COMMODITIES: Crude Falls Amid US-Iran Optimism, Gold, Copper Rebound

May-15 18:52

- WTI is trading lower today on optimism over a US-Iran agreement following earlier comments by Trump, with the market anticipating a potential easing of sanctions on Iran.

- WTI Jun 25 is down by 2.3% at $61.7/bbl.

- Iran currently has 300k to 400k b/d of spare capacity that it could bring back if the US eased sanctions, according to IEA analysis cited by Bloomberg.

- A downtrend in WTI futures remains intact, with initial support at $54.67, the Apr 9 low and bear trigger. On the upside, key resistance to watch is $63.46, the 50-day EMA.

- Meanwhile, spot gold has recovered from earlier session losses, with the yellow metal now up by 1.4% at $3,223/oz. The move brings gold back above the 50-day EMA, which was pierced overnight.

- The earlier move lower allowed for a better entry point for traders amid ongoing medium-term concerns around geopolitical/trade uncertainty and elevated US fiscal pressures.

- The move below the 50-day EMA was still notable, however, strengthening a bearish threat. Today’s session low at $3,120.98 provides initial support, clearance of which would expose $3,085.0, the 76.4% of the Apr 7 - Apr 22 upleg.

- On the upside, initial resistance is $3,263.9, the 20-day EMA.

- Elsewhere, copper has also recovered from earlier losses to trade up by 0.9% at $469/lb.

- Key short-term resistance has been defined at $498.25, the Apr 23 high. A resumption of weakness would expose $436.00, the Apr 10 low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Gold Holds Near Record High, Crude Edges Down

Apr-15 18:34

- Gold has traded in a relatively tight range for much of today, with the yellow metal holding close to yesterday’s record high amid continued tariff uncertainty.

- Spot gold is currently up by 0.5% at $3,228/oz, less than $20 below Monday’s all-time high of $3,245.7.

- Goldman Sachs expects gold to rally to $3,700 by the end of this year and $4,000 by mid-2026, while UBS sees it reaching $3,500 by year-end, supported by continued central bank demand, recession risks and trade and geopolitical uncertainties.

- From a technical perspective, the trend condition in gold remains bullish, with sights on $3,291.8 next, a Fibonacci projection.

- Meanwhile, crude has held relatively steady through the day as the market weighs global oil demand risks.

- Both OPEC and the IEA have cut their demand forecasts, while sentiment that Europe will reach a deal with the US on tariffs has weakened. Ongoing discussions between the US and Iran adds further uncertainty.

- WTI May 25 is down by 0.4% at $61.3/bbl.

- A bearish theme in WTI futures remains intact and recent weakness has resulted in the breach of a number of important support levels, reinforcing a bearish threat.

- A resumption of the bear cycle would open $54.26, a Fibonacci projection. Initial firm resistance is seen at $64.85, the Mar 5 low and a recent breakout level.

ECB VIEW: Downside Inflation Risks Have Grown Since March ECB [2/2]

