US NATGAS: Midwest Natgas Fundamentals - Apr 21st

MNI Take: Chicago CG rose 8 cent yesterday. Chicago weather forecasts continue to call for warmer than normal weather for the next week, providing minimal support for incremental heating demand. Demand weakened further today, reaching 10.4 Bcf/d, which is 0.9 Bcf/d below last year’s levels. Warm weather and weak demand is encouraging fewer net inflows from Eastern Canada, suggesting higher storage injections are on the horizon. Lower demand is being offset by lower inflows from Appalachia, the Bakken, and the MidCon leaving the region balanced to slightly short today.

- Chicago week ahead weather forecasts are calling for warmer-than-normal weather. Chicago cumulative HDDs increased by 1.76 compared with the prior forecast.

- Chicago cumulative HDDs count for the next 5 days is 22.07, down 45.1 days from the 10-year normal, while the count for the next 14 days is 133.81, down 46.61 days from the 10-year normal.

- MidWest demand is 10.4 Bcf/d today, down 1.06 Bcf/d from yesterday and up 0.3 Bcf/d from last week.

- Net imports from Eastern Canada are 1.1 Bcf/d today, down 0.14 Bcf/d from yesterday and down 0.05 Bcf/d from last week.

- Imports from Western Canada are 1.8 Bcf/d today, down 0.35 Bcf/d from yesterday and down 0.1 Bcf/d from last week.

- Appalachian inflows are 6.6 Bcf/d today, down 0.36 Bcf/d from yesterday and down 0.45 Bcf/d from last week.

- Bakken net inflows are 3.9 Bcf/d today, down 0.07 Bcf/d from yesterday and down 0.25 Bcf/d from last week.

- MidCon net inflows are 2.2 Bcf/d today, down 0.46 Bcf/d from yesterday and down 0.47 Bcf/d from last week.

- TVA exports are 2.3 Bcf/d today, down 0.14 Bcf/d from yesterday and up 0.11 Bcf/d from last week.

- Note: MidWest region includes IL, IN, IA, MI, MN, WI

- All fundamentals data is BNEF. Current figures as of publishing.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Key Resistance Remains Intact For Now

- RES 4: 1.3845 High Jan 22

- RES 3: 1.3800 High Jan 23

- RES 2: 1.3753 High Mar 03 and key resistance

- RES 1: 1.3748 High Mar 19

- PRICE: 1.3714 @ 17:00 GMT Mar 20

- SUP 1: 1.3670/3526 20-day EMA / Low Mar 09

- SUP 2: 1.3482 Low Jan 30 and the bear trigger

- SUP 3: 1.3420 Low Sep 25 ‘24

- SUP 4: 1.3400 50.0% retracement of the 2021 - 2025 uptrend

Attention in USDCAD is on key near-term resistance and a bull trigger at 1.3753, the Mar 3 high. A clear break of this hurdle would confirm a range breakout, highlight a stronger bull cycle and confirm a clear breach of the 20- and 50-day EMAs. This would open 1.3800 initially, the Jan 23 high. For bears, a reversal would refocus attention on 1.3482, the Jan 30 low and bear trigger.

AUDUSD TECHS: Trend Needle Points North

- RES 4: 0.7284 High Jun’22

- RES 3: 0.7256 2.500 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 2: 0.7208 61.8% of the Feb 25 ‘21 - Apr 9 ‘25 bear leg

- RES 1: 0.7187 High Mar 11 and the bull trigger

- PRICE: 0.7039 @ 16:59 GMT Mar 20

- SUP 1: 0.6979 50-day EMA and key support

- SUP 2: 0.6944 Low Mar 3

- SUP 3: 0.6897 Low Feb 6

- SUP 4: 0.6834 Low Jan 23

The trend condition in AUDUSD is unchanged, it remains bullish and the pair continues to trade above key support at 0.6979, the 50-day EMA. A clear break of this average would undermine the current bullish theme. The moving average set-up is in a bull mode position and this continues to highlight a dominant medium-term uptrend. A resumption of the trend would open 0.7208 next, a Fibonacci retracement point.

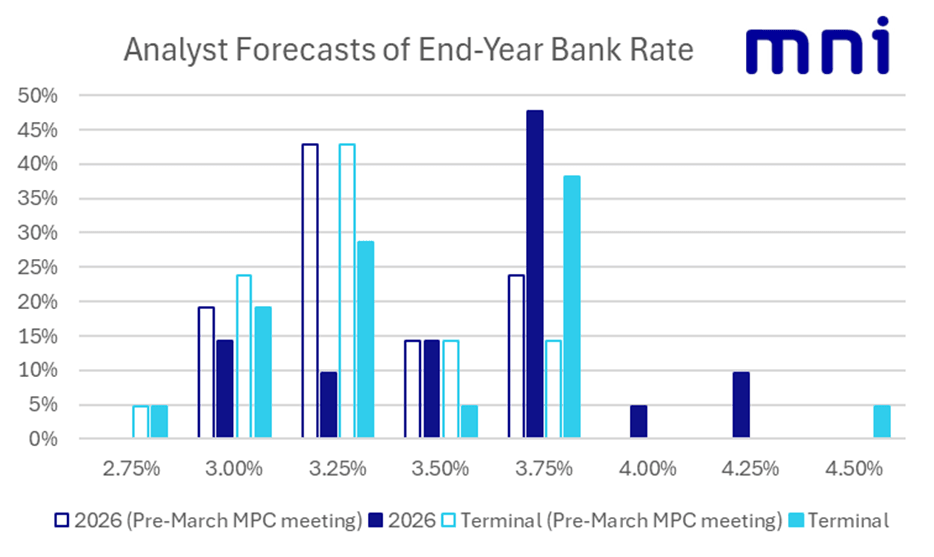

BOE: Summary of Analyst Views

- Just over half (11/21) of the analyst reviews that we have read still look for the next move from the MPC to be a cut. 4/21 look for a hike while 6/21 look for the Bank to remain on hold for their forecast horizon.

- In terms of those expecting hikes Daiwa, JP Morgan and Rabobank all look for the first hike in April with the former two looking for a 4.25% peak and Rabobank looking for a one-and-done. NatWest Markets look for the first hike in Q4-26 but then expect two further hikes in Spring 2027 to the highest peak of 4.50% seen in any analyst base case that we have seen.

- Note that of these analysts, 3/4 (all except NatWest Markets) expect cuts back to a least current levels within their forecast horizon.

- In terms of those looking for the next move to be a cut, none look for a move in April with 5 analysts expecting a June cut, 1 for July, 2 for November and the remaining 3 looking for cuts to begin in 2027.

- UniCredit has the lowest terminal rate, continuing to look for 2.75% while 4/21 analysts look for 3.00% terminal, 6/21 analysts look for 3.25% and 1/21 analyst looks for 3.50%. As noted above, NatWest Markets looks for hikes with no reversal but the remaining 8/21 analysts look for no moves from 3.75% throughout the forecast horizon.