MNI ASIA OPEN: Soft Inflation Expectation, Steady FOMC Ahead

- MNI Fed Preview - Sep 2023: The Last Mile

- MNI INTERVIEW: Fed Will Hike Again If Inflation Lingers-Kamin

- MNI FED WATCH: On Hold, But Open To One More

- MNI Surprisingly Low U.Mich Inflation Expectations

US

FED: The FOMC will hold rates at its September meeting, while maintaining its tightening bias.

- Despite recent progress on inflation, which will see core PCE forecasts revised down for the first time since 2020, we expect most of the FOMC’s median expectations to be largely unchanged in the latest set of quarterly projections.

- That includes the median rate “dots” indicating one further hike by end-2023, as most participants will remain cautious of signalling that the hiking cycle is over, and 100bp of cuts in 2024.

- Both of these are a very close call though, with risks that the 2023-24 dots shift a notch lower.

FED: Federal Reserve officials could “turn on a dime” and raise interest rates further if future inflation reports, like the latest August CPI, point to a plateauing of price pressures, former Fed board economist Steven Kamin told MNI.

- While policymakers have been hoping for a possible end to rate increases following a six-month period of steady disinflation, the stronger-than-expected CPI was a bump on the road to lower inflation that, if repeated, would prompt the FOMC to hike rates at least once more and perhaps even further, Kamin said.

- “The interest by the FOMC in pausing, maybe stopping the rate hikes, and seeing how inflation plays out is based on the felicitous inflation developments of the last half year, with inflation falling a lot,” he told MNI’s FedSpeak Podcast. “That will turn on a dime if the Fed officials become convinced that inflation is becoming more intransigent than they thought.” For more see MNI Policy main wire at 1036ET.

FED: The Federal Reserve is set to hold benchmark interest rates steady at a 5.25%-5.5% range next week as it takes some more time to decide whether a final quarter-point increase will be needed.

- Most officials projected in June that two more rate hikes were necessary, and the FOMC delivered one of those in July. Since then, growth has surprised to the upside with the Atlanta Fed GDP nowcast showing 4.9% for the third quarter, well above the FOMC's projection of a 1% annual rate for the fourth quarter. Meanwhile, inflation has eased and is on track to better the FOMC's June estimates slightly by year-end, while the labor market has stayed strong and the jobless rate lower than projected.

- An updated set of projections will likely continue to show a split over whether the Fed should hike again in November or December and a range of opinions over how quickly to trim rates next year as inflation falls. "Now is the time when differences in inflation forecasts and economy are going to widen and the resulting uncertainty over the path of policy will also likely grow," former Dallas Fed principal policy adviser Joe Tracy said in an interview. For more see MNI Policy main wire at 0954ET.

US TSYS Yields Higher Ahead Expected Steady FOMC W/ Tightening Bias Next Wk

- US FI markets look to finish weaker across the board Friday, inside a generally narrow session range after scaling back support overnight.

- Weakness came after a hawkish ECB sources story in the FT overnight sapped risk appetites ahead the weekend. Markets had traded positively after Thursday's ECB rate hike messaging was deemed less hawkish at the time. Focus is on next Wednesday's FOMC announcement where the Fed is expected to hold rates steady while maintaining a tightening bias.

- Modest data driven volatility in the first half: Treasury futures extended lows, TYZ3 marks 109-12.5 (-11.5) before drawing some buy interest after NY Fed data show persistent inflation pressures. Import Price Index MoM (0.5% vs. 0.3% est, prior down-revised to 0.1%), Export Price Index MoM (1.3% vs. 0.4% est, prior down-revised to 0.5%) while Empire Manufacturing climbs to 1.9 vs. -10.0 est.

- Treasury futures bounced off session lows after UofM data shows softer inflation expectations: 1 Yr Inflation 3.1% vs. 3.5% est, 5-10 Yr Inflation 2.7% vs 3.0% est. Futures saw sporadic sell interest as TYZ3 climbed to 109-28.5 (+4.5). Curves holding steeper profiles after the bell: 3m10Y +3.338 at -115.408, 2Y10Y +1.304 at -71.637.

- Quiet start to next week with NY Fed Services, NAHB Housing Market Index and TIC Flows.

