MNI ECB Review: You Could Argue That We Are On Hold

Jul-24 17:26By: Chris Harrison and 1 more...

European Central Bank+ 4

Download Full Report Here

Executive Summary

- The ECB left its three key rates unchanged, including the deposit rate at 2.00%, as fully expected.

- The decision statement continued to push data-dependence and a meeting-by-meeting approach.

- The press conference was met with a more hawkish reaction, driven by remarks such as “you could argue that we are on hold”, “the sooner this trade uncertainty is resolved the less uncertainty we will have to deal with” and a more constructive view on Eurozone growth.

- It was seen in light of the previous day’s media reports of nearing a US-EU deal with a 15% tariff, and also followed this morning’s better than expected July flash PMIs.

- Bloomberg and Reuters sources pieces have since added to the notion of a high bar to a cut in September.

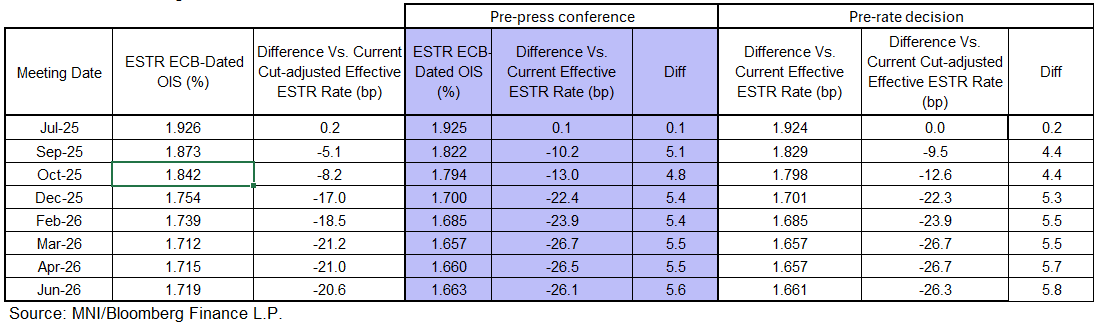

- Evolution of September cut odds: 50% before US-EU trade deal reports yesterday, 40% prior to the ECB decision, 28% at the end of the press conference and ~20% after sources pieces.

- A mild easing bias remains but it has been trimmed to a 17bp of cumulative cuts priced to year-end vs 22.5bp pre-decision. Cut expectations are capped at 21bp for March.

- In initial analyst takes, Commerzbank no longer expect a final cut in September and instead see rates on hold at 2% through end-2026. RBC also no longer see a September cut and see risks of a debate about rates hikes developing. We’ll follow with a full summary of analyst views tomorrow.