MNI ASIA MARKETS ANALYSIS: Tsys Retreat on Strong Data

HIGHLIGHTS

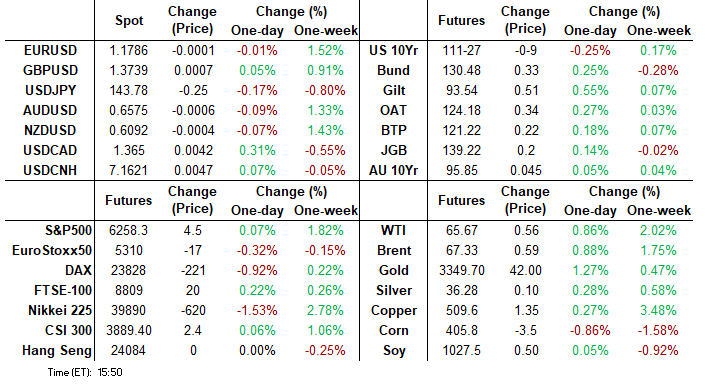

- Treasuries look to finish weaker, briefly off lows after late trade comments from Pres Trump on Japan and India; projected rate cuts into year end retreated from recent highs of nearly -75bp.

- The JOLTS report for May saw stronger than expected job openings whilst quit and hiring rates plus the level of layoffs all pointed to broad stabilization in the labor market rather than showing signs of further moderation.

- Senate narrowly passed the budget bill which heads to House for final vote before heading to Pres Trump on July 4 for signing if it passes.

- USD bounced off early trendline support with US yields following stronger-than-expected US data and an important technical support holding for the DXY, a trendline drawn across the 2011 and 2021 lows.

US TSYS

MNI US TSYS: Late Japan, India Trade Deal Comments Rattle Markets Briefly

- Treasuries look to finish weaker but off lows - drawing some buy interest after Pre Trump commented on trade deals with Japan and India.

- Bloomberg headlines: "DOUBT WE'LL HAVE DEAL WITH JAPAN" , "ON JULY 9 DEADLINE: NOT THINKING ABOUT EXTENDING" while "SUGGESTS JAPAN COULD PAY 30% OR 35% TARIFF".

- Nikkei spun it a little differently: "US TO HANDLE JAPAN LATER IN TARIFF TALKS, PRIORITIZING INDIA".

- Tsy Sep'25 10Y futures trade -7.5 at 111-28.5 after the bell vs. 111-22.5 low, 10Y yield +.0176 at 4.2456%. Curves remain flatter: 2s10s -3.167 at 47.299, 5s30s -3.900 at 93.654.

- The bull cycle in Treasury futures remains intact, however prices reversed hard off highs into the Tuesday close. As such, the contract has failed on the approach to the next important resistance at 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Note that the uptrend is overbought, a pullback would unwind this position. First key support to watch is 111-05+, the 20-day EMA.

- Stocks dipped (SPX emini -3.75 at 6250.0) as did US$ slightly after climbing off morning lows into midday high (BBDXY: 1185.43 low / 1191.23 high).

- Looking ahead: Wednesday data focus on MBA Mortgage Applications at 0700ET, Challenger Job Cuts at 0730 followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.45% (+0.06), volume: $2.946T

- Broad General Collateral Rate (BGCR): 4.39% (+0.02), volume: $1.059T

- Tri-Party General Collateral Rate (TCR): 4.39% (+0.02), volume: $1.038T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $79B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $157B

FED Reverse Repo Operation: Sharp Retreat as July Gets Underway

RRP usage retreats to $245.530B this afternoon from $460.731B yesterday (highest since December 31), total number of counterparties falls to 38 from 62. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported chunky two-way SOFR & Treasury option trade Tuesday, upside call interest evaporating into midday as underlying futures retreated after this morning's ISM Mfg and JOLTS job data. Projected rate cut pricing retreated from early morning (*) levels: Jul'25 steady at -5.3bp, Sep'25 at -28.0bp (-29.3bp), Oct'25 at -44.8bp (-47.3bp), Dec'25 at -63.9bp (-68.4bp).

