MNI ASIA OPEN: Pres Trump Tariff Threat Back in Spotlight

EXECUTIVE SUMMARY

- MNI FED: Chicago's Goolsbee: EU Tariff Threat Scary, Still See Lower Rates End-2026

- MNI TARIFFS: US' Bessent-Hope 50% Tariff Rate 'Lights Fire Under EU' To Reach Deal

- MNI TARIFFS: 50% EU Tariffs Would Have Big PCE, GDP Hit: Yale Budget Lab's Tedeschi

- MNI US DATA: KC Fed Services Sees Surprising Strength In May

- MNI US DATA: New Home Sales Surprisingly Step Above Recent Ranges

US

MNI FED: Hawks Musalem And Schmid Emphasize Signal From Hard Over Soft Data

St Louis Fed President Musalem (2025 FOMC voter, hawk) spoke alongside fellow 2025 FOMC voter, Kansas City Fed President Schmidt (hawk), at a panel event Friday. While there was almost nothing directly mentioning current monetary policy, it was notable that both appeared to assess "hard" data much more seriously than "soft" survey data. One possible takeaway from this is that the emphasis on incoming hard data means they are likely to want to wait for longer before making any decision to adjust rates.

MNI FED: Chicago's Goolsbee: EU Tariff Threat Scary, Still See Lower Rates End-2026

Chicago Fed President Goolsbee (2025 FOMC voter, dove) tells CNBC that the latest tariff threat of 50% rates on the EU is "really scary" for US supply chains, and he reiterates previous language in saying that the bar for adjusting rates remains high so long as uncertainty persists. Asked about his current rate cut view, Goolsbee says: "as we went into April 2nd...I thought over the next 12-18 months rates could come down a fair amount toward where the Dot Plot said they would settle". Goolsbee now says that timeline is "10-16 months" - implying that his view that rates would drop to near neutral by late 2026 hasn't really changed.

NEWS

MNI TARIFFS: Bessent-'Several Large Trade Deals In Coming Weeks'

Speaking on BBG TV, US Treasury Secretary Scott Bessent claims that "Over the next couple of weeks we're going to have several large [trade] deals announced." Adds that "We expect we will be negotiating with China in person again." Notable that Bessent is touring studios this morning (appeared on Fox News earlier) hours after US President Donald Trump issued a Truth Social post threatening 50% tariffs on EU. Treasury Sec has been deployed in the past during periods of market turbulence on tariffs.

MNI TARIFFS: US' Bessent-Hope 50% Tariff Rate 'Lights Fire Under EU' To Reach Deal

Speaking to Fox News, US Treasury Secretary Scott Bessent says that President Donald Trump "believes EU proposals [on trade and tariffs] have not been of good quality". Says the Trump move to impose 50% tariffs on the EU is in response to the Union's slow pace in talks. Bessent: "We hope this lights a fire under the EU....the EU has a collective action problem." Bessent claims that the "US is far along in trade talks with India and other Asian countries...most countries are negotiating in good faith except the EU." Says that the deals are "moving quickly".

MNI TARIFFS: 50% EU Tariffs Would Have Big PCE, GDP Hit: Yale Budget Lab's Tedeschi

The Yale Budget Lab's Ernie Tedeschi publishes (on X.com) some early estimates of the economic impact on the US of a 50% reciprocal tariff on EU imports (vs the 10% baseline). Some selected findings:

- "Pre-substitution tariff rate would be the highest since 1909 under a 50% EU 'reciprocal' tariff. The post-substitution rate would be the highest since 1910."

- "The pre-substitution average effective US tariff rate rises from 15.4% now to 19.5%/Post-substitution, the average rate rises from 14.0% to 18.3%". As explained by the Yale Budget Lab, "pre-substitution metrics (before consumers and businesses shift purchases in response to the tariffs) / post-substitution (after they shift)"

- "Short-run PCE price-level pressures rise by another 0.5pp, from 1.7% to 2.2%"

- "The hit to real GDP growth over 2025 grows by 0.2pp, to -0.84pp"

- "The effect on the unemployment rate in 2025 Q4 rises by 0.1pp, to +0.44pp"

- "Leather product prices (handbags & shoes) rise 40% in the short-run & stay persistently 18& higher.

- "Apparel prices is 31% higher in the short-run &15% higher in the long-run...Electronics prices are 31% in the near-term & stay 11% higher."

US TSYS

US TSYS: Unwinding Early Tariff-Tied Headline Risk

- Early Friday headline risk on tariffs again - spurred a fast risk-off reaction in markets after Pres Trump's unexpected 25% tariff threat on Apple followed by 50% tariffs on EU this morning.

