Heads Lower As Evergrande Troubles & Tech Turns

Hong Kong and China equities are lower today, with the tech and property sectors weighing on the market, tech names have been impacted after Nvidia sold off after unveiling its lasted AI processor at its GTC conference in San Jose earlier today, the EU is considering formal reviews of chips from China, while WuXi AppTech dropped 8.3% after giving weak 2024 guidance. Chinese regulators have stated the China Evergrande inflated revenue by more the $78b in the two years prior to defaulting.

- Hong Kong equities are lower today, the tech space is the the worst performing sectors as the HSTech Index trade down 1.83% while the Mainland Property Index is down about 1.72%, the wider HSI is down 1.20%. In China equiites are lower although out-performing Hong Kong equites, the CSI300 down 0.23%, while the CSI1000 is down 0.32% and the ChiNext is down 0.65%.

- China Northbound flows were 2.8 billion yuan on Monday, with the 5-day average at 2.07 billion, while the 20-day average sits at 3.65 billion yuan.

- In the property space, China Evergrande has been accused of falsely inflating revenue by more than $78b in the two years leading up to its failure according to the CSRC with much of the blame being put on the founder and chairman Hui Ka Yan. New home sales rose in Shanghai and Beijing and held steady in Guangzhou and Shenzhen, while Bloomberg reported Chinese new-home prices face steep declines in 2024 due to the combination of Vanke's debt crisis impacting buyer confidence, a surge in second-hand home inventory, and weakening pricing power for developers, particularly Country Garden, amidst a housing glut and liquidity constraints.

- The European Union is considering a formal review of the widespread use of mature or lower-end chips from China, echoing US concerns about national security risks and global supply chain vulnerabilities. This potential investigation may lead to joint measures with the US to address distortions in the global supply chain for these critical but not cutting-edge semiconductors.

- The Chinese government's initiative to encourage equipment renewal and consumer appliance trade-ins is expected to boost consumption and investment, potentially mobilizing up to 5 trillion yuan in investment and stimulating demand of over 1 trillion yuan annually, with an emphasis on voluntary decisions by consumers and corporations.

- Looking ahead, there is little on the calendar today, Wednesday loan prime rates are due out.

ASIA PAC EQUITIES: Asian Equities Reverse Earlier Losses After BoJ Lift Rates

Regional Asian equities are mostly higher today, focus was largely on the BoJ after they lifted rates for the first time in 17 years, the yen weakened and now trades above 150.17 a clear break of the 150 level while Japanese equities reversed their earlier losses to now trade higher. Elsewhere RBA kept rates on hold at 12-year highs, however haven't ruled are moves either way in interest rates looking ahead. Tech names are slightly lower after Nvidia held their AI conference earlier, while investors will be watching the China property space closely after the CSRC said China Evergrande had inflated revenue by $78b in the two-years prior to defaulting

- Japanese equities are lower today as the market awaits to hear from the BoJ later today. There has been little else in the way of market headlines today driving equities prices. Healthcare stocks are the worst performing, closely followed by tech, while Autos and energy are the top performers while the Nikkei 225 trades down 0.80%. The Topix is faring slightly better however still down 0.20% with Industrials, Consumer Discretionary & Financials the top performers.

- South Korean equities are lower today with the Kospi falling 1.30%, foreign investors are selling tech stocks with net foreign outflows of $213m so far this morning. While earlier WuXi AppTec revenue was in line with expectations however forward guidance weak for 2024 causing tech stocks to head lower.

- Taiwanese equities are lower as tech stocks weigh on the market. The Taiwanese officials have been growing increasingly concerned about market valuations and have been warning investors not to continue chasing stocks higher, the Taiex has opened twice above the 20,000 level recently but both times have been heavily sold in signs we may see more of a correction before being able to retest those levels, the Taiex is down 0.50%.

- Australian equities are unchanged today ahead of the RBA meeting at 2.30pm local, it's widely expected that rates will remain on hold at 12-year highs. Financials are weighing on the market offsetting gains in miners and real estate names.

