MNI ASIA OPEN: Surprisingly Subdued Tariff Impact On US CPI

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- MNI US Inflation Insight: Core Goods Spike Fails To Emerge

- Trump’s BLS Pick Suggested Suspending Monthly Jobs Report (BBG)

- MNI BRIEF: Fed Policy Well-Positioned For Uncertainty - Barkin

- MNI: Fed Easing Would Raise Risk of Price Increases - Schmid

- US: Trump Says Considering Allowing a "Major Lawsuit" Against Powell to Proceed

MNI US Inflation Insight: Core Goods Spike Fails To Emerge

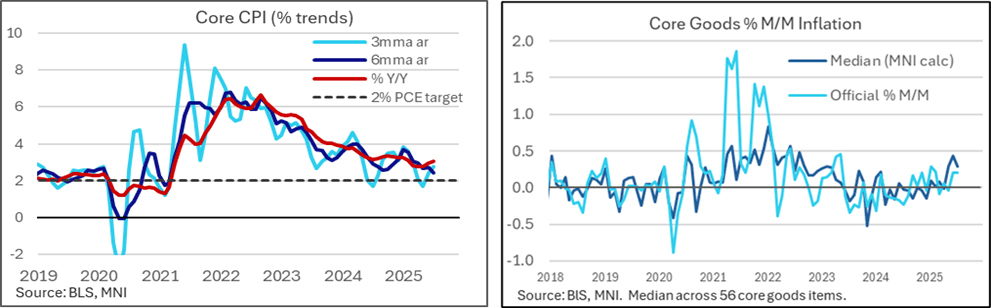

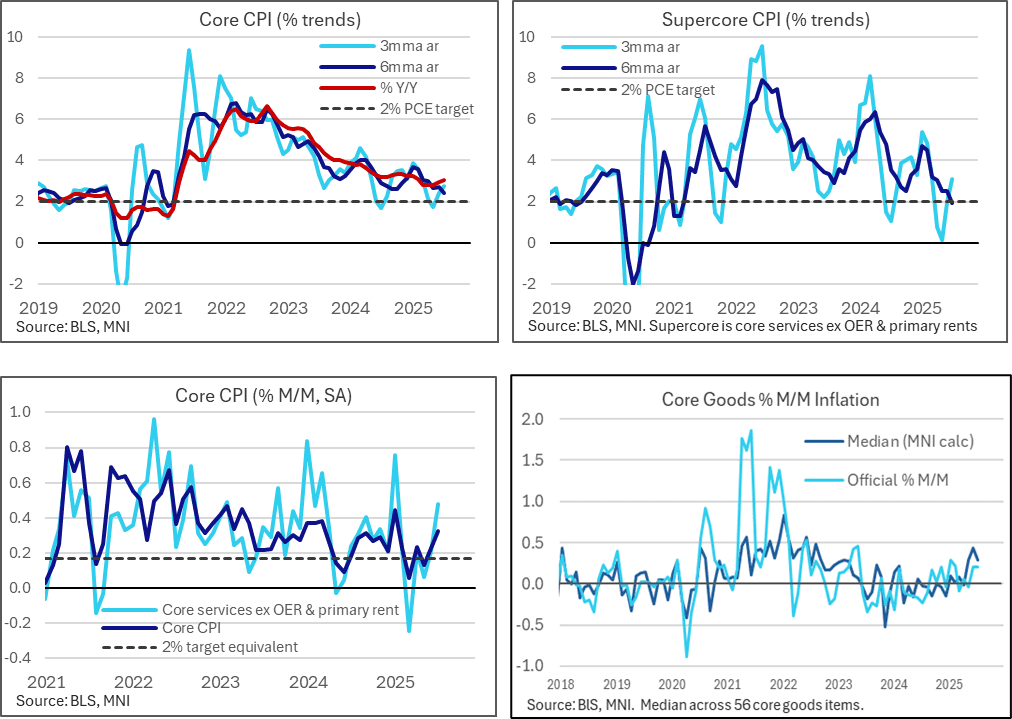

The July CPI report saw further acceleration in monthly core inflation but it was driven by the volatile supercore category. Instead, core goods inflation, an area of focus for tariff passthrough clues, was surprisingly soft. This category only maintained the still-solid monthly clip seen in June, whilst median core goods inflation moderated after a strong increase in June. Core CPI inflation was exactly in line with the median unrounded analyst estimate we had seen for July at 0.32% M/M, accelerating from 0.23% in June and 0.13% in May for its strongest month since January.

