MNI ASIA MARKETS ANALYSIS: Year-End Rate Cut Pricing Rises

HIGHLIGHTS

- Treasuries looked to finish near midday highs Thursday, off lows after a deluge of data came in on the weaker side of expectations, with retail sales disappointing and monthly PPI registering negative readings.

- The greenback held to lower, narrow channel while stocks recovered from early selling as focus turns to Friday's round of data: Housing Starts, Building Permits, Import/Export Prices, UoM Sentiment & TIC Flow.

- Fed Governor Barr (permanent FOMC voter) as usual has little to say about current monetary policy in opening remarks at a small business event.

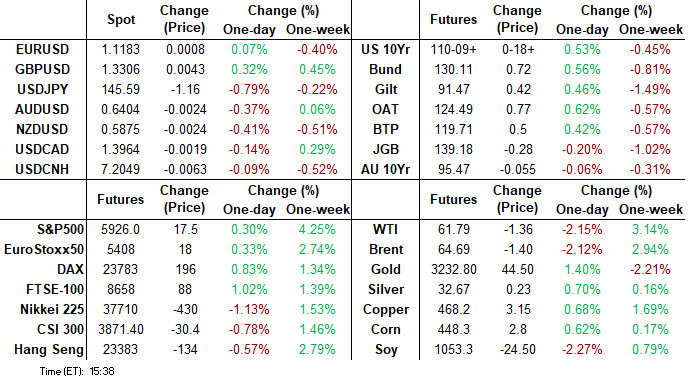

- Projected rate cut pricing near year end gained slightly vs. morning levels (*) as follows: Jun'25 steady at -2.1bp, Jul'25 at -10.3bp (-9.8bp), Sep'25 at -25.1bp (-22.8bp), Oct'25 at -38.3bp (-35.3bp), Dec'25 at -54.9bp (-50.0bp).

US TSYS

MNI US TSYS: Yields Decline Following Heavy Deluge Economic Data

- Treasuries look to finish near late Thursday session highs, well off early session lows after this morning's heavy round of economic data: PPI lower than expected (priors up-revised, however), retail sales largely in line w/ prior up-revised, weekly claims largely in-line.

- Core PPI (ex food, energy & trade services) inflation was surprisingly soft at 0.11% M/M (cons 0.3) after only a slightly upward revised 0.17% (initial 0.12) in March. Rather than showing input costs kicking higher with the implementation of reciprocal tariffs in April, the pattern of recent weakness in March and April after some strength through Dec-Feb (when it averaged 0.39% M/M) suggests tariff front-running was more inflationary.

- Additionally, Industrial and manufacturing production was a little weaker in April than expected, but while there was a pullback there was no collapse despite plummeting sentiment/survey indicators in the month. Philadelphia Fed's Manufacturing Business Outlook Survey saw a strong improvement in the headline General Business Conditions Index in May, rising 22.4 points to to a still-contractionary -4.0 (-11.0 expected, -26.4 prior).

- Currently, the Jun'25 10Y contract trades +18 at 110-09 vs. 110-11 high, still off initial technical resistance at 110-29 20-day EMA. Curves steeper in intermediates to long end: 5s30s +4.603 at 84.708. Tsy 10Y yield -.0891 at 4.4472%.

- Focus turns to Friday's data: Housing Starts, Building Permits, Import/Export Prices at 0830ET; U. of Mich. Sentiment at 1000ET followed by TIC Flow data at 1600ET.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (-0.01), volume: $2.543T

- Broad General Collateral Rate (BGCR): 4.28% (-0.01), volume: $1.066T

- Tri-Party General Collateral Rate (TCR): 4.28% (-0.01), volume: $1.028T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $288B

FED Reverse Repo Operation

RRP usage retreats to $109.436B this afternoon from $165.024B yesterday, total number of counterparties at 25. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks continued to report mixed SOFR options Thursday while Treasury options leaned toward better 10Y put volume in Jun'25 & Jul'25. Underlying futures extended highs while projected rate cut pricing near year end gained slightly vs. morning levels (*) as follows: Jun'25 steady at -2.1bp, Jul'25 at -10.3bp (-9.8bp), Sep'25 at -25.1bp (-22.8bp), Oct'25 at -38.3bp (-35.3bp), Dec'25 at -54.9bp (-50.0bp).