- Elsewhere in SEA, New Zealand equities are slightly higher, while the NZ treasury warned of "severe slowdown", Singapore & Philippines equities are unchanged while Malaysian equities are down 0.45%,

ASIA EQUITY FLOWS: Equity Flows Light Ahead Of A Busy Central Bank Week

- China equities were higher again on Monday, economic and market headlines were light. Tech names were the top performers again, while the property sector was the worst performing China Evergrande has been accused of falsely inflating revenue by more than $78b in the two years prior to failing. Equity flow momentum continues to grow stronger, although Monday's flows were down on the prior day, with 2.82b. The 5-day average is now 5.07b, the 20-day average is 3.65b yuan.

- South Korean equities were higher non Monday, with $77m in net inflows after a recording their largest outflow for a year on Friday. Tech names were the top performing names with Samsung leading the way. 5-day average is still negative at -$110m, while the 20-day average is $61m

- Taiwan equities were higher on Monday with tech names the top performer. Equities flows marked their third day in a row of net selling the first time since January. Government officials have warned investors about inflated stock prices. While short term flow momentum is negative with the 5-day average now $135m, although the 20-day is still positive at $159m

- Indonesia, Philippines and Thailand equities saw very little in the way of equity flows on Monday as investors wait to hear from global central banks over the coming for days.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 2.8 | 25.4 | 73.4 |

| South Korea (USDmn) | 77 | -552 | 8113 |

| Taiwan (USDmn) | -306 | -679 | 7721 |

| India (USDmn)** | 93 | 2302 | 1843 |

| Indonesia (USDmn) | 6 | 561 | 1680 |

| Thailand (USDmn) | -8 | 57 | -892 |

| Malaysia (USDmn) *** | -33 | -88 | -29 |

| Philippines (USDmn) | 0 | -51.0 | 195 |

| Total (Ex China USDmn) | -171 | 1550 | 18632 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To March 15 |

OIL: Crude Holds Gains, FOMC & Demand Indicators In Focus

Oil prices have held onto most of Monday’s gains during APAC trading today. WTI is down 0.2% to hold just above $82/bbl where it has found support during the session. Brent is also 0.2% lower at $86.72, close to the intraday low. The focus of oil markets is Wednesday’s FOMC decision, with rates widely expected to be unchanged, and any further geopolitical developments. The USD index is slightly higher.

- With the IEA now forecasting a small deficit in oil markets this year due to stronger demand, supply developments will continue to be watched closely. Bloomberg estimates that China refined a record amount of crude at the start of 2024. US crude stocks fell sharply the week before last as refining rates increased in the face of strong gasoline demand. US API data for last week is released today with the official EIA information due on Wednesday.

- Last week the Ukraine struck a major Russian refining facility and over the weekend drones targeted refineries in a number of Russia’s regions with some being hit. Bloomberg is reporting that JP Morgan estimated that Russia’s refining capacity has been impacted by 900kbd. Further Ukrainian attacks are likely to add to the current crude risk premium.

- OPEC+ supply cuts have been extended to the end of June but not all members are complying with their quotas. Iraq announced that it will reduce its exports to make up for overproducing.

- Later there are US February housing and Canadian CPI data. ECB’s de Guindos speaks today too.

GOLD: Slightly Higher Ahead Of A Busy Week OF Central Bank Meetings

Gold is little changed in the Asia-Pac session, after closing 0.2% higher at $2160.36 on Monday.

- It was a relatively subdued start to a busy week of central bank meetings, including the FOMC, BoJ, BoE and the RBA.

- Nevertheless, bullion is holding near record highs after rising sharply since mid-February, a rally that was partially driven by expectations the Federal Reserve was moving closer to easing policy. FOMC dated OIS is currently indicating a 52% chance of a Fed cut in June.

- According to MNI’s technicals team, the recent break above $2135.4, the Dec 4 high, reinforced bullish conditions and signaled scope for $2206.6 next, a Fibonacci projection. Short-term conditions are overbought and a deeper retracement would allow this set-up to unwind. Firm support is at $2112.9, the 20-day EMA.