MNI BRIEF: Fed Policy Well-Positioned For Uncertainty - Barkin

The Federal Reserve is well-placed to either weaker growth or higher inflation emanating from tariffs and other factors, though a softer economic backdrop appears to have become a predominant concern as tariff inflation fails to materialize, Richmond Fed President Thomas Barkin said Tuesday. "We may well see pressure on inflation, and we may also see pressure on unemployment, but the balance between the two is still unclear. As the visibility continues to improve, we are well positioned to adjust our policy stance as needed," Barkin said in prepared remarks.

MNI: Fed Easing Would Raise Risk of Price Increases - Schmid

Kansas City Fed President Jeff Schmid said Tuesday a modestly restrictive monetary policy stance remains appropriate for the time being and interest rate cuts could be counterproductive, with an economy still showing momentum, growing business optimism, and inflation stuck above target. "My support for a patient approach to changing the policy rate is based on two connected arguments. First, while monetary policy might currently be restrictive, it is not very restrictive," he said in prepared remarks. "And second, given recent price pressures, a modestly restrictive stance is exactly where we want to be."

US: Trump Says Considering Allowing a "Major Lawsuit" Against Powell to Proceed (MNI)

Trump on Truth Social: "Jerome “Too Late” Powell must NOW lower the rate. Steve “Manouychin” really gave me a “beauty”when he pushed this loser. The damage he has done by always being Too Late is incalculable. Fortunately, the economy is sooo good that we’ve blown through Powell and the complacent Board. I am, though, considering allowing a major lawsuit against Powell to proceed because of the horrible, and grossly incompetent, job he has done in managing the construction of the Fed Buildings. Three Billion Dollars for a job that should have been a $50 Million Dollar fix up. Not good!"

MNI NORGES WATCH: Aug Hold Foreseen, Door Open To More H2 Cuts

Norges Bank is expected to leave its key policy rate on hold at 4.25% in August, following up its June cut by sitting tight this month, with market expectations for a couple more cuts later in the year. The Norwegian central bank’s June rate path was compatible with "one or two" further cuts in the second half, and market pricing and analysts have converged on September and December as the most likely months for the next steps downward.

Trump’s BLS Pick Suggested Suspending Monthly Jobs Report (BBG)

EJ Antoni, President Donald Trump’s pick to lead the Bureau of Labor Statistics, has suggested suspending the agency’s monthly jobs reports and publishing only quarterly numbers until issues with data collection are corrected. In an interview with Fox Business before Trump nominated him on Monday, Antoni said businesses can’t plan and the Federal Reserve can’t conduct monetary policy when the monthly report is unreliable and frequently overstated and thus misleading.

MNI BRIEF: White House 'Hopes' Jobs Report Released Monthly

The White House on Tuesday said it expects the Bureau of Labor Statistics to continue to produce monthly jobs reports and going forward it will assess new means and methods for gathering key data that Wall Street so carefully analyzes. "That is the plan and that's the hope," White House press secretary Karoline Leavitt said, when asked if the administration expects the BLS to continue to release monthly jobs reports. "There has certainly been a decline in the quality and the reliability of data coming from the Bureau of Labor Statistics," she told reporters.

US TSYS: Lack Of Core Goods CPI Acceleration Triggers Twist Steepening

The Treasury curve twist steepened Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025 (up from 57bp Monday).

- This wasn't greatly dampened by Fed hawks Barkin and Schmid who expressed no urgency to cut rates in the near future.

- The long end, conversely, sold off after an initial rally. German Bunds appeared to lead the retracement, amid heavy volumes there albeit with little obvious catalyst. However some of the sell-off came after President Trump said on social media that he was considering a "major lawsuit" against Fed Chair Powell over Federal Reserve building renovation cost overruns.