SOFR Options:

-4,000 SFRZ5 97.00/97.50/98.00 call flys, 2.0 ref 96.215

+10,000 0QZ5 97.50/97.62 call spds, 2.0 ref 96.645/0.05%

-8,000 SFRM5 96.75 calls, 34.5 vs. 96.52/0.42%

Block, 7,000 SFRV5 95.68 puts, 2.75 ref 96.20

Block, +7,500 SFRU6 97.00/97.50 call spds vs. 15,000 0QU5 97.25/97.75 call spds, 2.5 net

-10,000 SFRU5 95.50 puts, 0.5 vs. 95.96/0.05%

+10,000 SFRZ5 95.37/95.50 put spds, 0.75 ref 96.21

+6,000 SFRZ6/0QZ5 96.75 call spds vs. 3,000 SFRZ6/0QZ5 97.25 call spds, 21 net

Block/pit: -32,000 SFRU5 96.00/96.25/96.50 call flys, 2.5 ref 95.93 to -.935

-5,000 SFRZ5 96.75/97.25 call spds, 5.0 ref 96.165

+3,000 SFRZ5 95.50/95.56/95.68 broken put flys, 1.5 ref 96.16

-3,000 2QK5 95.62 calls, 0.5

+1,000 SFRZ5 96.50/97.00 2x3call spds, 7.5

-5,000 SFRU5 95.56/95.68/95.75/95.87 put condors, 5.0 vs. 95.97/0.05%

-4,000 SFRM5 95.75 puts, 7.0

2,200 0QM5 96.12/96.31 put spds ref 96.46

Treasury Options:

3,900 wk3 TY 109.5 puts, 1 ref 110-05.5

2,000 TYM5 113 calls, 1 ref 110-06

6,000 TYM5 109.25/109.75, 4 ref 110-05.5

1250 TYM5 110.5/111 1x2 call spds

2,000 TYU5 108/112 strangles

2,500 TYN5 108/109 put spds, 20

20,000 TYM5 109.5 puts, 17 ref 109-26.5

2,000 TYQ5 107.5/109 put spds ref 109-26.5

2,400 TYM5 111.5/TYN5 110.5 call spds

+7,000 TYN5 107/108.5 put spds vs. TYM5 107.5/109 put spds, 10 net/Jul over

-2,000 TYM5 110/110.5/111/111.5 call condors, 5

+1,000 USM5 113.5/114 call spds, 9 vs. 112-18/0.06%

+2,000 TYN5 107.5/108.5 put spds, 14

-1,500 TYM5 109/110/111 put flys

-3,000 wk3 TY 110.5/111.75 1x3 call spds, 0.0

+2,000 TYU5 107.5/112.5 call over risk reversals, 2 vs. 110-00.5/0.52%

+3,000 wk3 TY 111 calls, 1 vs. 109-23.5/0.05%

Block/screen, appr +40,000 TYN5 107.5/108.5 put spds, 14-15 ref 109-21.5 to -22.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Core FI Finally Catches A Bid

European yields fell Thursday, with cash core FI ending a 5-session losing streak, including 10Y Bund yields falling the most since Jan 15.

- Yields fell in almost uninterrupted fashion through the session, with the biggest fall of the day coming in early afternoon after a slew of US data which pointed overall to both softer inflationary pressures and weaker growth than anticipated.

- The German finance ministry announced a more modest downward revision to expected tax revenue over the next 5 years than had been speculated, helping underpin Bunds.

