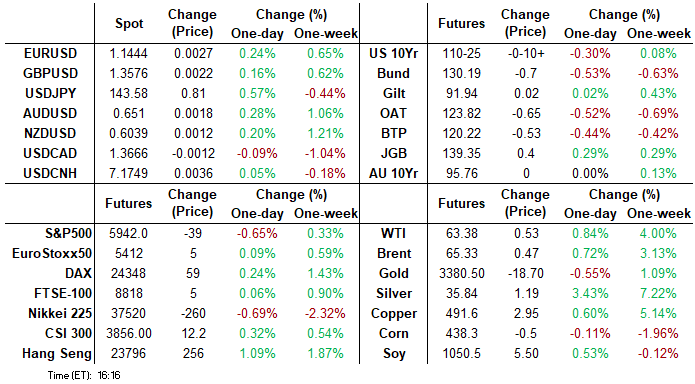

MNI ASIA MARKETS ANALYSIS: Trade Talk Touted, No Breakthroughs

HIGHLIGHHTS

- Rocky start to finish for Treasuries Thursday, well off early knee-jerk highs to extending lows in late trade as investors react to Trump/Xi trade headlines touted progress with no major breakthroughs.

- Treasuries ratcheted lower after higher weekly claims & labor costs, several Fed speakers after the ECB cut rates by 25bp.

- Stocks sink after Trump/Musk spat really heats up after the bell, Pres Trump musing about ending Musk's government contracts while Musk responds with claim that Trump is in the Epstein files.

- Projected rate cut pricing consolidated vs. early morning levels, December still pricing in just over 50bp, focus turns to Friday's headline employment report for May.

US TSYS

MNI US TSYS: Headline Risk Rattles Markets Ahead of Friday's Headline Jobs Report

- After gapping higher early Thursday, Treasuries look to finish at/near late session lows as markets try to absorb a raft of trade-related headline risk, higher weekly claims & labor costs, several Fed speakers and the ECB's 25bp rate cut decision earlier.

- Treasury futures extend gains briefly then pared move after higher than expected weekly claims while continuing claims come out a little lower than expected, prior down-revised; unit labor costs higher than expected. Rates continued to pare gains as details of Pres Trump/Xi phone call emerge - less optimistic regarding trade than when the headline first aired.

- Initial jobless claims unexpectedly rose in the week of May 31, rising to 247k (235k expected) from 239k (rev from 240k) prior. Continuing claims meanwhile went in the opposite direction, ticking lower in the May 24 week to 1,904k. Unit labor costs (ULCs) were revised substantially higher in the Bureau of Labor Statistic's Q1 final release, rising 6.6% Q/Q SAAR (rev from 5.7% prelim, and up from 3.8% prior).

- Meanwhile, ahead of Friday's headline jobs report for May, the Challenger Gray report for May saw 93.8k job cut announcements, after 105k in Apr, 275k in Mar (of which 217k was govt) and 172k in Feb.

- Note, late headline risk saw stocks tumble after the bell as Trump/Musk spat really heats up after the bell, Pres Trump musing about ending Musk's government contracts while Musk responds with claim that Trump is in the Epstein files.

- The U.S. Treasury on Thursday added Ireland and Switzerland to its currency manipulator watch list, and officials warned continued strengthening of global currencies relative to the dollar could see more foreign exchange market interventions and rising current account surpluses that would land more countries on the list.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (-0.04), volume: $2.625T

- Broad General Collateral Rate (BGCR): 4.27% (-0.03), volume: $1.060T

- Tri-Party General Collateral Rate (TCR): 4.27% (-0.03), volume: $1.033T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $294B

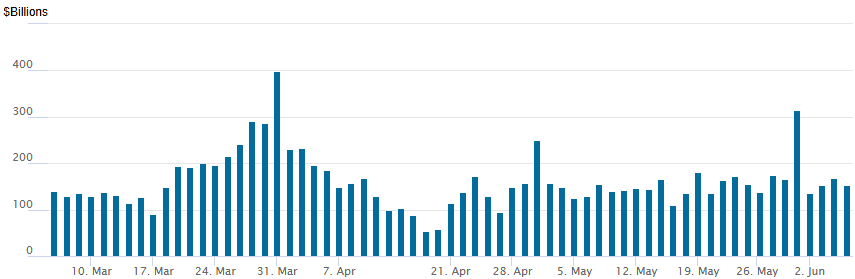

FED Reverse Repo Operation

RRP usage retreats to $152.727B this afternoon from $168.882B yesterday, total number of counterparties at 29. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury options saw better call unwinds and vol structure sales Thursday. After rising to 4W highs this morning, underlying futures reversed course midmorning - extending lows after midday as markets digested latest headlines over US/China trade. Curves twist flatter while projected rate cut pricing consolidates vs. morning levels (*) as follows: Jun'25 at -0.7bp (-0.2bp), Jul'25 at -7.9bp (-7.55bp), Sep'25 at -23.2bp (-24.9bp), Oct'25 at -36.9bp (-40bp), Dec'25 at -53bp (-57.5bp).

