MNI ASIA MARKETS ANALYSIS: US$ Rebound, French Confidence Vote

HIGHLIGHTS

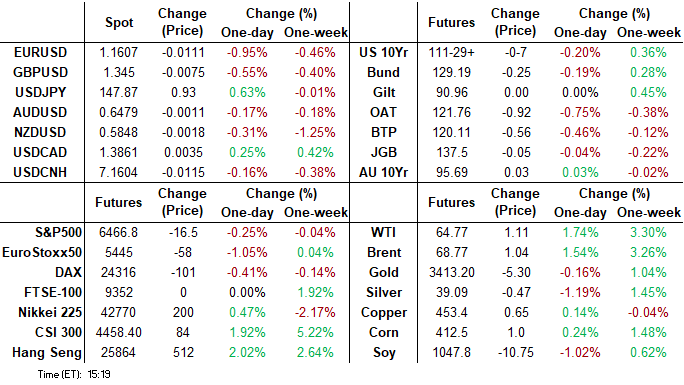

- Treasuries opened weaker - scaling back a fair portion of Friday's post-Chair Powell speech in Jackson Hole that left the door open to a possible rate cut at the next FOMC annc on September 17.

- Treasury futures maintained losses after higher than expected new home sales - but climbed back to mildly weaker levels on the open.

- NEC director Kevin Hassett (potential Fed Chair candidate) tells CNBC that Chair Powell's Jackson Hole speech showed a Fed that is "late" to cut but that Powell's presentation was "sound" and "data driven".

- US$ continued to climb in late trade, recovering appr half of Friday's decline. Today's move said to be EUR related after the French confidence vote call earlier.

US TSYS

MNI US TSYS: Tsys Retreat, Greenback Bounce, Both Unwind Half Fri's Post Powell Move

- Relatively quiet start to the week with London out for annual bank holiday. Treasuries opened weaker - scaling back a fair portion of Friday's post-Chair Powell speech in Jackson Hole that left the door open to a possible rate cut at the next FOMC annc on September 17.

- NEC director Kevin Hassett (potential Fed Chair candidate) tells CNBC that Chair Powell's Jackson Hole speech showed a Fed that is "late" to cut but that Powell's presentation was "sound" and "data driven".

- Treasury futures maintained losses after higher than expected new home sales - but climbed back to mildly weaker levels on the open. After the bell, Se'25 10Y contract trades -6.5 at 111-30 vs. 111-27.5 low. Support around the 50-day EMA, at 111-13. A clear break of this average would expose support at 110-23+, the Aug 1 low.

- The June reading of 652k (seasonally-adjusted, annualized) was better than the 630k Bloomberg consensus, but actually represented a slight fall (-0.6%) on the month due to a sizeable upward revision to June to 656k (from 627k).

- July's building permits were revised up in the final reading to 1,362k (annualized, seasonally-adjusted), vs 1,354k in the initial estimate. That got the data a little closer to the 1,386k consensus estimate going into the initial reading last week, though either way it is a pullback from 1,393k in June (a 2.2% fall vs the 2.8% initially recorded).

- US$ continued to climb in late trade, recovering appr half of Friday's decline. Today's move said to be EUR related after the French confidence vote call earlier. The Bbg $ index: BBDXY +5.94 at 1207.43 vs. 1201.02 low.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.04), volume: $2.738T

- Broad General Collateral Rate (BGCR): 4.35% (+0.04), volume: $1.143T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.04), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

FED Reverse Repo Operation

RRP usage rises to $47.567B this afternoon from $36.275B Friday -- compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021. Total number of counterparties at 23. This year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options looked mixed on net late Monday, SOFR Calls mixed while Treasury options saw decent buying in Oct 10y calls. Underlying had pared appr half of Friday's post-Powell speech support by late morning - inched off lows during the second half. Projected rate cuts contract slightly vs. early morning (*) levels: Sep'25 at -20.8bp (-21.2bp), Oct'25 at -33.9bp (-34.1bp), Dec'25 at -52.9bp (-53.0bp), Jan'26 at -65.6bp (-65.9bp).

SOFR Options:

3,000 SFRU5 95.75/95.81/95.87 put flys, 0.5 vs. 95.875/0.05%

-5,000 SFRM6 96.75/97.00 call spds w/ 96.50/97.00/97.50 call flys, 17.5 total

-4,000 SFRZ6 96.25 puts, 20.0 vs. 96.925/0.32%

-5,000 SFRZ5 95.75/95.81 put spds, 0.5

+2,000 SFRZ5 95.75/95.87/96.00 call flys, 2.0 ref 96.20

+4,000 SFRV5 96.93 calls, 1.0 ref 96.20

+5,000 SFRV5 96.43/96.50 call spds, 1.0 ref 96.23/0.05%

+4,000 0QH6 97.25/97.50/97.75 call trees, .25

+4,000 SFRZ5 95.68/95.81/95.87/96.00 2x2x1x1 put condors, 1.25 ref 96.21

-16,000 2QU5 97.0 calls, 4.4

-1,000 SFRU5 95.87/95.93 straddle strip, 18.5

+10,000 SFRU5 96.06/96.31 call spds, 1.0

+5,000 SFRU5 95.81/95.93/96.06 2x3x1 put flys, 1.25

+2,500 SFRU5 95.87/95.93/96.00/96.03 call condor, 2.5

6,000 SFRU5 95.87 calls 5.75 last

+4,000 SFRV5 96.06/96.18 put spds vs. 96.43 calls, 1.0 net ref 96.21.5

+7,600 SFRV5 96.25/96.37 call spds, 3.5 ref 96.22

Treasury Options:

3,000 TYZ5 113/114.5 1x2 call spds ref 111-29.5

3,700 USZ5 107 puts, 25 ref 114-05

+25,000 TYV5 113.5 calls, 15 vs. 112-00.5/0.19%

+2,500 TYX5 109.5 puts, 11

2,000 USX5 109/112 put spds

over -5,700 TYV5 110 puts, 5-6 last

over 3,700 TYV5 113 calls, 23 last

+1,500 wk5 TY 111/111.5/111.75/112 broken put condors, 4 ref 112-04.5, exp Fri

2,000 FVX5 108/108.25/108.75 put trees, 0.0 ref 109-05

EGBS

MNI BONDS: EGBs-GILTS CASH CLOSE: OAT Spreads Widen Sharply On Confidence Vote

Periphery/semi-core EGB spreads widened amid a broader sell-off Monday, with the Gilt market closed for holidays.