- UK Q1 GDP and monthly economic activity data was noisy and had little market read-through. Meanwhile Eurozone Q1 GDP was revised slightly downward, while industrial production beat expectations in March (largely on a volatile Irish print).

- The UK and German curves each bull flattened on the day, though German belly outperformance was notable.

- Periphery / semi-core EGB spreads mostly narrowed, with Greece the outlier with some modest widening. BTPs briefly dipped through 100bp vs Bund for the first time since 2021 but weakened after a Bloomberg sources piece saying Italian PMI Meloni wants to reduce payroll taxes in next year's budget.

- Friday's calendar includes French labour market data and Italian and Eurozone trade figures, with appearances by ECB's Lane and Vujcic and BOE's Lombardelli.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 6bps at 1.88%, 5-Yr is down 7.9bps at 2.19%, 10-Yr is down 7.7bps at 2.622%, and 30-Yr is down 8bps at 3.066%.

- UK: The 2-Yr yield is down 3.6bps at 3.988%, 5-Yr is down 4.3bps at 4.141%, 10-Yr is down 5.3bps at 4.66%, and 30-Yr is down 5.9bps at 5.41%.

- Italian BTP spread down 0.7bps at 100.5bps /Greek up 1.5bps at 78bps

MNI EGB OPTIONS: Upside Lean In Rates Trade Thursday

Thursday's Europe rates/bond options flow included:

- ERQ5 98.1875/98.3125/98.4375c fly, bought for 1.75 in 8k total

- SFIZ5 96.35/96.65cs vs 96.00p, bought the cs for -1.5 (receive) in 10k

- SFIZ5 96.40/96.50cs vs 96.10/96.00ps, bought the cs for flat in 4.5k

MNI FOREX: Japanese Yen Outperforms amid Move Lower for Core Yields

- The plethora of US data releases on Thursday came in on the weaker side of expectations, with retail sales disappointing and monthly PPI registering negative readings. US yields have moved significantly lower in sympathy and while the USD index does reside in negative territory, greenback moves have been very modest in comparison.

- This doesn’t tell the whole story in G10, where there has been mixed performance. The Japanese yen is outperforming, owing to US yields sliding 10bps lower in the belly of the curve. USDJPY is 0.75% lower around 145.65 as we approach the APAC crossover. Lows for the session were 145.42, however, we note the pair is yet to close the gap to last Friday’s close at 145.37. This level will remain in short-term focus, before 145.10, the 20-day EMA. Overall, the latest USDJPY pullback underpins the view that gains since Apr 22 appear corrective.

- Underperformance for the higher beta currencies in G10, such as the antipodeans sees the likes of AUDJPY and NZDJPY falling around 1.2% today. For AUDJPY, the prior trendline resistance break now provides solid support around the 93.00 handle, with both the 20- and 50-day exponential moving averages intersecting just below this mark.

- Stronger-than-expected UK growth data has only provided a modest boost to GBP, with cable hovering just below the 1.33 mark. A continuation higher would refocus attention on the key resistance and a bull trigger, at 1.3444, the Apr 28 / 29 high.

- In emerging markets, USDZAR (-1.3%) has fallen close to its worst level of the year at 18.0081, the Mar 18 low, and is now nearly 10% lower compared to April’s all-time high. Moderate greenback weakness and a solid recovery in spot gold through the European session have provided tailwinds for the rand, with sights turning to next support at 17.6191, the Dec 12 2024 low.

- Japan GDP and NZ inflation expectations cross tomorrow, before US import prices and building permits highlight the US calendar. SNB’s Schlegel is also due to speak Friday.

MNI US STOCKS: Late Equities Roundup: Consumer Staples & Utilities Outperforming

- Stocks remain mostly higher late Thursday, well off morning lows after the heavy round of economic data: PPI lower than expected (priors up-revised, however), retail sales largely in line w/ prior up-revised, weekly claims largely in-line. Currently, the DJIA trades up 242.29 points (0.58%) at 42292.98, S&P E-Minis up 24.25 points (0.41%) at 5933, while the Nasdaq trades down 39.5 points (-0.2%) at 19106.99.