- Latest cash levels: the 2-Yr yield is down 3.8bps at 3.7308%, 5-Yr is down 1.6bps at 3.8207%, 10-Yr is up 0.2bps at 4.2868%, and 30-Yr is up 2.1bps at 4.8736%. Sep 10-Yr futures (TY) down 2/32 at 111-26.5 (L: 111-19.5 / H: 112-06)

- Wednesday's data calendar is lighter (ahead of PPI and retail sales later in the week), with weekly MBA mortgage data in the morning, though we hear from a few FOMC participants including Barkin, Goolsbee, and Bostic.

OVERNIGHT DATA

US DATA: US CPI Wrap: No Sign Of Faster Tariff Passthrough In July CPI Report

The July CPI report saw further acceleration in monthly core CPI inflation but it was driven by the volatile supercore category. Instead, core goods inflation, an area of focus for tariff passthrough clues, was surprisingly soft as it only maintained the monthly clip seen in June whilst median core goods inflation moderated after a strong increase in June.

- Core CPI inflation was exactly in line with the median unrounded analyst estimate we had seen for July at 0.32% M/M, accelerating from 0.23% in June and 0.13% in May for its strongest month since January.

- The breakdown relative to expectation was dovish however, as core goods underwhelmed (0.21% M/M vs average expectations closer to 0.4%) in a month that was expected to show increasing signs of tariff passthrough ahead of perhaps the largest monthly increases in the fall months. It follows a very similar 0.20% M/M in Jun after a weak -0.04% M/M in May.

- Notably, this came despite used cars prices exceeding expectations (0.48% M/M vs estimates closer to 0.3) although that’s still a modest increase after four consecutive monthly declines averaging -0.6% M/M.

- Indeed, MNI calculations of median core goods inflation across 56 items softened to 0.28% M/M after a particularly strong 0.44% in June and 0.29% in May. This is still a robust pace - it averaged 0.0% M/M in 2024 and 0.06% M/M in Q1 - but clearly doesn't show any further acceleration in what would have been a sign of accelerated tariff passthrough.

- The offsetting factor to softer than expected core goods inflation was core services (0.36% M/M vs average expectations around 0.30%), driven by the volatile “supercore” category at 0.48% M/M whilst rental inflation was exactly as expected.

- Airfares played a large role here (4.0% vs 1.5% expected) and as always won’t feed into PCE. Some notable PCE inputs meanwhile saw partly offsetting large moves from booming dental services (2.6% M/M, 4.3% of supercore CPI) and further declines in lodging (-1.0% M/M, 6.4% of supercore).

- Taking a step back, core CPI inflation firmed to 3.06% Y/Y (cons 3.0) after 2.93% Y/Y for its strongest since Feb 2025. Both three- and six-month run rates are tracking softer than this, at 2.8% and 2.4% annualized respectively.

- Adding to the net dovish take from core CPI details, headline CPI undershot with 0.20% M/M in July (MNI median 0.24) owing to downside surprises in both food (0.05% M/M vs expectations 0.25%, including food at home at -0.12% M/M for only the second decline in the past fifteen months) and energy (-1.1% vs 0.6%, despite gasoline being as expected).

- It saw headline CPI inflation little changed at 2.70% Y/Y after 2.67% in June, holding the prior acceleration from the April low of 2.31% Y/Y.