- EGBs were under some pressure in early trade, with Bund yields moving back above the levels seen just prior to Friday's speech by Federal Reserve Chair Powell at Jackson Hole which triggered a broad global bond rally.

- And just over an hour before the European cash close, OATs sold off and Bunds rallied in a risk-off move after French PM Bayrou called for a confidence vote in the government to be held on September 8 (an extraordinary meeting that is two weeks before lawmakers were set to return) in a gambit to get his controversial fiscal legislation passed.

- Having already widened modestly earlier in the session, 10Y OAT/Bund jumped to its widest close since April at 75.2bp.

- Similarly, earlier widening in other periphery EGBs (Italy/Greece most notably) extended after the French news.

- Earlier in the session, German IFO was broadly in line with expectations.

- The belly underperformed on the German curve, in a bear-flattening lean overall.

- Focus for the week is on national/Eurozone flash August inflation data, most of which arrives on Friday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.7bps at 1.975%, 5-Yr is up 3.8bps at 2.315%, 10-Yr is up 3.5bps at 2.757%, and 30-Yr is up 2.3bps at 3.332%.

- Italian BTP spread up 3.4bps at 83.8bps / French OAT up 5.7bps at 75.2bps

MNI US STOCKS: Late Equities Roundup: Steady/Mixed Dow Off Friday Record Highs

- Stocks held near steady in SPX eminis to mixed in late Monday trade, the DJIA underperforming as markets (rates, currency and equities) unwound a portion of Friday's post-Chair Powell related rally.

- After climbing to new record high last Friday (45,757.84), the DJIA trades currently down 281.62 points (-0.62%) at 45350.5, S&P E-Minis down 12.5 points (-0.19%) at 6470.75, Nasdaq up 21.1 points (0.1%) at 21518.51.

- Health Care and Consumer Staples sectors underperformed in late trade, Pharmaceutical stocks weighed on the Health Care sector: Dexcom -6.37%, Moderna -4.90%, Align Technology -3.04%, Regeneron Pharmaceuticals -2.74% and Pfizer -2.61%. Highlight laggers in the staples sector included: Keurig Dr Pepper -10.03%, Estee Lauder Cos -2.85%, Constellation Brands -2.11% and Molson Coors Beverage -2.08%.

- On the positive side, tech stocks continued to lead gainers in late trade: Western Digital +3.51%, Seagate Technology Holdings +3.22%, NVIDIA and Super Micro Computer both +1.89% (Nvidia reports after Wednesday's close). Meanwhile, Interactive media and entertainment shares were buoyed Communication Services: Netflix +1.71%, Alphabet +1.54%, Take-Two Interactive Software +1.40% and Electronic Arts +0.70%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bull Phase Intact

- RES 4: 6600.00 Round number resistance

- RES 3: 6572.45 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and all-time High

- PRICE: 6470.75 @ 14:42 BST Aug 25

- SUP 1: 6362.75 Low Aug 20

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6298.61 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and Friday’s rally reinforces current conditions. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. Attention is on 6508.75, the Aug 15 high and the bull trigger. Clearance of this level would confirm a resumption of the uptrend and open 6523.63, a Fibonacci projection. Support to watch lies at 6298.61, the 50-day EMA.

COMMODITIES

MNI OIL: Americas End of day Oil Summary: Crude Supported by Geopolitical Concerns

Oil markets were supported today amid Russian supply concerns as potential secondary sanctions are touted and Ukraine continues energy strikes on Russia.

- Optimism around a Russia/Ukraine peace deal is once again fading which prompted Trump to renew sanctions threats on Friday and set yet another deadline – this time “within two weeks”

- Ukraine has increasingly struck Russian energy targets this month. Ukrainian attacks on 10 plants disrupted at least 17% of Russia's refinery capacity, or 1.1 million barrels per day, according to Reuters calculations on Monday.

- Slovakian officials said on Monday Russian Druzhba oil flows were expected to return today after Ukraine strikes last Thursday.

- Starting Wednesday, Indian goods to the U.S. face 50% tariffs, heavily impacted by Indian purchases of Russian oil. Although impacted in Jul/Aug, Indian buyers are reported to be coming back for Russian cargoes while officials remain defiant of Washington threats.

- WTI Oct futures were up 1.8% at $64.80

- WTI Nov futures were up 1.7% at $64.30

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/08/2025 | 0600/0800 | ** | PPI | |

| 26/08/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 26/08/2025 | - | DMO to hold FQ3 consultations with investors / GEMMs | ||

| 26/08/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/08/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 26/08/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 26/08/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 26/08/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 26/08/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 26/08/2025 | 1400/1500 | BOE Mann at Banxico Conference (text release) | ||

| 26/08/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 26/08/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 26/08/2025 | 1830/1430 | BOC Governor speech in Mexico City | ||

| 27/08/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 27/08/2025 | 0130/1130 | *** | Quarterly construction work done |