- Treasuries gapped higher, Jun'25 10Y tapped 110-17.5 high (10Y yld 4.4456% low) while SPX emins traded down to 5756.5 from 5858.75 prior to the headlines. Both spent much of the session gradually unwinding the moves -

- Mollified to a degree after after Tsy Sec Bessent claimed that the "US is far along in trade talks with India and other Asian countries...most countries are negotiating in good faith except the EU," adding that the deals are "moving quickly".

- Heavy volumes on the day (TYM5 over 3.7M) tied to Jun'25/Sep'25 roll, Sep takes lead quarterly next Friday.

- The prevailing theme of dollar weakness in recent months played out again this week, prompting the Bloomberg dollar index to fall ~1.65% this week and print fresh yearly lows in the process.

- Extended weekend with Monday's Memorial Day holiday. Tuesday Data Calendar: Durables, Cap Goods, Consumer Confidence, split times for Tsy bills and 2Y Note auctions next Tuesday.

OVERNIGHT DATA

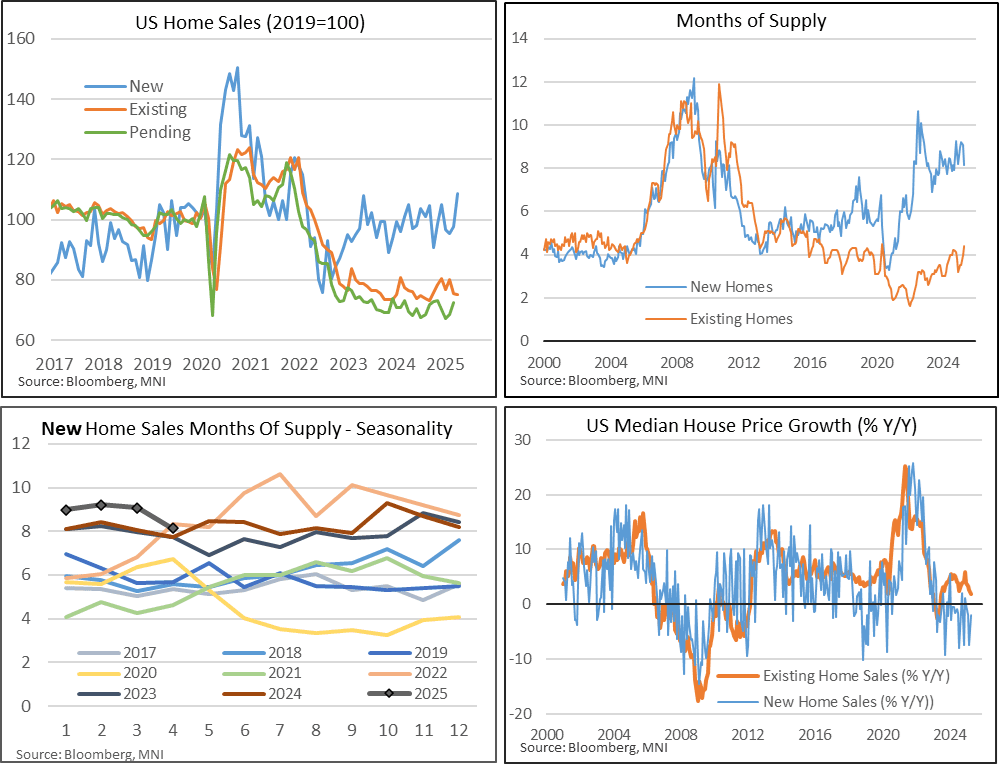

MNI US DATA: New Home Sales Surprisingly Step Above Recent Ranges

- New home sales were far stronger than expected in April at a seasonally adjusted annualized 743k (cons 695k) as they increased from a downward revised 670k (initial 724k) in March.

- It left a 10.9% M/M bounce vs expectations of -4.0% but the prior 7.4% increase was downgraded to 2.6%. That’s a very different profile to existing home sales (-0.5% Apr after -5.9% Mar).

- It’s a new recent high for new home sales, last higher in early 2022 and 8.5% above average 2019 levels. In contrast, existing home sales are 25% below 2019 levels.

- Regional details point to typically wide ranges (from 35% M/M for the Midwest to -15% northeast) but three of the four increased and by far the largest, the south, increased by 12%.

- Relative supply fell to 8.1 months after three months in the low 9s although previous strong increases in inventory meant relative supply was the highest for an April since 2022 and before that 2009.