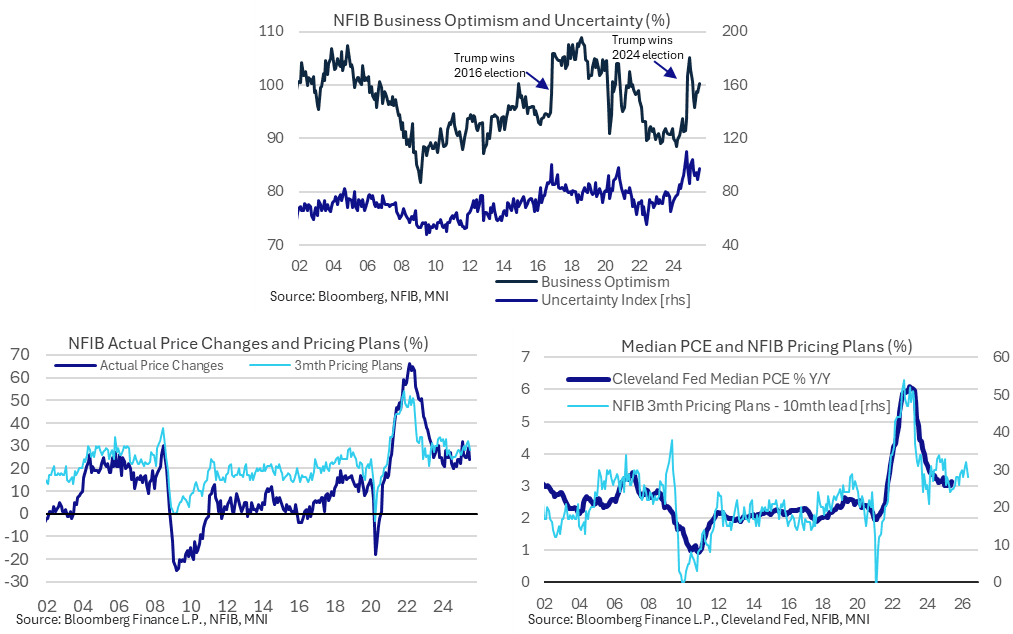

US DATA: NFIB Small Business Price Plans Cool

The NFIB small business index was stronger than expected in July despite weakness in the already published jobs details. Notably despite this slightly firmer backdrop, price plans cooled rather than accelerating further.

- The NFIB small business index was higher than expected in July as it increased to 100.3 (cons 98.9) after 98.6 in June for a five-month high.

- The 100.3 compares with the April low of 95.8 on the announcement of reciprocal tariffs, a high of 105.1 in December fully reflecting US election results and an average of 93 in 2024. The series has a very long-term 52-year average of 98.

- Impressively, seeing as the already published jobs report had shown multiple points of weakness in July, six of the ten components for this broader index improved.

- A net 36% of owners expect better business conditions, +14pps from a month earlier and the most this year. A net 16% said now is a good time to expand their business, the largest share since January.

- Ahead of today’s US CPI report for July, price plans remain relatively elevated but contained, and with some moderation compared to May and June levels.

- Specifically, a net 24% increased prices over the past three months vs 29% in June and a recent high of 32% back in February. This is in line with the 23% average seen in 2024 but remains above pre-pandemic averages of ~12%.

- A net 28% expects to increase prices over the next three months vs a recent high of 32% in June. It’s in line with the 28% averaged in 2024 but remains above the 22% averaged pre-pandemic.

- As such, it’s still pointing to some stabilization in inflation at above-target rates but the pace hasn’t accelerated further as might have been seen if small firms were planning to increasingly pass on tariff cost increases.

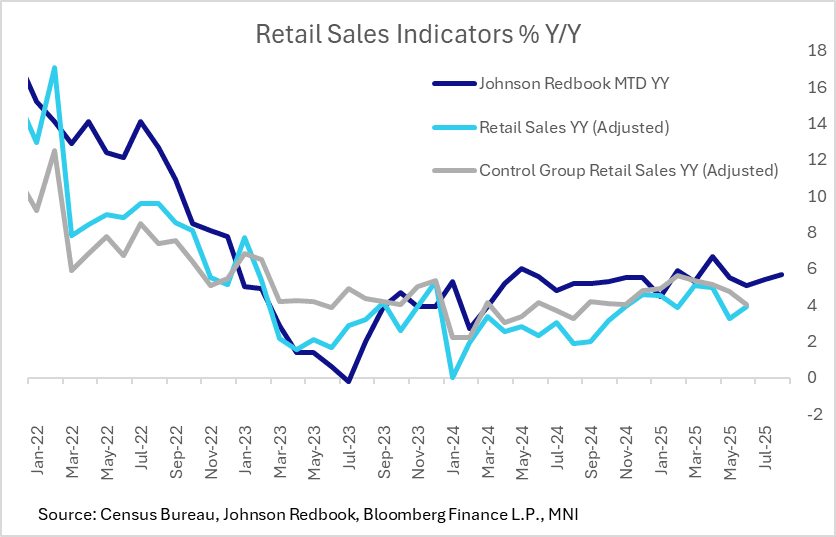

US DATA: Redbook Retail Sales Remain Solid, Sellers Eye Tariff Price Increases

Retail sales have maintained their solid growth pace through the summer, with the Johnson Redbook Retail Sales Index rising 5.7% Y/Y for the week ending Aug 9 (the first retail week of August). That's light vs a targeted 6.2% gain but still robust overall.

