MEXICO: Goldman Sachs Believe Latest Data Supports Gradual Banxico Easing

Aug-22 14:32

- According to Goldman Sachs, the early August inflation release supports the continuation of a gradual monetary policy rate normalization cycle.

- Overall, core-goods inflation remains low and shows no visible signs of MXN weakness pass-through. Services inflation remains high and sticky but is now showing early signs of moderation.

- The acceleration of headline inflation during 2Q24 and 1H Jul was driven by a major shock to non-core perishable food and rising energy prices which drove non-core inflation to a high 10.64% yoy by 1H Jul.

- The large perishable food price shock has now started to mean-revert, a process that GS expect will continue through the end of the year. In the meantime, we will be looking for potential second-round effects of core inflation components.

- Finally, the recent decline in oil prices should also help to ease non-core price pressures, though renewed MXN depreciation pressure may neutralize that effect.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: MNI INTERVIEW: Fed To Open Door To Sept Cut Next Week

Jul-23 14:29

Former Secretary to the FOMC speaks to MNI about the Fed's next meeting.-- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

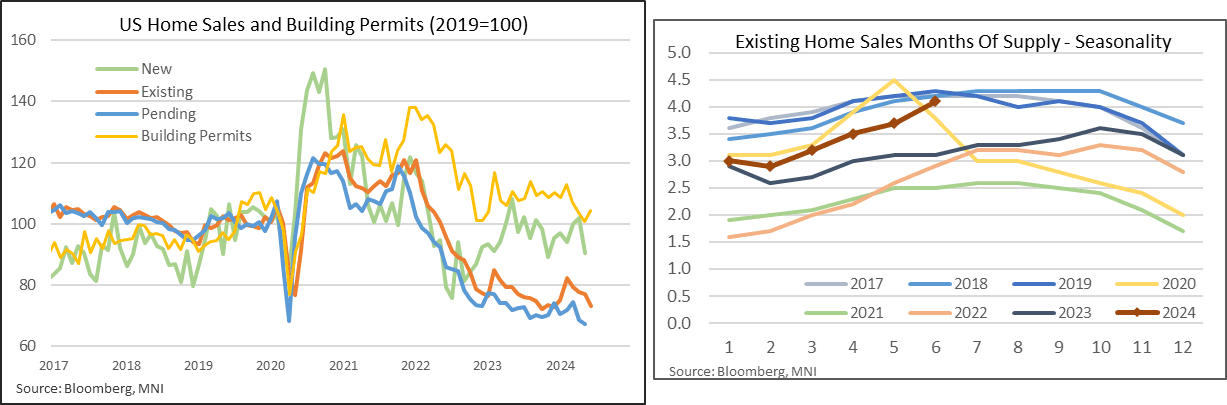

US DATA: Existing Home Sales Disappoint Whilst Relative Supply Is Back At Pre-Pandemic Levels

Jul-23 14:15

- Existing home sales were weaker than expected in June at 3.89m (cons 3.99m) after an unrevised 4.11m in May.

- It sees sales fall -5.4% M/M and a fourth consecutive monthly decline worth a cumulative -11% which has more than offset the 9.5% jump back in Feb.

- The trend better reflects the continued weakness seen in pending home sales which hit a new series low in May for data going back to 2001.

- Latest existing home sale declines were relatively broad-based, ranging from -2% (northeast) to -8% (midwest) and with the largest region, the south, falling -6%.

- A further uplift in the outright level of inventories meant that the months of supply increased strongly to 4.1 from 3.7 in May.

- This non-seasonally adjusted figure compares with 3.1 in Jun’23 and 2.9 in Jun ’22, and is essentially back to pre-pandemic averages (4.2 average in 2017-19 June readings). That compares with last month’s 3.7 vs a 2017-19 average also of 4.2.

- Impressively considering the further increase in relative supply, median price growth slowed but only from 5.2% to 4.1% Y/Y.

COMMODITIES: Softer Oil, Metals Backdrop Supportive of Core FI

Jul-23 14:11

Crude oil prices are once again under pressure, with front-month Brent and WTI futures each around 1% lower today. Industrial metals are similarly weaker (iron ore -1.8%, copper -1.1%, steel -0.7%).

- These moves will have provided some support to core FI, with the EUR and USD 5y5y inflation swaps around 1.5/2bps lower at typing.

- Our commodities team notes that concern around future global oil demand - especially in China – and the planned return of OPEC+ supply is outweighing the impact of near-term tightness and geopolitical/weather-related supply risks.

- Next support in Brent is seen at $79.32/bbl (76.4% retracement of the Jun 4 - Jul 5 bull leg), while key WTI support is at the June 4 low at $72.23/bbl.