SOFR Options:

+5,000 SFRU5 95.68/95.87/96.00 put flys, 0.75 ref 95.975

+10,000 SFRZ5 98.00 calls, 2.0

+5,000 SFRH6 96.12/96.50 2x1 put spds, 5.5

5,000 0QQ5 97.18 calls, ref 96.925

Block, 10,000 SFRH6 96.00/96.50 put spds, 18.0

over +45,000 SFRU5 95.87/95.93/96.00/96.12 broken call condors, 0.0 ref 96.00

2,000 0QN5 96.68/96.87 put spds ref 96.94

2,000 SFRN5 96.00/96.25 call spds ref 96.005

Block, 12,000 SFRQ5 96.00/96.12/96.25/96.37 call condors, 2.5 ref 96.005

Block/screen 6,000 SFRU5 95.68/95.75/95.87 2x3x1 put flys, 1.25 net

4,000 0QN5 97.06/97.18 call spds vs. 96.68/96.81 put spds, 0.5 net - call spd over

+4,000 SFRZ5 96.00 straddles, 48.0 vs. 96.35/0.52%

+2,000 SFRQ5 95.81/95.87/96.00 broken put trees, 4

+8,000 SFRU5 96.00/96.12 put spds, 8.5 ref 96.00

+2,000 SFRZ5 96.00/96.25 2x1 put spds, 3.25 ref 96.325

Treasury Options:

+10,000 TUU5 105.12 calls, 3

3,500 TYQ5 112.75/113.25 call spds vs. 111.75/112.25 put spds, 5.0 net/puts over

Block, 18,900 wk1 TY 111.5/112 put spds, 11.0

-4,000 wk2 TY 112.25 straddles, 48 vs. 112-05.5/0.09%

10,000 TYU5 108/110 put spds, 12 ref 112-07.5

-15,000 wk1 FV 109.25/109.5/109.75/110 call condors, 3.5 vs. 109-03.5/0.10%

+2,500 FVU5 105/106.5 put spds, 2.5 vs. 109-01.25/0.04%

+5,000 TYQ5 112.5 calls, 39 vs. 112-10/0.46%

+2,000 TYQ5 110.5/112 call spds vs. 109.5/111.5 put spds, 50 net vs. 112-10/0.54%

+2,000 TYQ5 109 puts, 3 ref 112-04/0.08%

+2,500 TYU5 109.5 puts, 13

-1,500 FVQ5 108.5 puts, 14.5 vsd. 109-01.5/0.29%

+5,000 TYU5 107/108 put spds, 2 ref 112-10.5

+10,000 FVQ5 108 puts, 6.5 ref 109-03.25

+2,000 TYQ5 113.25 calls, 23 vs. 112-10/0.60%

+5,000 wk1 TY 111.25/111.5 put spds, 3 vs. 112-04.5/0.10

MNI BONDS: EGBs-GILTS CASH CLOSE: Flattening To Start The Quarter

European yields pulled back Tuesday in a flattening move.

- There was a strong rally in early trade, largely following the cue of US Treasuries as the month/quarter got underway.

- Gains faded by mid-afternoon in Europe, with US data releases showing firmer-than-expected job openings, and still-elevated manufacturing sector prices.

- The German curve bull flattened on the day, with the UK's twist flattening. Periphery/semi-core EGB spreads widened slightly, with Greece underperforming.

- In data, Spanish PMI beat expectations but Italy missed. Eurozone June flash inflation metrics came in line with consensus though ECB 1-year and 3-year ahead inflation expectations both eased.

- BoE's Bailey reiterated that the direction of rates continues to be downwards, while ECB's Lagarde repeated that there was no commitment to any particular rate path.

- Wednesday's calendar includes labor market data for Italy, Spain and the Eurozone, and commentary from dovish BoE dissenter Taylor.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.2bps at 1.849%, 5-Yr is down 2.2bps at 2.148%, 10-Yr is down 3.3bps at 2.574%, and 30-Yr is down 4.7bps at 3.053%.