- The report notes in the anecdotal section that retailers are planning price increases due to tariffs: "August, much like July, is a transitional month marked by final summer clearance sales and a shift in inventories toward back-to-school merchandise and fall apparel. Sales have benefited from back-to-school sales tax holidays in several states, including Arkansas, Florida, Maryland, Massachusetts, Ohio, Oklahoma, South Carolina, Texas, Virginia, and West Virginia. As retailers begin to report their second-quarter earnings in the coming weeks, they are approaching the second half of the year with caution. They anticipate higher costs due to tariffs and are planning price increases to offset these adjustments. Currently, back-to-school sales have not yet made a significant impact, but this is expected to change as the month progresses."

- If sustained, a reading of 5.7% Y/Y would mean the fastest growth since April. While the Redbook index's growth has typically been higher than the "official" Census Bureau series, current levels would be consistent with Y/Y growth in the latter above 3.5%. We get the July report on Friday, with consensus for overall retail sales at 0.3% M/M (roughly 3.3-3.5% Y/Y).

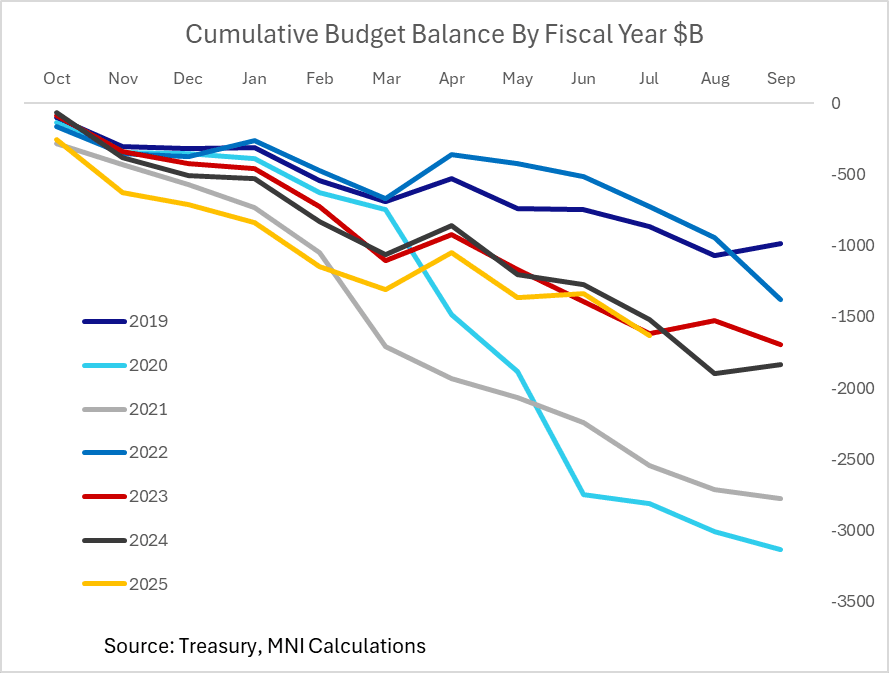

US FISCAL: Federal Deficit Up 7% Y/Y With 2 Months To Go In Fiscal Year

Treasury reported a $291.1B federal budget deficit in July, larger than the $239B shortfall expected by Bloomberg consensus but almost exactly in line with the Congressional Budget Office's previously published $289B estimate.

- As MNI noted previously, while the year-to-date deficit is up 7% Y/Y to $1.629T with two months remaining in the 2025 fiscal year (which runs Oct-Sep), compared with $1.517T in the same period of FY2024, the difference is smaller when adjusting for timing changes.

- CBO estimated a $37B wider deficit when accounting for these changes, vs $109B "actual". The implied adjusted rise in the deficit is around 2% Y/Y, tracking lower than nominal GDP growth over that period.

- YTD revenue is up 6.4% Y/Y ($4.346T), with expenditure up 6.7% ($5.975T).

- At the start of 2025, CBO estimated a $1.9T deficit this fiscal year which remains plausible with August typically seeing a large deficit ahead of a better outturn in September in part on tax receipts, though looks on the high side at this point.