INDONESIA: MNI Bank Indonesia Preview – March 2024: IDR Needs Fed To Ease First

- Bank Indonesia (BI) is unanimously expected to leave rates at 6.0% at its March 20 meeting given the persistence of a high level of “global uncertainty” and little new domestic information since the last decision. FX stability remains its focus and as USDIDR remains elevated, a pivot to a dovish tone is highly unlikely this month. BI will not want to risk further rupiah softening by cutting rates ahead of the Fed.

- BI has said that it sees H2 2024 as the window to begin easing to support growth but if the first Fed move is delayed, then it may not be able to cut until closer to the end of the year rather than the middle.

- Indonesian CPI inflation is well within the target band and growth is robust, although exports are looking soft but BI expects them to improve. It is likely to continue to support the economy with accommodative macroprudential measures for now.

- See full preview here.

ASIA FX: USD/Asia Pairs Higher, Spillover From Yen Weakness Evident

USD/Asia pairs are mostly higher, albeit to varying degrees. This is in line with firmer USD gains against the majors, particularly post the BoJ's dovish hike. Higher USD/JPY levels has certainly aided the USD/Asia move higher in parts of the region. CNH is weaker, but only modestly. Regional equities have been mixed, but softer HK and China trends have weighed on FX markets. KRW and PHP are the weakest performers in spot terms. Tomorrow, we have the China LPR outcomes, but no change is expected. The BI decision is also due, but again a steady hand is forecast.

- USD/CNH is pushing up towards 7.2100 amid weaker yen levels and a negative lead from onshore stocks. Familiar headwinds in terms of the property sector, along with earnings concerns in the tech sector, have been the main drags. For USD/CNH we are still sub earlier March at 7.2176. Tomorrow, the LPRs are expected to remain on hold, which would be in line with the recent unchanged MLF rate.

- 1 month USD/KRW has been dragged higher, last near 1337.5, close to session highs and around 0.20% weaker in won terms versus end NY levels from Monday. Onshore equities are weaker, amid broad tech equity losses. Spill over from weaker yen levels is also a likely headwind. Focus will be on whether we can breach the 1340 level and if the authorities step up their response in terms of FX rhetoric.

- USD/IDR pushed above 15730 in early dealing, but sits back close to 15720 in recent dealings (dips back to 15700 have been supported). Most of the earlier spot weakness reflected catch up to the sharp rally in the 1 month USD/IDR NDF through Monday US trade. We got to highs of 15757 earlier, but now sit back at 15734. Tomorrow's BI decision is seen on hold. Tomorrow we also get the General Election Commission declaring the winner of the earlier Presidential elections, although there is a risk that a legal challenge is filed over the result and concerns this is followed by protests.

- USD/THB is attempting to hold a break of 36.00, the pair last near 36.06, around 0.20% weaker, so in line with broader moves in the region. Earlier Feb highs in the pair were close to 36.20. Thailand PM Srettha noted that the committee in charge of the country's digital wallet scheme will meet in two weeks.

- USD/PHP spot has rallied strongly, up nearly 0.50% to 55.82. A fundamental catalyst hasn't been evident for the move. It is unwinding some of the recent outperformance from PHP though.

INDONESIA: Indonesian Sovereign Debt Steady, BI Rate Decision Wednesday

Indonesian USD sovereign debt curve is largely unchanged over the past day, there has been slightly better selling in the front end, with yields 1-2bps higher. The Indonesian President is expected to be announced on Wednesday, although it is also expected to be met with protests and a legal challenge. The Bank Indonesia will holds their rate decision meeting also on Wednesday where rates are expected to be left at 6.00%

- Curves are mostly unchanged over the past day, the front end saw some selling, although it should be noted that Friday saw the INDON front-end trading 8-10bps tighter vs the US Treasuries, the 2Y yield is 1bp higher at 4.98%, 5Y yield is unchanged at 4.995%, the 10Y yield is unchanged at 5.09%, while the 5-year CDS is down 1bp to 68bps.