- UK: The 2-Yr yield is up 1bps at 3.827%, 5-Yr is down 1.4bps at 3.936%, 10-Yr is down 3.5bps at 4.454%, and 30-Yr is down 5bps at 5.229%.

- Italian BTP spread up 0.6bps at 87.5bps / Greek up 2.1bps at 71.1bps

MNI OPTIONS: Mixed Rates Trade And Euribor Call Rolling Continues

Tuesday's Europe rates/bond options flow included:

- RXV5 126.50/125.0/125.00p fly, bought for 12 in 2k

- ERZ5 98.25c vs 2RZ5 98.00c, bought the 2yr for 1 in 10k. also bought Yesterday in 15k

- ERM6 97.75p, bought for 4.25 in 6k total

- ERU6 98.68/98.87cs x4.5 vs ERU6 98.25p x0.5, bought the cs for flat in 36k x 4k

- 0RQ5 98.125/98.1875/98.25/98.3125c condor, bought for 1.75 in 3k

- SFIU5 96.20/96.30/96.40/96.50 call condor, paper pays 2 for 8k

- SFIZ5 96.20/96.30cs, sold at 7 in 8k

- SFRZ5 96.25/96.00 1x2 put spread 2K given at 3.25

MNI FOREX: USD Index Recovers From Trendline Support, US Yields Reverse

- It was a tale of two halves for the greenback on Tuesday as an initial extension of recent weakness USD index weakness to fresh cycle lows saw a solid recovery across the US session. Two key factors were at play here; the reversal higher for US yields from bearish extremes which was assisted by some stronger-than-expected US data and an important technical support holding for the DXY, a trendline drawn across the 2011 and 2021 lows.

- This dynamic prompted most G10 peers to erase early gains and slip into negative territory ahead of the APAC crossover. The Canadian dollar stands out here as an underperformer, falling 0.35% against the greenback. The likes of EURUSD and GBPUSD sit around 50 pips off their respective cycle highs.

- For EURUSD, it is worth flagging some interesting comments from ECB Vice President Luis de Guindos who told Bloomberg that the speed of the euro’s ascent is more worrying than its current level. Furthermore, De Guindos expressed the view that levels above 1.20 would provide a more complicated scenario. This may have helped EURUSD consolidate back below 1.18 today, while appetite for fresh EURUSD positions may be contained by the close proximity to this Thursday's US employment print.

- Yen volatility was notable, with an impressive 142.68-144.08 daily range. While dollar/rate dynamics were a primary driver of the day’s moves, it is worth noting the Q2 Japan Tankan survey painted a resilient picture and improved capex outlook, potentially providing an additional yen tailwind. As such, USDJPY remains 0.26% lower on the session despite the greenback turnaround.

- Wednesday’s data calendar is highlighted by Australian retail sales, Eurozone unemployment releases and US ADP. The focus then turns to US NFP and ISM Services data on Thursday, ahead of the July 04 holiday.

MNI OPTIONS: Expiries for Jul02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.0bln), $1.1650(E1.4bln), $1.1675(E1.2bln), $1.1700(E2.1bln), $1.1725-30(E1.1bln), $1.1775(E1.0bln), $1.1785-00(E3.0bln), $1.1900(E1.1bln);

- USD/JPY: Y143.00($555mln), Y143.99-00($648mln), Y144.75($699mln)

- USD/CAD: C$1.3800($1.2bln)

MNI US STOCKS: Late Equities Roundup: Still Mixed, Off Lows After Budget Bill Passes

- Stocks remain mixed in late Tuesday trade, the Dow continues to outperform weaker Nasdaq stocks while SPX eminis see-saw around steady. Currently, the DJIA trades up 426.94 points (+0.97%) at 44521.18, S&P E-Minis down 0.5 points (-0.12%) at 6253.25, Nasdaq down 127.80 points (-0.6%) at 20241.96.

