ECB: Macro Since Last ECB Decision - Inflation: Non-Universal Firming In Surveys

Jun-10 18:16

PMIs Imply Further Intensification Although To Less Degree Than Input Costs * May final PMI (Jun 3)...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US INFLATION: Watch Semiconductor Shortages (For Core PCE Tracking)

May-11 18:11

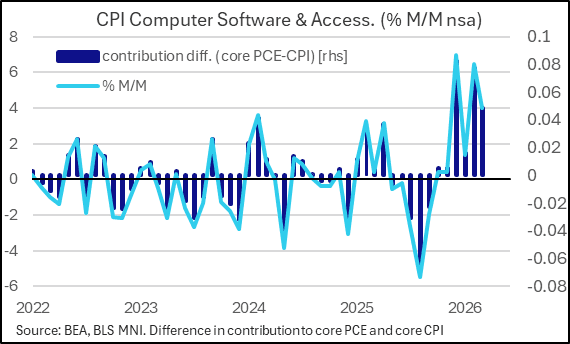

Sticking with core goods, there is one small category that should be watched even if it doesn’t get a spot in the summary table in the MNI US CPI Preview (link).

- Computer software & accessories saw two particularly strong months with 4.0% M/M in March after 6.5% M/M in February and is qualitatively expected to have been firm again in April.

- JPMorgan write that we “could see another firm increase. The index includes SD and USB memory devices, whose prices have been surging because of AI-related increases in memory prices. Prices for some of the best-selling products in this category on Amazon saw further price increases in April.”

- Recall that this is very much a core PCE rather than core CPI story, helping widen the wedge between the two, with weights of 1.2% vs 0.04% respectively. As such, it added 0.05pps to core PCE in March after 0.08pp in Feb compared to essentially zero to core CPI.

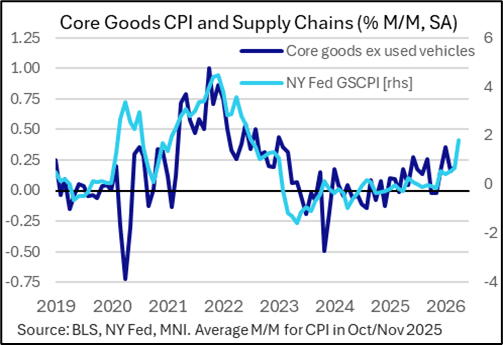

US INFLATION: Supply Chain Pressures Increased More Acutely In April

May-11 18:09

- Away from the direct impacts from markedly higher energy prices, core goods items more broadly could see upward pressure from another intensification in supply chain pressures.

- The NY Fed’s GSCPI saw a marked increase in April to 1.8 standard deviations above its historical average for its highest since mid-2022.

- This index first stepped higher in December to 0.55 and happened to be followed by our estimate of median core goods inflation accelerating to 0.44% M/M (matching the Jun 2025 high for the post-tariff period) before monthly inflation moderated notably as the index levelled off at that level through Q1.

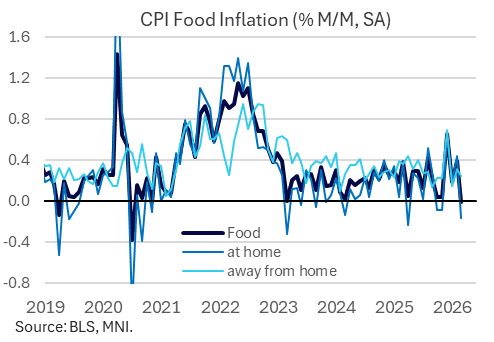

US INFLATION: CPI Food Prices Seen Bouncing Back After Rare Drop

May-11 18:07

- Food inflation is expected to have returned to a more typical 0.3% M/M after an unusually soft March at -0.01% M/M when food at home fell -0.16% M/M. This category should give an idea of passthrough from higher transportation and fertilizer costs.

- Food away from home held at a somewhat solid 0.24% M/M in March after three particularly strong months averaging 0.39% M/M through Dec-Feb. This services-related category could give an indication of discretionary demand in the face of the sharp rise in travel costs.

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank