EM ASIA CREDIT: MNI EM Credit Market Update - Asia

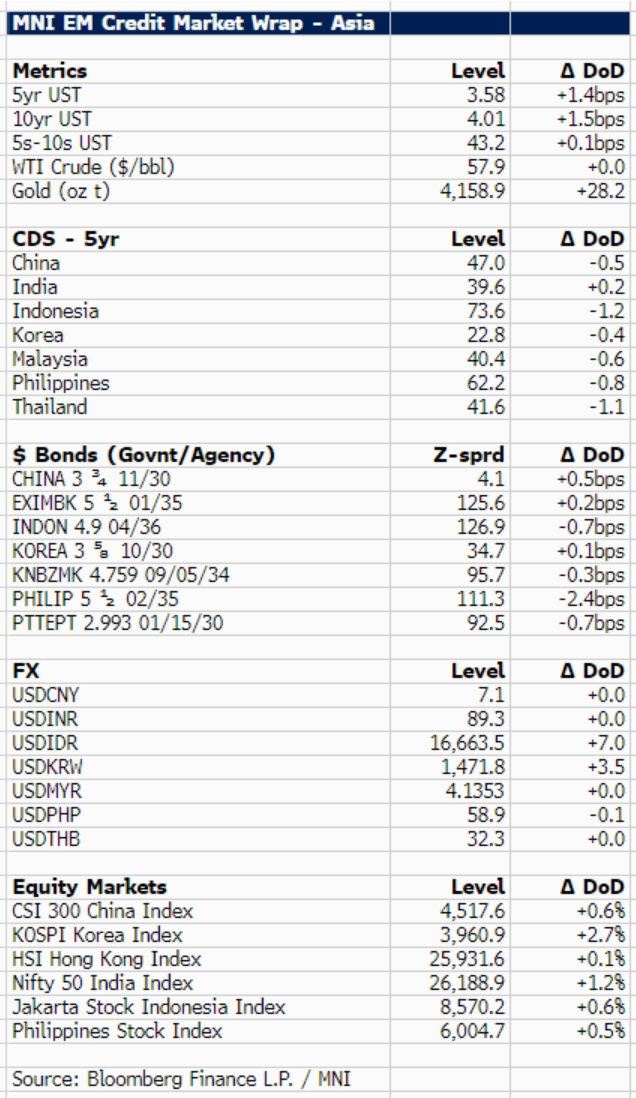

US 10Y Treasury yields are 1.5bp higher at 4.01% with no particular driver ahead of Thanksgiving. We follows LATAM, secondary market benchmark USD bond spreads tightened a couple of basis points in higher rated names while several high yield names such as Brazil corporate CSN and the Argentina sovereign widened about 20bp.

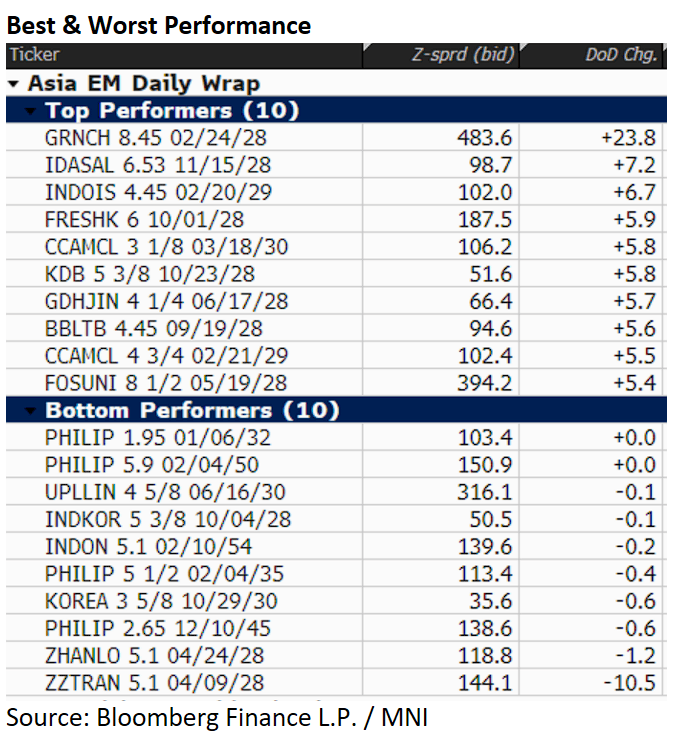

In Asia, emerging markets USD sovereign and agency spreads are more or less unchanged. Regional equities were positive, led by a 2.7% gain in the Korean KOSPI. In primary markets, two new deals are out today, a USD PerpNC3 bond from China Huaneng Group and a USD 3Y bond from China Orient Asset Management. Overnight, West China Cement and BDO Unibank priced USD deals.

Outside of primary issuance, China Vanke bonds continue to decline, with USD bonds down around 3 points as trading in some yuan bonds was temporarily suspended. This follows a 10-point drop yesterday amid mounting investor concerns over liquidity risks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Bullish Theme

- RES 4: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 3: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 2: 0.6574 50.0% retracement of the Sep 17 - Oct 14 bear leg

- RES 1: 0.6548 Intraday high

- PRICE: 0.6537 @ 08:11 GMT Oct 27

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

AUDUSD continues to trade above its recent lows. Attention remains on the Oct 14 reversal pattern - a hammer candle. It signals the end of the bear cycle that started Sep 17. Note that the initial firm resistance at 0.6541, the 50-day EMA, has been pierced. A clear break of this hurdle would strengthen a bullish theme. For bears, a breach of 0.6440, the Oct 14 low, would instead cancel the reversal pattern and reinstate a bear threat.

FOREX: AUD Gains on Positive Trade Deal Language, USD Flat Headed into Fed

- Hopes for a trade deal between China and the US (triggered by positive language from Trump this weekend) has tipped the AUD to be the best early performer in G10 , up 0.5% against the USD through the European open. As such, AUDUSD has reached the best level in 11 sessions and the next resistance is now seen towards 0.6573.

- More broadly in G10, the USD is mixed, keeping the USD Index close to flat as markets prepare for the FOMC meeting on Wednesday, at which markets are fully priced for a further 25bps rate cut (and another in December).

- Today sees, German IFO and ECB inflation expectations while the US durable goods orders print will not be released due to the Government shutdown.

EGBS: Core Bonds Pressured on Trade Deal Hopes; Belgian, US Supply Due This Week

- Bund futures gapped lower at the resumption of trade late Sunday as the growing hope of a trade deal between the US and China helped support equities and pressure core global bonds. President Trump said that nothing was agreed yet but felt "good" on the prospect of a deal.

- The opening gap in Bunds sits at 129.49, while the initial support remains at 129.13. European CPIs will be the main data release this Week, but focus will be on the Fed meeting on Wednesday outside of Europe.

- Investors will also be watching a busy week of earnings on Wednesday & Thursday. Microsoft, Alphabet, Meta, Amazon and Apple are all due to report.

- Month End extensions will likely be small for Europe, average for the US and large for the UK into Friday.

- SUPPLY: Belgium 5s, 7s, 10s, US Sells $69bn of 2yr Notes and $70bn of 5yr Notes.

- The Fed and ECB are inside their pre-meeting media blackout periods, keeping the speaker schedule muted.