SOFR Options:

+2,000 SFRZ5 96.00/96.25/96.37 broken call flys, 3.75 ref 95.94

-2,500 SFRZ5 96.00 puts, 14.0 vs. 96.22/0.34%

+3,000 SFRV5 95.87 puts, 5.5 ref 96.255

-3,000 SFRN5 96.00/0QN5 96.75 straddle strips, 54.5-54.0

-16,000 SFRU5 96.25/96.50 call spds, 3.0 ref 95.97

-10,000 SFRZ5 97.00/97.50 call spds, 4.5 ref 96.28

-4,000 SFRU5 95.75/95.81/96.00 put flys 2.5 over 95.68/95.81 put spds

-40,000 0QN5 97.00/97.25 call spds, 4.25 ref 96.765

Block, 5,000 0QN5 96.87/97.25/97.62 call flys, 5.5

4,000 SFRN5 95.62/95.75/95.87 put flys ref 95.955

-2,350 0QM5 96.81/97.06 2x1 put spds, 0.5 vs. 96.63/0.62%

2,800 0QM5 96.75/97.00 call spds ref 96.625

Block, +4,000 2QU5 96.87/97.25/97.50 broken call flys, 6.0 ref 96.665

Block, -3,500 SFRM5 95.68/95.75/95.81 put flys, 0.75 ref 95.6925

+2,000 SFRM5 95.68/95.75 1x2 call spds, 0.5

2,000 0QU5 95.62/2QU5 95.50 put spds, 0.0 net short Sep over

Treasury Options:

-5,000 TYU5 111 straddles 239-238 ref 110-25

-9,700 TYQ5 109/112.5 strangles, 51 ref 110-25

+4,000 TYQ5 110 puts, 36 ref 110-28

-4,500 TYN5 111.25 straddles, 109 ref 111-03

4,000 TYN5 111.25/111.75 call spds 11 ref 111-05

16,200 wk1 FV 108.5/108.75/109.0/109.25 call condors (exp Fri)

5,000 TYU5 107/108 put spds, 8 ref 111-08.5

4,500 Wed wkly FV 108/108.25 2x1 put spds ref 108-14.5 to -15.5

+5,000 Mon wkly TY 112 calls, 5

3.500 TYN5 111/111.75 call spds vs. wk1 TY 111.25 calls ref 111-07.5

+1,000 TYN5 110/111 1x2 call spds 0.0

+5,000 wk1 FV 107.5 puts, 0.5

+3,000 TYN5 107.5 puts, 1

3,000 wk1 TY 111.25/111.5 call spds, 4 (exp Fri)

+3,000 TYN5 109.5 puts, 7

Block, +20,000 TYQ5 108.5/109.5 put spds 13 ref 111-03.5

MNI BONDS: EGBs-GILTS CASH CLOSE: ECB Bear Flattens Bund Curve

European yields rose sharply Thursday, with the ECB signalling that rate cuts are on hiatus.

- While the ECB cut rates 25bp as widely expected, the tone of communications was perceived hawkishly.

- The decision statement was non-committal on future moves, and Pres Lagarde provided multiple hints that the Governing Council was as she said "getting to the end of a monetary policy cycle".

- A Bloomberg post-meeting sources piece pointed to consensus among policymakers for a pause in July, and markets eye no more than one more cut the rest of the year (December).

- Adding bearish fuel to the bond fire was an apparent rapprochement between US's Trump and China's Xi.

- The German curve bear flattened, with the UK's belly underperforming.

- Periphery EGB spreads fell, with 10Y BTP/Bund closing at the tightest levels in 4 years.

- Friday's calendar includes German industrial production (after today's factory orders) and trade data, and French IP/manufacturing, as well as the final reads of Eurozone GDP and Employment in Q1, alongside several ECB speakers including Lagarde and Holzmann.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 7.5bps at 1.873%, 5-Yr is up 7.3bps at 2.171%, 10-Yr is up 5.4bps at 2.582%, and 30-Yr is up 2.6bps at 3.025%.

- UK: The 2-Yr yield is up 0.2bps at 4.007%, 5-Yr is up 1.1bps at 4.126%, 10-Yr is up 1bps at 4.616%, and 30-Yr is up 0.3bps at 5.325%.

- Italian BTP spread down 2bps at 94.4bps / French up 0.6bps at 67.9bps

MNI EGB OPTIONS: Large Euribor Profit Taking And Upside Post-ECB

Thursday's Europe rates/bond options flow included:

- ERM5 97.9375/98.0625cs, sold at 7.5 in 47k (profit taking).

- ERH6 97.87/98.37/98.87 call fly bought for 21.5 in 40k

- SFIM6 96.80/96.90cs, bought for 2.75 in 25k (6k was done vs 96.38.5 and 19k vs 96.38).