OVERNIGHT DATA

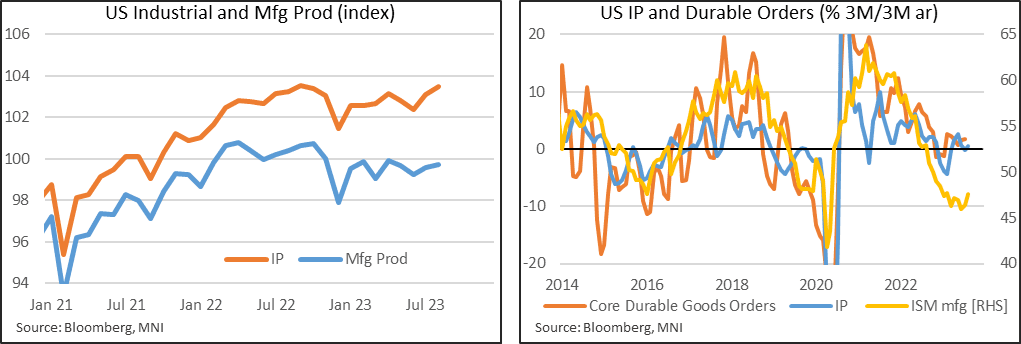

- US AUG INDUSTRIAL PROD +0.4%; CAP UTIL 79.7%

- US JUL IP REV TO +0.7%; CAP UTIL REV 79.5%

- US AUG MFG OUTPUT +0.1%

- Industrial production was stronger than expected in August at 0.4% M/M (cons 0.1).

- The surprise was dented by a downward revised July (0.7 from an initial 1.0) but there were also some upward revisions to prior months including -0.4 from an initial -0.8% for June, which don’t show on the main Bloomberg calendar limited to just the prior month.

- However, these moves weren’t driven by manufacturing production, which was more closely in line with expectations with a tepid 0.1% M/M (cons 0.1) after a downward revised 0.5% (initial 0.4) in Jul and upward revised -0.4% (initial -0.5%) in June.

- It leaves sluggish trend growth of 0.5% for IP and essentially 0% for manufacturing on a 3M/3M basis, although they continue to hold up well relative to the ISM manufacturing index firmly in contraction territory at 47.6 as of August.

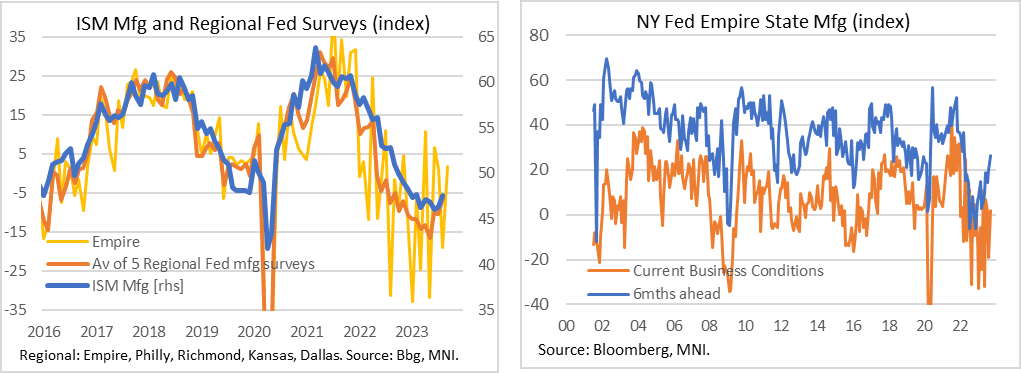

- US NY FED EMPIRE STATE MFG INDEX 1.9 SEP

- US NY FED EMPIRE MFG NEW ORDERS 5.1 SEP

- US NY FED EMPIRE MFG EMPLOYMENT INDEX -2.7 SEP

- US NY FED EMPIRE MFG PRICES PAID INDEX 25.8 SEP

- The Empire Fed manufacturing index increased by more than expected to +1.9 (cons -10) in September from -19 in August, back close to the +1.1 seen in July for the ever-volatile series (monthly move std dev of 23pts since 2021).

- Whilst we put little weight on the current period headline measure, it’s worth noting that the six-month ahead index increased 6.4pts to 26.3 for its highest since Mar’22.

- It has shown much less volatility than the current period headline index, although still can noisy with a std dev of 8.5pts over the same period.

- Behind this trend improvement: “New orders and shipments are expected to increase significantly in the months ahead, and employment is expected to grow. The capital spending index edged down to 10.3, suggesting that capital spending plans remained somewhat weak.”

- US AUG IMPORT PRICES +0.5%

- US AUG EXPORT PRICES +1.3%; NON-AG +1.7%; AGRICULTURE -2.2%

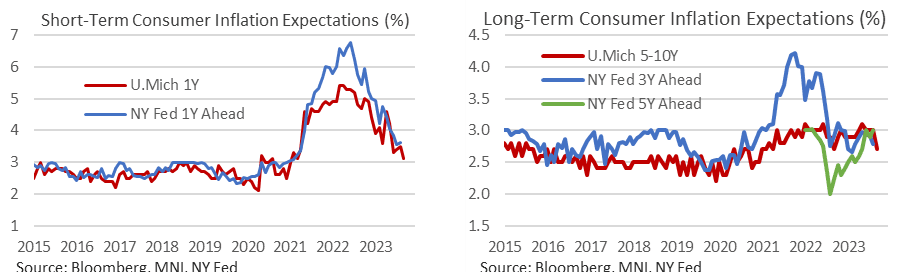

- UNIV OF MICHIGAN SEP. PRELIM 1Y INFL EXPECTATIONS 3.1% (3.5% EXP; 3.5% AUG)

- UNIV OF MICHIGAN SEP. PRELIM 5-10Y INFL EXPECTATIONS 2.7% (3.0% EXP, 3.0% AUG)

- UNIV OF MICHIGAN CONSUMER SENTIMENT PRELIMINARY SEP INDEX 67.7

- UMICH CURRENT ECONOMIC CONDITIONS PRELIMINARY SEP INDEX 69.8

- UMICH CONSUMER EXPECTATIONS PRELIMINARY SEP INDEX 66.3

US DATA: U.Mich inflation expectations come in markedly lower than expected in the preliminary September data.1Y inflation expectations: 3.1% (cons 3.5) after 3.5%

- 5-1Y inflation expectations: 2.7% (cons 3.0) after 3.0%. It’s a joint low since Sep’22, the only month it was outside of the narrow 2.9-3.1% range since Aug’21, and it was last at 2.7% in Apr’21.

- Softer inflation expectations came alongside weaker consumer sentiment, at 67.7 (cons 69.0) after 69.5, although that was dragged down by current conditions (from 75.7 to 67.7) whereas expectations firmed (from 65.5 to 66.3).

- “Consumers have taken note of the stalling slowdown in inflation, but they do expect the slowdown to resume.”

- CANADIAN JUL MANUFACTURING SALES +1.6% MOM

- CANADA JUL FACTORY INVENTORIES -0.7%; INVENTORY-SALES RATIO 1.7

- FOREIGN HOLDINGS OF CANADA SECURITIES +11.6B CAD IN JUL

- CANADIAN HOLDINGS OF FOREIGN SECURITIES +2.6B CAD IN JUL

MARKETS SNAPSHOT

Key late session market levels:- DJIA down 255.03 points (-0.73%) at 34648.98

- S&P E-Mini Future down 53 points (-1.16%) at 4501.25

- Nasdaq down 223.1 points (-1.6%) at 13700.37

- US 10-Yr yield is up 3.6 bps at 4.3224%

- US Dec 10-Yr futures are down 7/32 at 109-17

- EURUSD up 0.0019 (0.18%) at 1.0661

- USDJPY up 0.37 (0.25%) at 147.84

- WTI Crude Oil (front-month) up $0.86 (0.95%) at $91.02

- Gold is up $13.43 (0.7%) at $1924.23

- EuroStoxx 50 up 15.3 points (0.36%) at 4295.05

- FTSE 100 up 38.3 points (0.5%) at 7711.38

- German DAX up 88.24 points (0.56%) at 15893.53

- French CAC 40 up 70.15 points (0.96%) at 7378.82

US TREASURY FUTURES CLOSE

- 3M10Y +3.338, -115.408 (L: -122.552 / H: -113.426)

