MNI ECB Review: Bar To Cuts Pushed A Little Higher Again

Sep-11 2025 17:53By: Chris Harrison and 1 more...

European Central BankSchatzGermanyBobl+ 3

Hidden PDF

Executive Summary

- The ECB left its three key rates unchanged, including the deposit rate at 2.00%, as fully expected.

- The decision statement continued to push data-dependence and a meeting-by-meeting approach.

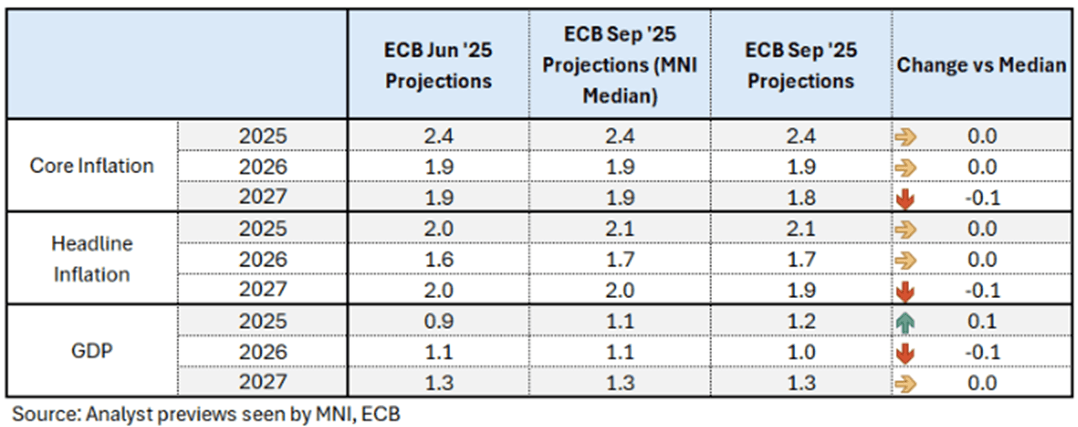

- Headline and core inflation was revised down 0.1pp in 2027 to 1.9% and 1.8% respectively. That sparked a modest dovish reaction, but the decision statement warned the inflation outlook was broadly unchanged.

- The press conference then sparked a hawkish reaction with growth risks deemed more balanced and the disinflationary process over.

- Policy is still deemed to be in a good place and the ECB won’t react to small deviations from inflation target projections.

- The bar to rate cuts appears to have been lifted a little higher. Nevertheless, with inflation projections technically undershooting, we still see near-term risk poised to further cuts rather than an early start to a hiking cycle.

- ECB sources from Bloomberg suggested further shocks are needed to see rate cuts whilst Reuters sources said the debate on a rate cut was not over just yet with October too soon but December eyed.

- ECB-dated OIS points to just 12bp of cumulative cuts out to July 2026.

Related stories

Related by topic

European Central Bank

Schatz

Germany

Bobl

Bunds

Inflation

GDP