Apr-15 18:33

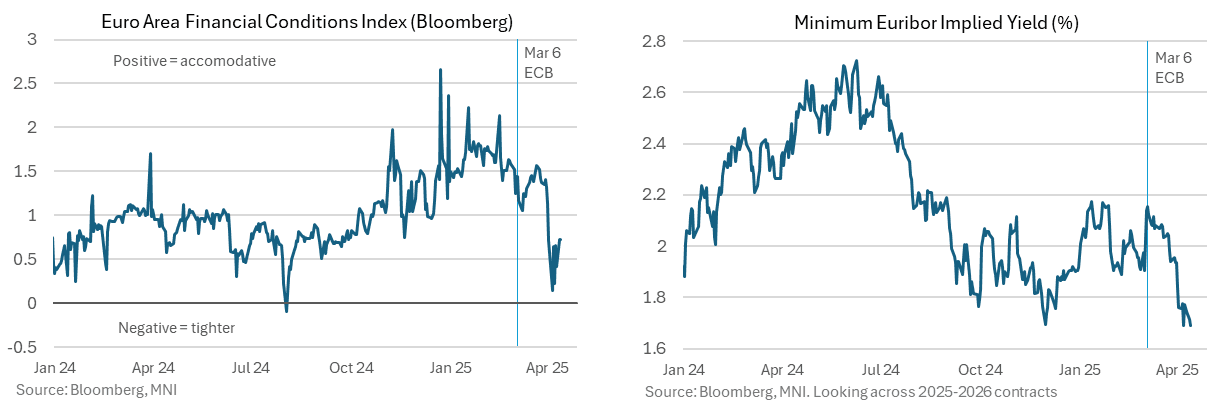

- On top of this euro appreciation, financial conditions have tightened as equities have tumbled since President Trump’s “Liberation Day” tariff announcements and 5Y5Y inflation swaps have fully reversed the 15bp push higher seen on the defence and infra spending plans.

- Whilst there has been some tariff reprieve for the European Union with Trump’s 90-day ‘pause’ at a reciprocal rate of 10% rather than 20%, the huge 145% tariffs imposed by the US on China has further bolstered the risk that “a re-routing of exports into the euro area from countries with overcapacity would put downward pressure on inflation.”

- Our policy team has been closely following this amongst other areas - see MNI: Europe to Sharpen Trade Tools To Tackle Dumping (Feb 24) and MNI: EU To Keep China Option In Reserve As Seeks US Deal (Apr 11).

- The combination sees terminal rate expectations close to cycle lows heading into the meeting, roughly consistent with a policy rate bottoming out below 1.6%.

- It should also see the Governing Council hawks having a little less sway in this meeting’s communications but would also make any hawkish skew more notable.

ECB VIEW: Downside Inflation Risks Have Grown Since March ECB [1/2]

Apr-15 18:31

The below is taken from the MNI ECB Preview [see the full report here]

- Inflation risks were two-sided amidst heightened uncertainty and might continue to be viewed as such although one potential upside risk has clearly not materialised: a weaker euro.

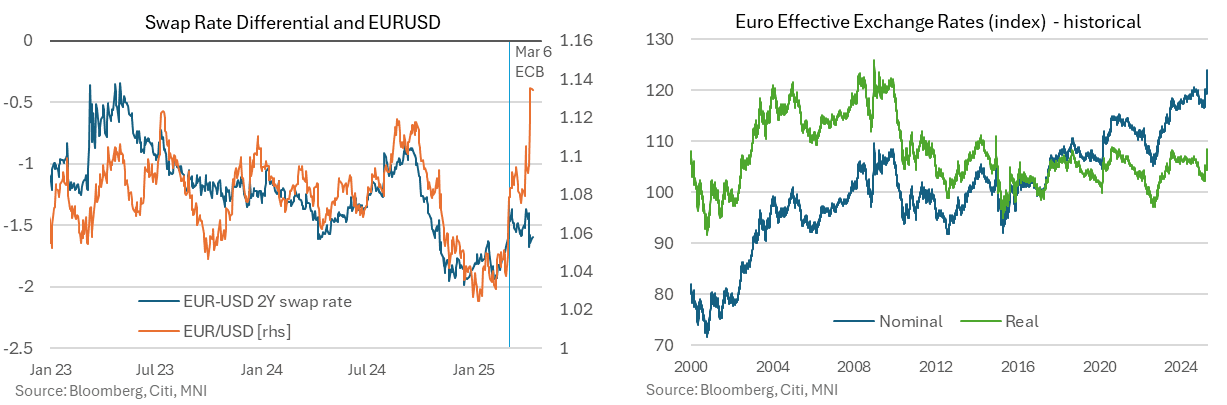

- The March statement noted “A general escalation in trade tensions could see the euro depreciate and import costs rise” but the euro has instead seen another leg higher after appreciating in early March on defence and infra spending announcements.

- EUR/USD has surged closer to 2022 highs whilst the euro on a trade-weighted basis is at highs since the creation of the single currency (although much less historically elevated in real terms with its lower historical inflation than many of its trading partners).

- Note the rare disconnect with rate differentials.