- 2Y10Y +1.504, -71.437 (L: -73.75 / H: -70.255)

- 2Y30Y +0.914, -62.544 (L: -64.364 / H: -61.021)

- 5Y30Y -0.352, -4.308 (L: -5.963 / H: -2.89)

- Current futures levels:

- Dec 2-Yr futures down 1.75/32 at 101-15.875 (L: 101-14.625 / H: 101-18.375)

- Dec 5-Yr futures down 5/32 at 105-30.75 (L: 105-28.25 / H: 106-06.5)

- Dec 10-Yr futures down 7.5/32 at 109-16.5 (L: 109-12.5 / H: 109-28.5)

- Dec 30-Yr futures down 15/32 at 118-19 (L: 118-11 / H: 119-09)

- Dec Ultra futures down 19/32 at 124-31 (L: 124-25 / H: 125-27)

US 10Y FUTURE TECHS: (Z3) Key Support Remains Intact - For Now

- RES 4: 112-24+ High Jul 27

- RES 3: 112-14 High Aug 10

- RES 2: 112-00 Round number resistance

- RES 1: 110-07+ /111-12+ 20-day EMA / High Sep 1 key resistance

- PRICE: 109-14 @ 1400 ET Sep 15

- SUP 1: 109-03 Low Sep 13 and the bear trigger

- SUP 2: 109-00 Round number support

- SUP 3: 108-20 1.000 proj of the Jul 18 - Aug 4 - Aug 10 price swing

- SUP 4: 107.23 1.236 proj of the Jul 18 - Aug 4 - Aug 10 price swing

The trend direction in Treasuries remains down and Wednesday’s low print of 109-03 reinforces the bearish theme and. However, the recovery from Wednesday’s low was a bullish development and a hammer candle formation - a reversal signal - was confirmed at the close. The pattern suggests scope for a correction near-term. First resistance to watch is 110-07+, the 20-day EMA. On the downside, a break of 109-03 would resume the downtrend.

SOFR FUTURES CLOSE

- Sep 23 +0.008 at 94.608

- Dec 23 steady at 94.550

- Mar 24 -0.030 at 94.645

- Jun 24 -0.040 at 94.870

- Red Pack (Sep 24-Jun 25) -0.045 to -0.04

- Green Pack (Sep 25-Jun 26) -0.04 to -0.035

- Blue Pack (Sep 26-Jun 27) -0.04 to -0.035

- Gold Pack (Sep 27-Jun 28) -0.035 to -0.03

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00349 to 5.32708 (-0.00238/wk)

- 3M -0.00841 to 5.40168 (-0.00879/wk)

- 6M -0.01183 to 5.46584 (-0.00613/wk)

- 12M -0.01521 to 5.42144 (-0.00248/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $92B

- Daily Overnight Bank Funding Rate: 5.31% volume: $252B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.436T

- Broad General Collateral Rate (BGCR): 5.30%, $575B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $563B

- (rate, volume levels reflect prior session)

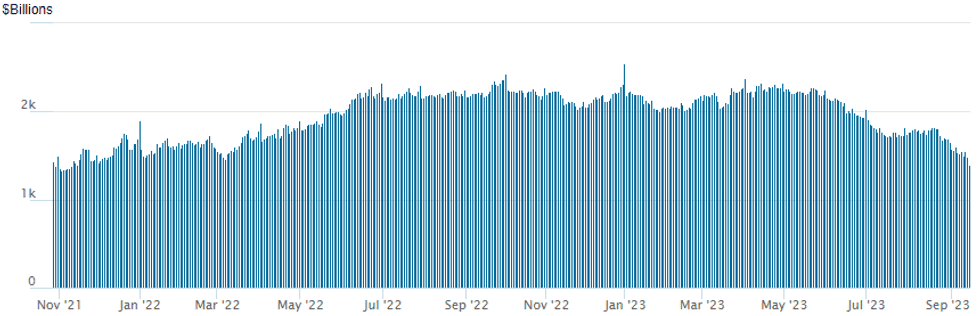

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

Repo operation falls back lowest level since November 15, 2021: 1,401.403B w/96 counterparties, compared to $1,492.427B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE US$ Corporate/Supra-Sovereign Debt Near $50B Issued on Week

