JGB TECHS: (M6) Holds Above Fresh Lows

* RES 3: 133.15 - High Feb 24 '26 * RES 2: 131.85 - 50-dma (cont) * RES 1: 131.80 - 38.2% retracemen...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

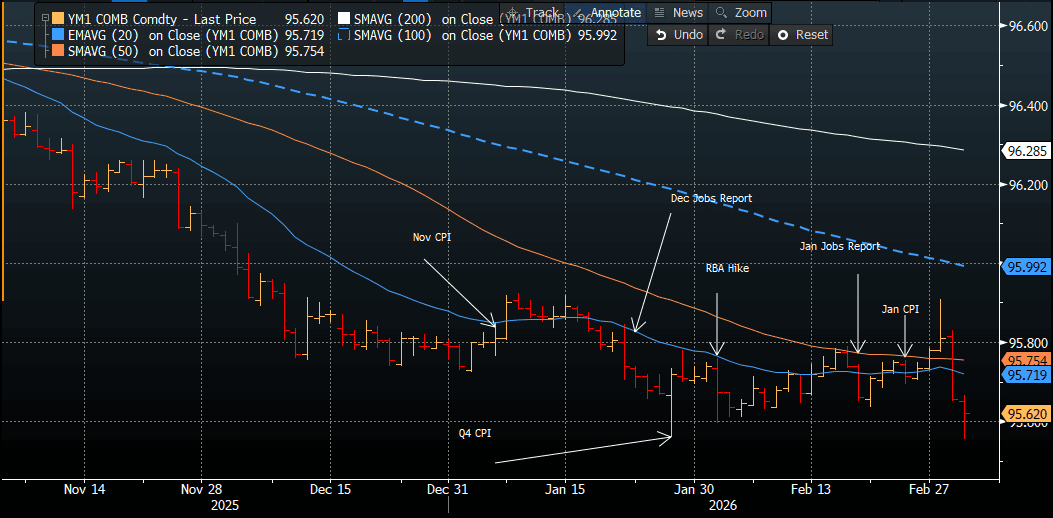

AUSSIE 3-YEAR TECHS: (H6) Corrective Phase

- RES 3: 96.700 - High Sep 12

- RES 2: 96.260 - Congestion High Nov 19 -24 ‘25

- RES 1: 96.925 - High Jan 9 and a key short-term resistance

- PRICE: 95.625 @ 16:02 GMT Mar 03

- SUP 1: 95.555 - Low Mar 03

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.776 - 1.0% 10-dma envelope

The primary trend structure in Aussie 3-yr futures is bearish - MA studies are in a bear-mode set-up highlighting a dominant downtrend. This suggests that recent gains are corrective. Resistance to watch is 95.925, the Jan 9 high. A clear break of it would signal a short-term reversal. For bears, a move lower would refocus attention on the year-to-date lows at 95.560 (Jan 27) and major support. A breach of it would confirm a resumption of the downtrend.

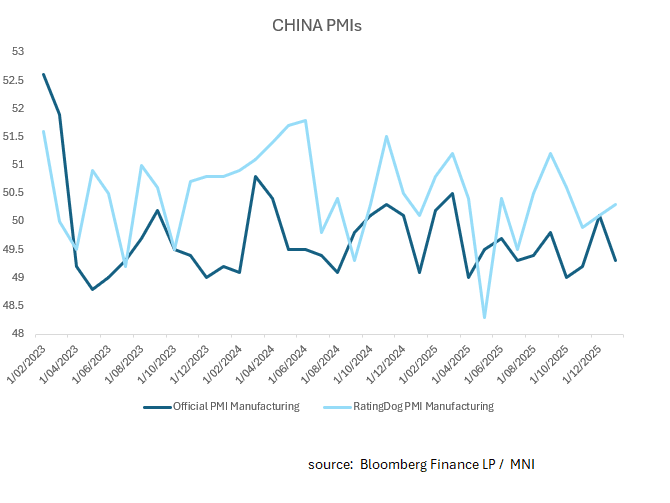

CHINA: PMIs Scrutinized Ahead of NPC

Today's dual PMI data release serves as the final economic health check for China before the National People's Congress (NPC) convenes tomorrow.

- The official government data focuses on large, state-owned enterprises and is expected to show continued domestic struggles.

Manufacturing Forecast: 49.2 (Previous: 49.3).

Non-Manufacturing Forecast: 49.7 (Previous: 49.4).

Forecasts expect the official print to remain in contraction (below 50), weighed down by a significant slowdown in the construction sector and weak domestic consumer demand. - RatingDog (Caixin) PMI (Private Co's)

The RatingDog (formerly Caixin) index surveys smaller, private, and export-oriented firms. It has recently outperformed the official data due to robust overseas demand.

Manufacturing Forecast: 50.1 (Previous: 50.3).

This index is expected to hover right on the neutral 50-mark. While new orders and exports have supported the sector, business sentiment recently hit a nine-month low due to rising input costs for metals and general economic uncertainty.

Markets are watchging closely for output from the NPC this week. A simultaneous miss on both figures would intensify pressure to announce a more expansionary fiscal stance at the NPC, including a potential 4.0–4.5% fiscal deficit target and monetary policy measures (RRR cuts currently favoured).

AUSSIE BONDS: Cheaper, Oil Price In Focus, Q4 GDP & Oct-37 Supply Due

ACGBs (YM -4.0 & XM -2.0) are weaker after US tsys finished 2-3bps cheaper across benchmarks as markets continue to focus oil price & the US/Israel conflict with Iran.

- Pres Trump posted on Truth Social: "Effective IMMEDIATELY, I have ordered the US Development Finance Corporation (DFC) to provide, at a very reasonable price, political risk insurance and guarantees for the Financial Security of ALL Maritime Trade, especially Energy, traveling through the Gulf.

- Today, the local calendar will see Q4 GDP.

- MNI AU - Consensus for Q4 GDP growth in Australia sits at 0.8%q/q, and 2.3% y/y. The consensus forecast range for the q/q outcome sits at 0.5 to 1.2%. If the 0.8%q/q outcome is realised it would be the strongest rate of growth since the end 2022 (when growth was +0.9%q/q).

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +73bps.

- The bills strip is -2 to -5 across contracts, late whites leading.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for March to 114% by May and 203% by December 2026.

- The AOFM plans to sell A$900mn of the 4.75% 21 October 2037 bond today and A$800mn of the 1.50% 21 June 2031 bond on Friday.

Bloomberg Finance LP