- That implies the FY2025 deficit looks closer to coming in below the 6.4% of GDP posted in FY2024, though is widely expected to re-expand in FY2026 largely on "One Big Beautiful Bill" effects.

- CBO will publish the Monthly Budget Review with its final projection next month.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

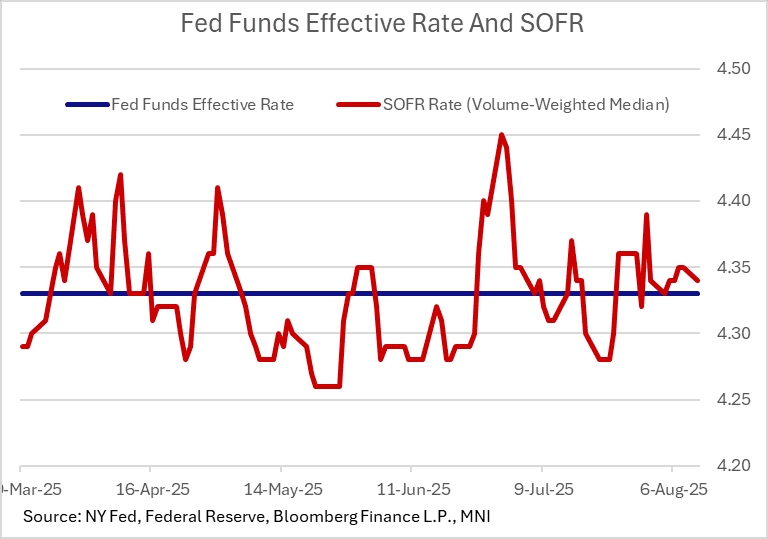

US TSYS/OVERNIGHT REPO: SOFR Softens Slightly, Potential Pickup Ahead

Secured rates were a little softer Monday as was broadly expected, with SOFR edging 1bp lower to 4.34%. Other major secured rates and effective Fed funds were unchanged.

- As we noted yesterday, pressure could pick up later in the week on Treasury auction settlements. These include $55B in net cash raised by bills today, and a further $42B on Thursday, followed by $35B in coupon settlements Friday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.34%, -0.01%, $2796B

* Broad General Collateral Rate (BGCR): 4.33%, no change, $1173B

* Tri-Party General Collateral Rate (TGCR): 4.33%, no change, $1137B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $115B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $263B

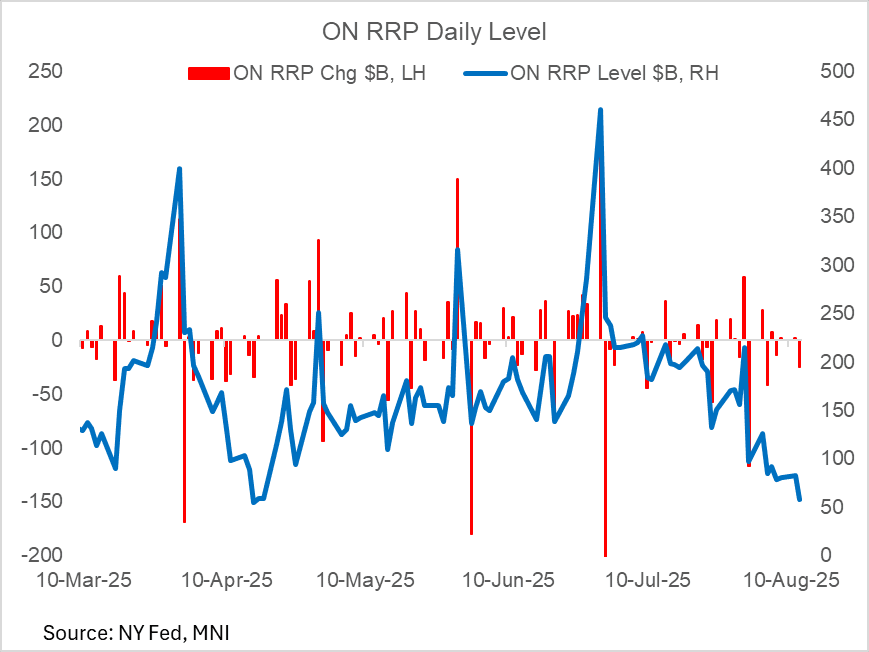

US TSYS/OVERNIGHT REPO: ON RRP Takeup At 4-Month Low

Takeup of the Fed's overnight reverse repo facility Tuesday fell to its lowest since April 16th (which was depressed by a major tax payment deadline).