- Date $MM Issuer (Priced *, Launch #)

- 09/15 $1B #Energy Development Oman 10Y Sukuk +165

- 09/15 $Benchmark African Development Bank (AfDB) investor calls

- $4.25B Priced Thursday, $47.15B running total for the week

- 09/14 $1.5B *Citigroup PerpNC5 7.625%

- 09/14 $1.25B *Bangkok Bank $500M 5Y +125a, $750M 10Y +150a

- 09/14 $500M *Corebridge 5Y +150

EGBs-GILTS CASH CLOSE: Weaker On Hawkish ECB Messaging

An early sell-off saw UK and German yields completely reverse their drop after Thursday's ECB decision, with bear steepening in both curves as 30Y segments underperformed.

- Several ECB speakers commented in the wake of Thursday's decision, but it was the hawks that spurred weakness on the open and set a negative tone for rates on the day.

- Hawkish ECB sources in an FT piece overnight looked to keep open the option of a rate hike in late '23. Other commentary was mixed: Muller, usually a hawk, played down the need for further hikes; Vasle said he was open to further hikes if needed; Simkus pointed to hope that Thursday's hike would be the last; de Guindos and Lagarde stuck to yesterday's script.

- Gilt yields rose for the 1st session in 4, alongside EGBs, with attention turning to the BoE decision next week.

- Multiple ratings decisions after market close Friday include Moody's on Greece, and S&P on Spain. GGBs have underperformed vs periphery peers despite hopes of a constructive assessment.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 5bps at 3.216%, 5-Yr is up 7.2bps at 2.692%, 10-Yr is up 8.3bps at 2.676%, and 30-Yr is up 9.1bps at 2.818%.

- UK: The 2-Yr yield is up 7.2bps at 5.022%, 5-Yr is up 5.3bps at 4.534%, 10-Yr is up 7.8bps at 4.359%, and 30-Yr is up 9.3bps at 4.701%.

- Italian BTP spread up 3.8bps at 178.5bps / Greek up 4bps at 142.2bps

FOREX USDJPY Bridges Gap, USD Index Extends Weekly Winning Streak

- Currency Markets traded in subdued fashion despite the weakness across major equity benchmarks. Despite the USD index dropping 0.15% on the session and having a shaky start to the week, the DXY looks set to extend its impressive streak of consecutive weekly advances to nine. Slightly higher US inflation data and firmer-than-expected activity figures have underpinned the greenback strength.

- The session highlight was the rally for USDJPY in early European trade, on the back of reports that there may have been some confusion by markets in their interpretation of the weekend comments by Bank of Japan Governor. According to people familiar with the matter, most of what Ueda said in the Yomiuri newspaper interview published Saturday was consistent with his routine remarks of late, indicating very little change in how the BOJ board will need to assess both upside and downside risks before adjusting the bank’s policy.

- USDJPY moved steadily higher throughout the European session, bridging the gap to last week’s close, however, unable to breach the 148 handle. Above here, and in focus next week, will be 148.40 next, the Nov 4 2022 high and 148.85, the Oct 31 2022 high. This would all the while narrow the gap with 150.00, a level touted by some sell-side analysts as a potential tipping point for the MOF to intervene.

- Amid the weakness in stocks, AUD, NZD and GBP have edged a touch lower to finish the week, with a more noticeable 0.4% uptick for EURGBP. Note that the 100-day MA at 0.8612, has been pierced which represents an important resistance.

- The docket is packed next week with central bank meetings, highlighted by the Fed and the BOE. Elsewhere, rate decisions in Norway, Sweden and Switzerland are scheduled as well as a host of emerging market central banks.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/09/2023 | 0900/1100 |  | EU | ECB's de Guindos Speaks at Event | |

| 18/09/2023 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 18/09/2023 | 1230/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 18/09/2023 | 1400/1000 | ** |  | US | NAHB Home Builder Index |

| 18/09/2023 | 1530/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 18/09/2023 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 18/09/2023 | 2000/1600 | ** |  | US | TICS |