- The INDON to UST spread difference continues to move tighter, the front end did push slightly wider over the past day up 1bp, while the longer end tightened, 2yr is 26bps (+1bp), 5yr is 66.5bps (-1.5bps), while the 10yr is 77.5bps (-0.5bps).

- In cross-asset moves, the USD/IDR is 0.12% higher, the JCI is 0.56% higher, Palm Oil is down 0.47%, while US Tsys yields are 1-3bps lower.

- Foreign Investors continue to sell Indonesian debt with Friday marking the 7th consecutive day of selling. The 5-day average is now -$131m, the 20-day average has turned negative at -$64m while the longer term 200-day average now also sits negative at -$0.71m

- The General Election Commission is set to declare the official result of Indonesia’s presidential election by Wednesday, with Defense Minister Prabowo Subianto expected to be declared President after already claiming victory, however Presidential candidates Anies Baswedan and Ganjar Pranowo are expected to file a legal challenge citing fraud.

- Looking ahead: Wednesday BI Rate decision, expected to hold steady at 6.00%

PHILIPPINES: Philippines Sovereign Debt Curves Flatter, BoP Data Due Out Shortly

The Philippines USD sovereign debt curves are slightly flatter on Tuesday with yields 1-3bps higher. It's a light week for economic data for Philippines with just Balance of Payments due later today, elsewhere the EU and Philippines have resumed their free trade negotiations after seven years, while the US, Japan & Philippines will hold their first trilateral meet leaders meeting on April 11.

- Curves are slightly slight flatter with yields 1-3bps higher. The 2Y yield is 1bp higher at 4.86%, 5Y yield is 1.0bp higher at 5.02% the 10Y yield is unchanged at 5.10%, while 5yr CDS is unchanged to 60bps.

- The PHILIP to UST spread difference has significantly tightened over the past week, although did move 1-2bps wider over the past day with the 2y is 14bps (+2bps), the 5yr is 69bps (+1bp), while the 10yr is 79.5bps (-0.5bp)

- Cross-asset moves: the USD/PHP is 0.41% higher, PSEi Index is up 0.60%, Corporate Credit curve is 4-9bps higher over the past week with better selling i3-4yr part of the curve, while US Tsys yields are 1.3bps lower.

- The EU and the Philippines have resumed their free trade negotiations after a seven-year halt, aiming for an ambitious and comprehensive trade deal that will ensure mutual market access, diversify supply chains, and provide opportunities for professionals and service providers, according to statements from both sides.

- US President Joe Biden will convene the first trilateral US-Japan-Philippines leaders' summit on April 11 at the White House, where discussions will focus on promoting inclusive economic growth, advancing clean energy supply chains and climate cooperation, and enhancing peace and security in the Indo-Pacific and globally.

- Looking Ahead: Philippines To Sell PHP30B 20Y bonds, while Balance of Payment data due on Tuesday

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/03/2024 | 0830/0930 |  | EU | ECB's De Guindos at IV Observatorio de las Finanzas event | |

| 19/03/2024 | 1000/1100 | *** |  | DE | ZEW Current Conditions Index |

| 19/03/2024 | 1000/1100 | *** |  | DE | ZEW Current Expectations Index |

| 19/03/2024 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 19/03/2024 | 1230/0830 | *** |  | CA | CPI |

| 19/03/2024 | 1230/0830 | *** |  | US | Housing Starts |

| 19/03/2024 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 19/03/2024 | 1530/1130 | * |  | US | US Treasury Auction Result for Cash Management Bill |

| 19/03/2024 | 1530/1130 | ** |  | US | US Treasury Auction Result for 52 Week Bill |

| 19/03/2024 | 1700/1300 | ** |  | US | US Treasury Auction Result for 20 Year Bond |

| 19/03/2024 | 2000/1600 | ** |  | US | TICS |