- At $57.5B, down $24.7B from Monday, this is the 7th session in the last 8 that it's been below $100B. It hasn't so consistently been below that level since February.

- It comes amid continued buildup of the Treasury General Account amid bill sales, which appear to be diverting funds away from RRP.

- At least one analyst (Citi) sees ON RRP takeup dropping to near-zero by month-end.

EGBs-GILTS CASH CLOSE: Bear Steepening, With Gilts Underperforming

European curves bear steepened Tuesday.

- US CPI data in early afternoon was the session's global focus, and initially brought a positive reaction in core FI as it appeared to allay fears of upside pressure on goods prices from inflation.

- However the move swiftly reversed, with Bunds leading a global selloff. There was no identifiable trigger for the long-end German sell-off, which saw 30Y yields hit the highest since 2011 amid heavy volumes in futures. 10Y German yields stopped just shy of the July high of 2.769% (hitting 2.758%).

- There was some extension of the selloff in sympathy with long-end Treasuries as President Trump said on social media that he was considering allowing a "major lawsuit" against Fed Chair Powell to proceed.

- That said, Gilts underperformed Bunds on the day. The August UK labour market release was on balance stronger-than-expected, bringing a mildly hawkish market reaction, though private sector regular pay data remains consistent with slowing wage growth. Our review of the data is here.

- Both the German and UK curves bear steepened, with periphery/semi-core EGB spreads closing mixed.

- Wednesday's calendar is lighter, with final Spanish and German CPI readings on offer.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 1.967%, 5-Yr is up 2.9bps at 2.318%, 10-Yr is up 4.8bps at 2.744%, and 30-Yr is up 7.3bps at 3.299%.

- UK: The 2-Yr yield is up 2.2bps at 3.885%, 5-Yr is up 3.9bps at 4.04%, 10-Yr is up 6.1bps at 4.626%, and 30-Yr is up 7.5bps at 5.467%.

- Italian BTP spread down 0.1bps at 78.8bps / French OAT up 0.5bps at 66.8bps

FOREX: USD Slides as CPI Clears Way for Sept Fed Cut

- The USD slid against all others Tuesday as the July CPI print cleared the path for the Fed to resume rate cuts from the September meeting. Core goods inflation undershot expectations for a further acceleration in M/M terms, and while still a solid monthly clip compared to 2024 levels, there few sufficient signs of tariff-led inflation that could derail easing both in September, as well as further rate cuts before year-end.

- The resultant USD Index weakness pushed the price back below the 50-dma, testing last week's lows in the process. Medium-term, this clears markets for a test of the late July pullback lows of 97.109 - a level that should see firm support.

- EUR was the primary beneficiary of the USD pullback, and EUR/JPY extended gains above 172.50 for the first time since July - keeping momentum pointed higher and tilting focus toward the YTD highs of 173.97. In addition, GBP/USD saw support, with the CPI reaction prompting a new weekly high and a test at the 50-dma of 1.3502. Clearance above this level would further reverse the downleg off the late July high and put markets near 3% off the early August low.

- Despite the post-RBA weakness, AUDUSD is yet to challenge any meaningful support. The pair rallied well off the week's lowest levels last week on broad USD weakness - erasing any signs of a bearish breakout on the show through the 20- and 50-day EMAs. While support at 0.6455 the Jul 17 low, has been cleared, the recovery in prices keeps key resistance in focus at 0.6625 the Jul 24 high.

- Focus Wednesday shifts to Japanese PPI data, German final CPI and appearances from Fed's Barkin and Schmid.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/08/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 13/08/2025 | 0700/0900 | *** | HICP (f) | |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 13/08/2025 | - | *** | Money Supply | |

| 13/08/2025 | - | *** | New Loans | |

| 13/08/2025 | - | *** | Social Financing | |

| 13/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 13/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 13/08/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 13/08/2025 | 1730/1330 | Atlanta Fed's Raphael Bostic | ||

| 14/08/2025 | - | NorgesBank Meeting | ||

| 14/08/2025 | 0130/1130 | *** | Labor Force Survey |