- Consumer Staples and Utility sectors continue to outperform in late trade, leading gainers in the former included Dollar General +4.94%, Coca-Cola +2.96%, Altria Group +2.80% and Hormel Foods +2.30%.

- Leading gainers in the Utility sector included NextEra Energy +2.90%, Xcel Energy +2.75%, CMS Energy +2.69% and Duke Energy Corp +2.46%.

- Conversely, Consumer Discretionary and Energy sectors continued to underperform, stocks weighing on the Discretionary sector included Amazon.com -2.56%, MGM Resorts -1.83%, Norwegian Cruise Line -1.65% and Caesars Entertainment -1.40%.

- Oil and gas stocks were pressured by weaker crude prices (WTI -1.52 at 61.63): APA -3.47%, Diamondback Energy -2.63%, Halliburton -1.81% and Occidental Petroleum -1.78%. Notable mention, the Health Care sector was weighed down by UnitedHealth -12.86%, amid reports they were under investigation for Medicare fraud.

MNI EQUITY TECHS: E-MINI S&P: (M5) Trend Signals Point North

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5944.50 Intra day high

- PRICE: 5929.50 @ 1509 ET May 15

- SUP 1: 5658.48 50-day EMA

- SUP 2: 5455.50 Low Apr 30

- SUP 3: 5355.25 Low Apr 24

- SUP 4: 5127.25 Low Apr 21 and a key support

A bullish trend condition in S&P E-Minis remains intact and this week’s appreciation reinforces current conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5658.48, the 50-day EMA.

MNI COMMODITIES: Crude Falls Amid US-Iran Optimism, Gold, Copper Rebound

- WTI is trading lower today on optimism over a US-Iran agreement following earlier comments by Trump, with the market anticipating a potential easing of sanctions on Iran.

- WTI Jun 25 is down by 2.3% at $61.7/bbl.

- Iran currently has 300k to 400k b/d of spare capacity that it could bring back if the US eased sanctions, according to IEA analysis cited by Bloomberg.

- A downtrend in WTI futures remains intact, with initial support at $54.67, the Apr 9 low and bear trigger. On the upside, key resistance to watch is $63.46, the 50-day EMA.

- Meanwhile, spot gold has recovered from earlier session losses, with the yellow metal now up by 1.4% at $3,223/oz. The move brings gold back above the 50-day EMA, which was pierced overnight.

- The earlier move lower allowed for a better entry point for traders amid ongoing medium-term concerns around geopolitical/trade uncertainty and elevated US fiscal pressures.

- The move below the 50-day EMA was still notable, however, strengthening a bearish threat. Today’s session low at $3,120.98 provides initial support, clearance of which would expose $3,085.0, the 76.4% of the Apr 7 - Apr 22 upleg.

- On the upside, initial resistance is $3,263.9, the 20-day EMA.

- Elsewhere, copper has also recovered from earlier losses to trade up by 0.9% at $469/lb.

- Key short-term resistance has been defined at $498.25, the Apr 23 high. A resumption of weakness would expose $436.00, the Apr 10 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/05/2025 | 0730/0930 | ECB's Cipollone At EU Cyber Resilience Board Meeting | ||

| 16/05/2025 | 0800/1000 | *** | HICP (f) | |

| 16/05/2025 | 0900/1100 | * | Trade Balance | |

| 16/05/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/05/2025 | 1230/0830 | New York Fed's Roberto Perli | ||

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 16/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 16/05/2025 | 1500/1700 | ECB's Lane On Central Bank Communication Panel | ||

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 2000/1600 | ** | TICS | |

| 16/05/2025 | 0140/2140 | San Francisco Fed's Mary Daly |