MNI FOREX: EUR Boosted by Hawkish ECB Presser, JPY Underperforms

- The Japanese yen has underperformed on Thursday, prompting USDJPY to consolidate back above 143.50, having recovered healthily from the overnight 142.53 lows. Contributing to the recovery was cautious optimism surrounding progress between US/China talks, which initially had boosted major equity benchmarks.

- However, late headlines surrounding the Trump/Musk feud and potential sanctions on Russia & Ukraine dented overall sentiment. This had less of an impact on USDJPY, with higher front-end US yields providing support.

- In contrast to the yen’s underperformance, the Euro is higher on the day following President Lagarde giving a clearly more hawkish/congratulatory tone in the press conference, noting policy is well positioned and that “we are getting to the end of a monetary policy cycle that was responding to compounded shocks.” EURUSD printed a high of 1.1495 on the session, keeping bullish conditions firmly intact, and signalling scope for a move to cycle highs at 1.1573.

- EURJPY is 0.8% higher as we approach the APAC crossover and sights remain on a cluster of resistance around the 165.00 mark, a level of pivotal significance dating back to the BOJ’s intervention back in July last year. 165.21, the May 13 high remains the technical bull trigger, of which a breach would target a move towards 166.10, the Nov 6 high.

- Elsewhere, USDCAD temporarily breached support – trading below 1.3643 for the first time since early October last year. Below here, attention will be on 1.3579, the 1.5 Fibonacci projection of the Feb 3 - 14 - Mar 4 price swing, before the September lows at 1.3420 will garner attention.

- The USD index is unchanged as we approach tomorrow’s US employment report for May, where Canadian jobs figures will also be published.

MNI FX OPTIONS: Expiries for Jun06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E1.0bln), $1.1350(E656mln), $1.1400(E1.bln), $1.1450(E847mln), $1.1500(E1.4bln), $1.1550(E500mln)

- USD/JPY: Y142.00($1.6bln), Y142.50-60($744mln), Y142.90-05($684mln), Y143.50-65($584mln)

- EUR/GBP: Gbp0.8420-30(E510mln)

- GBP/USD: $1.3410(Gbp897mln)

- AUD/USD: $0.6300(A$1.5bln)

- USD/CAD: C$1.3600($626mln), C$1.3660($500mln), C$1.3745-60($1.1bln), C$1.4035-40($1.2bln), C$1.4180-85($1.6bln)

MNI US STOCKS: Late Equities Roundup: Jack Daniels & Tesla Underperforming

- Stocks sink after Trump/Musk spat really heats up after the bell, Pres Trump musing about ending Musk's government contracts while Musk responds with claim that Trump is in the Epstein files. DJIA currently down 207.89 points (-0.49%) at 42455.75, S&P E-Minis down 48.75 points (-0.82%) at 5968, Nasdaq down 225.3 points (-1.2%) at 19384.45.

- S&P eminis had gapped higher after Chinese state media Xinhua confirmed that Presidents Xi & Trump have held phone talks early this morning. Earlier this week Politico reported that Trump saw a call with Xi as key to breaking a deadlock in trade negotiations. Stocks pared gains following this morning's economic data while details over the Trump/Xi lacked any major breakthroughs.

- Consumer Staples underperformed: Brown-Forman fell -16.96% after Canada & Europe cut back on Jack Daniels imports do to tariffs, global growth concerns. Constellation Brands -3.12% and Costco Wholesale -3.82%. Meanwhile, the Consumer Discretionary sector was weighed by Tesla -11.43% as a Trump and Musk spat spills onto social media platforms, Wynn Resorts -2.57% and LKQ -2.18%.

- Communication Services and Health Care sectors outperformed in the second half, Live Nation Entertainment +3.17%, Match Group +1.77% and TKO Group Holdings +1.59% buoyed on the former. Pharmaceutical stocks supported the Health Care sector in late trade: West Pharmaceutical +3.54%, Medtronic +1.72% and Gilead Sciences +1.71%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Trend Needle Points North

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6008.00 High May 29

- PRICE: 5939.00 @ 1528 ET Jun 5

- SUP 1: 5863.16/5774.07 20- and 50-day EMA values

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has traded to a fresh cycle high, today. The break of 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5774.07, the 50-day EMA.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 06/06/2025 | 0600/0800 | ** | Trade Balance | |

| 06/06/2025 | 0600/0800 | ** | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Foreign Trade | |

| 06/06/2025 | 0830/1030 | ECB Lagarde Video Message For CIBP Anniv | ||

| 06/06/2025 | 0900/1100 | ** | Retail Sales | |

| 06/06/2025 | 0900/1100 | *** | GDP (final) | |

| 06/06/2025 | 0900/1100 | * | Employment | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1900/1500 | * | Consumer Credit |