MNI ECB Review: Lagarde Sees The End Of The Easing Cycle

Jun-05 17:12By: Chris Harrison and 1 more...

European Central Bank+ 4

Download Full Report Here

- The ECB cut its three key rates by 25bps, including the deposit rate to 2.00% as fully expected.

- The decision statement was unsurprisingly non-committal.

- New forecasts showed a sharper than expected drop in HICP inflation for 2026, but it was mostly on energy whilst core inflation and GDP growth for 2026 was marked down a tenth for exactly in line with the median analyst reviewed by MNI.

- President Lagarde gave a clearly more hawkish/congratulatory tone in the press conference however, noting policy is well positioned and that “we are getting to the end of a monetary policy cycle that was responding to compounded shocks.”

- Released after the press release, a new approach at providing scenario analysis didn’t move markets.

- A Bloomberg sources piece that officials envisaged a pause in July echoed market pricing.

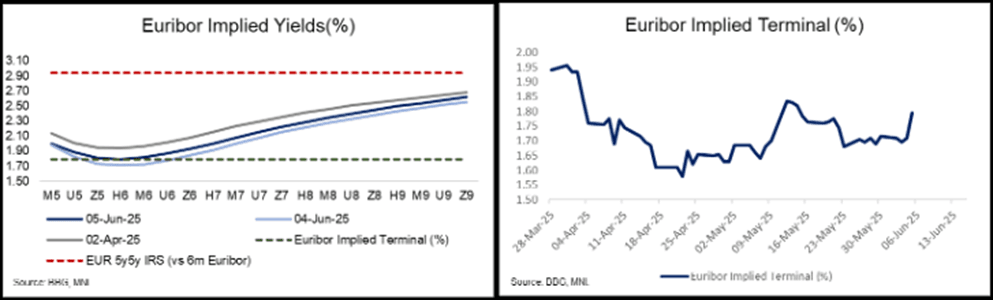

- The main change today has been a notable hawkish shift in ECB pricing, unwinding some recent dovish moves on data, with September pricing drifting to 14-15bp vs an equivalent 20bp yesterday.

- There is only just about one cut priced for the rest of this year, in December.