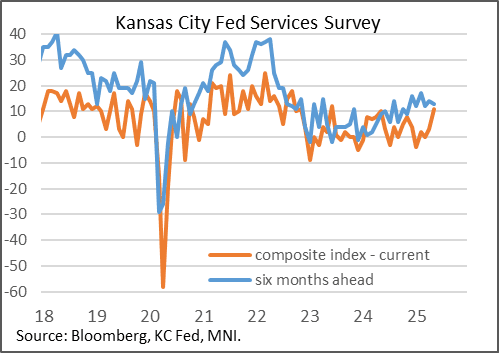

MNI US DATA: KC Fed Services Sees Surprising Strength In May

The Kansas City Fed's services sector survey showed a strong rebound in the composite index to 11 in May from 3 prior, marking a 23-month high. The 6-month outlook however ticked 1 point lower to 13. The KC Fed survey has been a bit of an outlier versus other regional Fed reports, generally seeing less volatility in either direction throughout the last few months of tariff policy uncertainty.

- Each of the regional surveys for May so far (as well as flash PMI) have shown an improvement in services activity, though the rise in KC is especially impressive, with the current index catching up to prior relative optimism (6-month outlook) rather than the other way around. Additionally, input inflationary pressures softened (to 43 from 49) though selling prices rose (to 18 from 16).

MNI CANADA DATA: Retail Sales Grow In March And April Despite Tariff Threats

Retail sales grew in March and April even as economists said consumer confidence would be hit by U.S. tariff threats. Sales +0.8% in March, and April flash estimate +0.5%, StatsCan said Friday. March sales gain was broad-based across 6 of 9 categories, and only significant decline was led by a drop in gasoline prices. Big-ticket spending led March increase with new cars +5.2%. Unclear if consumers wanted to buy before any potential tariffs on autos or a sign of unexpected confidence. Sales also grew for furniture, electronics and appliances.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 191.85 points (-0.46%) at 41668.77

S&P E-Mini Future down 30.75 points (-0.53%) at 5826

Nasdaq down 153.1 points (-0.8%) at 18772.2

US 10-Yr yield is down 1.8 bps at 4.511%

US Jun 10-Yr futures are up 9.5/32 at 110-4

EURUSD up 0.0079 (0.7%) at 1.136

USDJPY down 1.5 (-1.04%) at 142.51

Gold is up $69.54 (2.11%) at $3364.07

European bourses closing levels:

EuroStoxx 50 down 98.17 points (-1.81%) at 5326.31

FTSE 100 down 21.29 points (-0.24%) at 8717.97

German DAX down 369.59 points (-1.54%) at 23629.58

French CAC 40 down 130.04 points (-1.65%) at 7734.4

US TREASURY FUTURES CLOSE

3M10Y -1.048, 16.552 (L: 9.631 / H: 17.619)

2Y10Y -1.889, 51.555 (L: 50.62 / H: 57.097)

2Y30Y -0.645, 103.979 (L: 101.475 / H: 111.455)

5Y30Y +0.998, 95.445 (L: 92.337 / H: 100.562)

Current futures levels:

Jun 2-Yr futures up 0.5/32 at 103-10.25 (L: 103-09.5 / H: 103-15.125)

Jun 5-Yr futures up 5.75/32 at 107-23 (L: 107-18.25 / H: 108-01)

Jun 10-Yr futures up 9.5/32 at 110-4 (L: 109-28.5 / H: 110-17.5)

Jun 30-Yr futures up 16/32 at 111-22 (L: 111-08 / H: 112-16)

Jun Ultra futures up 14/32 at 114-8 (L: 113-30 / H: 115-12)

MNI US 10YR FUTURE TECHS: (M5) Key Support Remains Exposed

- RES 4: 112-20+ High May 1 and a bull trigger

- RES 3: 112-01+ High May 2

- RES 2: 111-22 High May 7

- RES 1: 110-21+ High May 16 and a key near-term resistance

- PRICE: 110-01 @ 1120 ET May 23

- SUP 1: 109-13 Low May 22

- SUP 2: 109-08 Low Apr 11 and key support

- SUP 3: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 4: 108-21 Low Feb 19

A bear cycle that started early May in Treasury futures remains in play. The recent breach of 110-01+, 76.4% of the Apr 11 - May 1 bull leg, strengthened a bearish theme and has exposed key support at 109-08, the Apr 24 low and a bear trigger. Key near-term resistance has been defined at 110-21+, the May 16 high. A move above this level is required to signal a potential reversal.

