CANADA: March LFS Preview: Analysts See Muted Employment Gains (2/2)

Apr-09 19:06

MNI's median of Canadian bank analysts sees a 15k increase in employment in March, with the unemploy...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Bearish Cycle Extends

Mar-10 19:00

- RES 4: 0.8818 High Nov 26 ‘25

- RES 3: 0.8806 76.4% retracement of the Nov 14 - Feb 4 bear leg

- RES 2: 0.8739/89 High Mar 3 / High Feb 27 and key S/T resistance

- RES 1: 0.8703 50-day EMA

- PRICE: 0.8654 @ 16:22 GMT Mar 10

- SUP 1: 0.8642 Low Feb 5 & Mar 10

- SUP 2: 0.8613 Low Feb 04 and bear trigger

- SUP 3: 0.8597 Low Aug 14

- SUP 4: 0.8578 Low Jul 2 ‘25

A bear cycle in EURGBP remains intact. The reversal lower from the Feb 27 high has resulted in a breach of support at the 50-day EMA. The break highlights a stronger reversal, and the continuation lower exposes 0.8613, the Feb low and bear trigger. Key short-term resistance has been defined at 0.8789, the Feb 27 high, where a break would resume the recent bull leg. The first important resistance is the 50-day EMA at 0.8703.

US PREVIEW: Too Early For Energy Shock To Show In February CPI Report

Mar-10 18:35

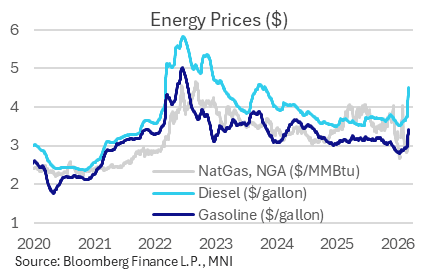

- As noted in the MNI Preview, seasonally adjusted fuel prices are expected to have seen a sequential acceleration in February driving a shift in overall energy price inflation from -1.5% M/M in Jan to perhaps close to 1.0% M/M in Feb.

- Fuel prices increased in non-seasonally adjusted terms through Feb but it paled in comparison to increases seen so far in March following the Middle East conflict stemming from US-Israel strikes on Feb 28.

- AAA retail gas prices increased a non-seasonally adjusted 3.2% M/M in Feb but as of Friday (Mar 6) were another 16% higher than average February levels.

- Diesel prices are more pronounced still, currently another 22.5% higher after a 3.9% average increase in February.

- Natural gas prices meanwhile are currently ~5% higher than average February levels, offsetting a -4.3% decline over the month.

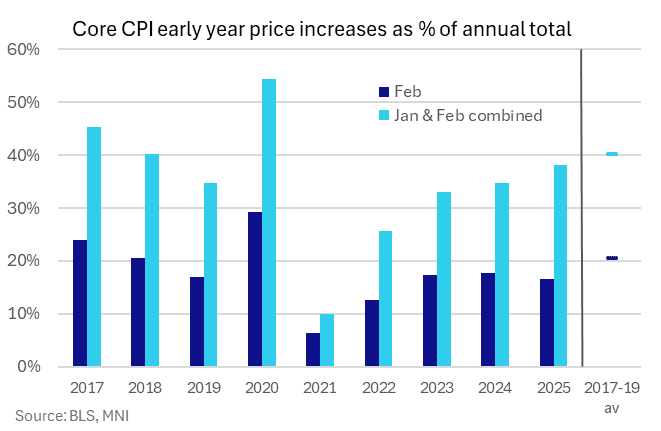

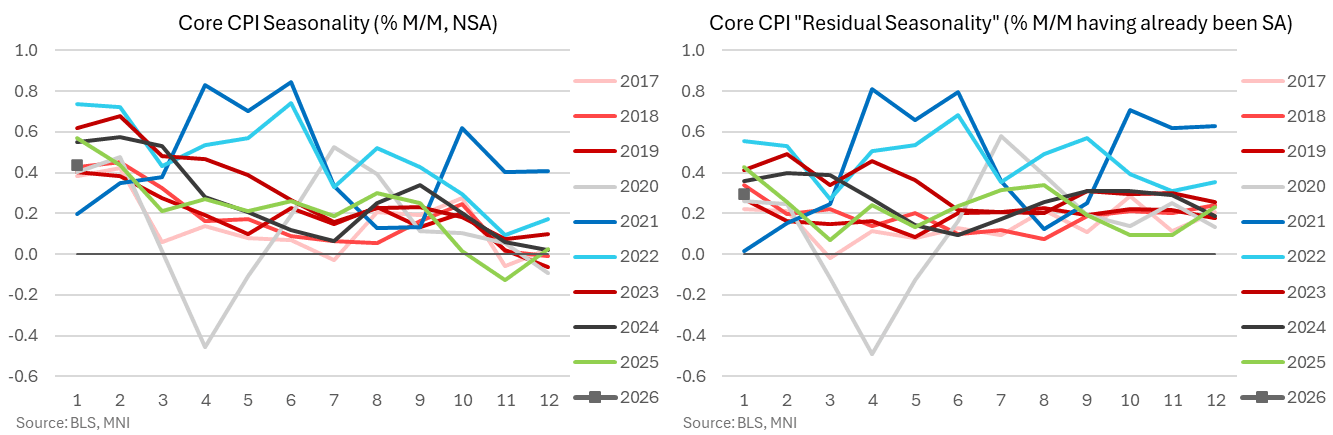

US PREVIEW: Less Of A Case For CPI Residual Seasonality Than In Jan

Mar-10 18:33

- February can still see residual seasonality – biasing seasonally adjusted inflation rates higher – although it tends to be smaller than January effects. Last month’s seasonal adjustment revisions didn’t materially change this on net with core CPI trimmed 2bps in Jan but lifted 3bps in Feb.

- Nevertheless, it’s still a second important month at the start of the year, with the two months having historically (pre-pandemic) accounted for an average 40% of price increases that are seen over the upcoming year.

- That has historically been split broadly equally over January and February although recent February’s have seen slightly less of a return to pre-pandemic trends, with Feb 2025 accounting for 16.5% of 2025 price increases.