CHINA: MLF Rates Lower on New Pricing Structure, Not Policy Shift

- The Medium-term Lending Facility (MLF) is a monetary policy tool used by the PBoC to manage liquidity in the banking system and influence medium-term interest rates.

- The MLF has transitioned to a more market-driven, bidding mechanism, rather than the PBoC setting a single uniform interest rate. Under this "multiple-price auction" system introduced in March 2025, participating banks bid at different rates for a set amount of funds.

- This has seen PBOC charging some lenders as low as 1.5% in January, down from the last official rate of 2% early in 2025, before the PBOC stopped publishing the figure.

- The MLF provides collateralized loans to commercial and policy banks to ensure they have stable funding for periods from 3 to 12 months and is primarily viewed as a backstop to manage maturity mismatches between lending and deposits. Operations are monthly and supplement daily OMO, with an injection of CNY700bn in January.

- A more market focused approach is aimed at lowering the cost the MLF, as the PBoC encourages banks to lower interest rates for small and medium enterprises.

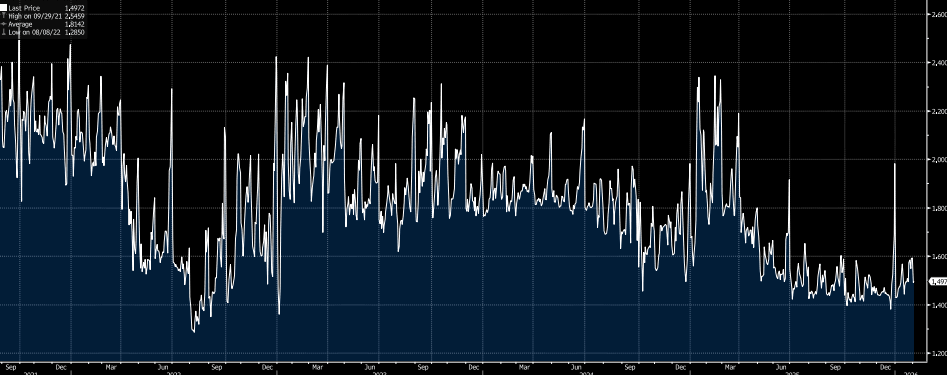

- DR007 is the best gauge for interbank lending liquidity and the central bank's actual monetary stance. The PBoC uses this rate to manage the "interest rate corridor," making it a lead indicator for where the LPR might move in the future. Currently it is at 1.59%

- We expect less of headline policy moves in the first part of the year in China, more incremental moves like this to support the broader economy.

Fig 1: DR007 - 1-Yr Decline Since Moving to More Market Based Approach

source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Eyes on Bond's Reactions to Geopolitical Moves

US bond futures across all maturities finished down Friday. The US 10-Yr finished down -07+ at 112-06+. It is wedged between the upside resistance from the 100-day EMA of 112-14+ and the downside resistance from the 200-day EMA of 112. TYH6 has opened the trading day in Asia at 112-06+ with limited activity early on.

Venezuela and Geopolitics will be a key influence for general market sentiment and the bond market will watch closely for the equity open. Equity futures in Asia are generally positive at this stage.

- The 2-Yr finished last seek at 3.47%, down -0.5bps for the week.

- The 5-yr finished last week at 3.74%, up +5bps for the week.

- The 10-Yr finished last week at 4.192%, up +6.3bps for the week.

- The 30-Yr finished last week at 4.871%, up +5.6bps for the week.

Whilst January is typically a busy month for issuance, Monday kicks off with just a US$86bn 13-week bill auction and a US$77bn 26-week bill auction.

Data wise ISM releases are the focus with the ISM Manufacturing forecast to remain in contraction and ISM Prices paid to remain elevated.

CHINA: Weekly Preview: PPI and CPI Key, Equity Valuations Looking Stretched

Download Weekly Preview Here:

- The key data releases are the PPI and CPI which have been mired in or near to deflation for some time. Whilst PPI has remained in deflation since 2022, CPI has inched back positive in November and will be keenly watched this week.

- The CSI 300 ended the week with modest gains and in early January is at 5-Year highs for Price to Earnings. At 17.52x, it remains significantly above the 2026 forecast of 14.40x, suggesting downside risks could build. The dividend yield finished 2025 at 2.36% to remain a supportive factor from a valuation perspective, relative to bond yields.

- Despite this, investor sentiment remains in a weakening trend with the property sector woes continuing to weigh heavy.

- USD/CNH consolidated its late 2025 break under 7.00, tracking near 6.9700 in latest dealings. The pair saw little upside through the tail end of last year, despite broader USD indices recovering some ground.

JGBS: Trading To Resume After Extended NY Break

In post-Tokyo trade on NYE, JGB futures closed stronger, +8 compared to settlement levels.

- On Friday, after US tsys finished Friday with a modest bear-steepener.

- There was limited data on Friday: The final December S&P Global Manufacturing PMI was unchanged from the flash reading of 51.8, confirming a 5-month low for the index (52.2 Nov). In turn, the details of the report confirmed the flash data in portraying a broad-based softening amid overall growth in manufacturing.

- Japan markets return today after an extended new year break from late last week. The local data calendar just has the final Dec PMI manufacturing read (via S&P Global) out today.

- Most focus this week is likely to rest on Thursday Nov labour earnings data. Real earnings are forecast to remain negative y/y (-1.3% forecast, versus -0.7% prior). On Friday Nov household spending prints.

- From late last week, Japan PM Takaichi said that she plans to visit the US in spring after a successful phone call with the US President Trump.

- Headlines also crossed earlier that North Korea has test fired a hypersonic missile, but broader risk appetite has been unmoved.

Source: Bloomberg Finance LP