SOFR FUTURES CLOSE

Jun 25 steady at 95.683

Sep 25 -0.015 at 95.875

Dec 25 -0.015 at 96.145

Mar 26 +0.015 at 96.385

Red Pack (Jun 26-Mar 27) +0.035 to +0.065

Green Pack (Jun 27-Mar 28) +0.050 to +0.065

Blue Pack (Jun 28-Mar 29) +0.050 to +0.060

Gold Pack (Jun 29-Mar 30) +0.060 to +0.065

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.26% (+0.00), volume: $2.540T

- Broad General Collateral Rate (BGCR): 4.26% (+0.00), volume: $1.046T

- Tri-Party General Collateral Rate (TCR): 4.26% (+0.00), volume: $1.017T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $302B

FED Reverse Repo Operation

RRP usage recedes to $154.841B this afternoon from $173.018B yesterday, total number of counterparties at 39. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Outperform On Trump Tariff Threat

European yields fell sharply Friday as EU-US trade tensions ratcheted up.

- After a fairly subdued start to the session, global core FI soared in a risk-off move after US President Trump first threatened to place 25% tariffs on Apple phone imports, before then "recommending a straight 50% Tariff on the European Union, starting on June 1".

- There was no word as to the outcome of a call between EU Trade Commissioner Sefcovic and US Trade Representative Greer which was to have taken place within an hour before the European cash close.

- Bunds outperformed Gilts in the aftermath of Trump's tariff pronouncement, with the UK seen relatively insulated given the recent US-UK trade agreement. Additionally, UK retail sales data surprised to the upside (for the 4th consecutive month).

- Periphery / semi-core EGB spreads widened modestly on the day, though off the widest levels of the session. There was some attention on Moody's review of Italy after hours Friday (current rating Baa3; Outlook Stable).

- On the week, both the German and UK curves steepened: the UK's twist steepened (2Y -2.2bp, 10Y +3.2bp), with Germany's bull steepening (2Y -9.1bp, 10Y -2.3bp).

- Monday is a market holiday in the UK, while the key data highlight the rest of the week is flash May inflation in multiple Eurozone countries.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 6.7bps at 1.764%, 5-Yr is down 7.5bps at 2.097%, 10-Yr is down 7.6bps at 2.567%, and 30-Yr is down 6.3bps at 3.088%.

- UK: The 2-Yr yield is down 4.8bps at 3.983%, 5-Yr is down 7.1bps at 4.13%, 10-Yr is down 7bps at 4.681%, and 30-Yr is down 7bps at 5.48%.

- Italian BTP spread up 0.8bps at 101.7bps / French OAT up 1.5bps at 69.5bps

MNI FOREX: Bloomberg Dollar Index Extends Weekly Decline, Fresh 2025 Lows

- The prevailing theme of dollar weakness in recent months played out again this week, prompting the Bloomberg dollar index to fall ~1.65% this week and print fresh yearly lows in the process. Weakness Friday was in play across the Asian session, but then was exacerbated by renewed tariff related concerns.

- President Trump announced he would be recommending a 50% straight tariff on the EU, and while the Euro did initially come under moderate pressure, the statement appears to have further weighed on the greenback. This dynamic has been assisted by Treasury Secretary not necessarily categorising the USD as weak, bolstering the offered tone for dollar indices.

- Safe havens have performed well with the likes of USDJPY and USDCHF falling just shy of 1%. In late session trade, USDJPY has traded steadily in a 142.50-90 range, consolidating its near 4% sell-off from last week’s highs and a 2% decline this week. The immediate focus is on 142.36, the May 6 low, of which a breach would signal scope for a deeper retracement towards 139.89, the Apr 22 low and key support.

- However, it’s the antipodeans that have outperformed despite the risk-off tone for equities, with AUD and NZD rising 1.3% and 1.45% respectively on Friday. AUDUSD trend signals remain bullish. The recent consolidation phase appears to be a triangle formation - a bullish continuation signal. Attention is on key resistance at 0.6515, the May 7 high.

- Looking across Thursday and Friday, GBP stands out as one of the key outperformers, allowing cable to print above the 1.35 handle, a level not seen since February 2022. Technical breaks have emboldened the price action, following the breach of the bull trigger at 1.3444, the Apr 28 / 29 high. The next point on the chart is at 1.3550 - the Feb 24 ’22 high.

- Next week’s economic calendar is headlined by US PCE/GDP and the RBNZ May decision.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/05/2025 | 0600/0800 | ** | PPI | |

| 26/05/2025 | 0700/0900 | ** | PPI | |

| 26/05/2025 | 1300/1500 | ECB's Lagarde On Europe's Role In A Fragmented World | ||

| 27/05/2025 | 2301/0001 | * | BRC Monthly Shop Price Index |