- Trade negotiation headlines took a backseat to the Senate's US budget bill vote that needs a simple majority of 50 votes to pass, rather than the 60 required to pass under regular Senate order. In the case of a 50-50 vote, Vice President JD Vance would cast the tie-breaking vote.

- Stocks drifted higher after the Senate narrowly passed the budget bill which now goes to the House where GOP leaders want to see a final vote tomorrow, allowing Congress to send the completed bill to President Trump's desk on July 4.

- Materials, Health Care and Retail sectors led gainers in the second half with a fair amount of discretionary stocks as well: Builders FirstSource +9.44%, Las Vegas Sands +8.83%, Wynn Resorts +8.64%, Packaging Corp of America +7.44%, MGM Resorts International +7.21%, Smurfit WestRock PL +6.00%, Target Corp +5.62%, Hershey Co +5.49% and Best Buy Co +5.35%.

- Technology and energy related shares continued to underperform in late trade, the latter under pressure as an amendment to the budget bill struck down state-level bans on AI regulation: Palantir Technologies -4.60%, Broadcom -3.58%, Advanced Micro Devices -3.22%, Arista Networks -3.11% and Nvidia -2.11%. Perhaps ironically, energy stocks were under pressure for the same reasons as high speed chips use a lot of energy: Williams Cos -5.68%, GE Vernova -5.22%, Expand Energy -4.16% and Vistra -3.85%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Approaching The Bull Trigger

- RES 4: 6300.00 Round number resistance

- RES 3: 6281.12 1.618 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6277.50 High Feb 19 and a bull trigger

- RES 1: 6265.50 High Jun 30

- PRICE: 6257.00 @ 1445 ET Jul 2

- SUP 1: 6087.08/5964.66 20- and 50-day EMA values

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has started this week on a firm note. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has recently been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared too, this opens 6277.50, the Feb 21 high and bull trigger. Key support is at the 50-day EMA - at 5964.66.

MNI COMMODITIES: Gold Recovers From Monday’s Low, WTI Rises

- Spot gold has rallied by 1.1% today to $3,338/oz, leaving the yellow metal 2.8% above yesterday's $3,248.7 low.

- Mounting fiscal concerns in the US as the Senate passed President Trump’s tax bill may be providing some support to gold, which has also benefitted from the further decline in the dollar so far this week.

- The recovery in gold highlights a possible false trendline break, after spot pushed through the 50-day EMA and trendline support drawn from the December 30 low last Friday.

- Spot has pierced initial resistance at $3,336.3, the 20-day EMA today, exposing the June 23 high at $3,395.1. Stronger gains would refocus attention on $3,451.3, the June 16 high.

- Meanwhile, crude is on track for slight gains on the day, with the market weighing stronger seasonal demand and improved global economic outlooks ahead of expected US trade deals, against expectations of another large OPEC+ output hike in August.

- WTI Aug 25 is up by 0.5% at $65.4/bbl.

- Oil traders expect OPEC+ will agree a fourth bumper oil supply increase on July 6, Bloomberg reports.

- For WTI futures, support to watch is at the 50-day EMA, at $64.64, which has been pierced. A clear break of it would signal scope for a deeper retracement, exposing $58.87, the May 30 low.

- On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 02/07/2025 | 0800/1000 | ECB de Guindos Chairs Sintra Panel | ||

| 02/07/2025 | 0900/1100 | ** | Unemployment | |

| 02/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/07/2025 | 0900/1100 | ECB Cipollone Chairs Sintra Panel | ||

| 02/07/2025 | 1030/1230 | ECB Lane Chairs Sintra Panel | ||

| 02/07/2025 | 1030/1130 | BOE Taylor On Panel At Sintra Conference | ||

| 02/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 02/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 02/07/2025 | 1415/1615 | ECB Lagarde Gives Closing Sintra Remarks | ||

| 02/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/07/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/07/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/07/2025 | 0130/1130 | ** | Trade Balance | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |