EU TRANSPORTATION: Lufthansa: 3Q Results

(LHAGR: Baa3/BBB-/BBB-)

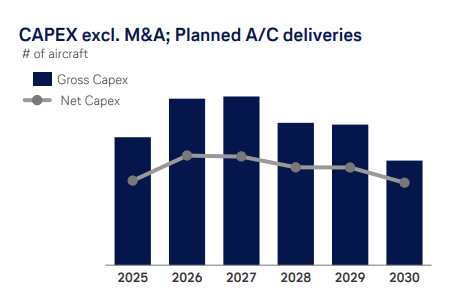

The weakness in unit revenues (-0.4% ex. FX) is in line with Air-France & IAG and is on soft US and European yields. On cost side +1% ex. fuel unit cost inflation is relatively subdued/good. Outside airlines group earnings is continuing to get support from solid demand for maintenance services and (volatile) cargo. It says unit revenue trends for 4Q are better but note FCF will be negative on seasonality & a capex bump (~guidance implies -€1b). Capex ramp up continues for next few years (below from CMD). Earnings itself not a credit mover, Lufthansa does, and always has traded tight supported by retail denoms. Non-retail 29s equally un-interesting.

- ASK (capacity) +3.2%

- Yield -5.4% (-3.8% ex. FX), Load factor 87.5% (+40bps) leaving RASK -2.2% (-0.4% ex. FX)

- 3Q RASK was down -9.5% in NA (incl. FX headwind) and -6.3% in Europe

- YTD yield weakness (-1.4%) driven by Europe (-4%) and NA (-1.6%)

- Airline revenue €9b, +1%

- CASK ex. Fuel +0.5% (+1.2% ex. FX). Fuel €0.2b tailwind

- YTD +2.5% (ex. FX +2.3%)

- Left airline EBIT at €1.2b, flat y/y on a 12.9% margin (-20bps)

- Technik (maintenance arm), continues strong growth, revenue €2b, +10% y/y. Tariffs (40% of the fall) and production expansion costs left EBIT at €130m, -19%

- Cargo continues growth, revenue €824m (+5%), adj. EBIT €49m (vs. €38m LY)

- Together group EBIT €1.3b, -1%, on a 11.9% margin (-60bps). YTD €1.5b, +€0.3b y/y

- FCF was €818m (vs. €128m LY) boosted on WC, taxes and capex push-back

- Net debt of €7.2b vs. €7.7b LY, levered 1.6x (vs. 1.9x LY)

- Bookings across Nov-Jan are at lower yields (net of FX) - but much less severe than -5.4% in 3Q. Bookings up +2-3% in Dec & Jan. Capacity growth is muted helping boost load factors.

Guidance unch for:

- 4Q CASK increase to be less than YTD level (2.5%)

- 4Q RASK to stabilise/improve vs. 3Q (-0.4%)

- FY EBIT to "significantly increase"

- Net capex €2.7-3.3b (€2.4b LY)

- adj. FCF stable y/y (€840m LY)

FY26 Outlook:

- Capacity +4%

- adj. FCF stable y/y

- guided pick-up in net capex

- 71% hedged on fuel for 2026

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Largely Dovish Tilt Since Pre-September Meeting But Divisions Persist (2/3)

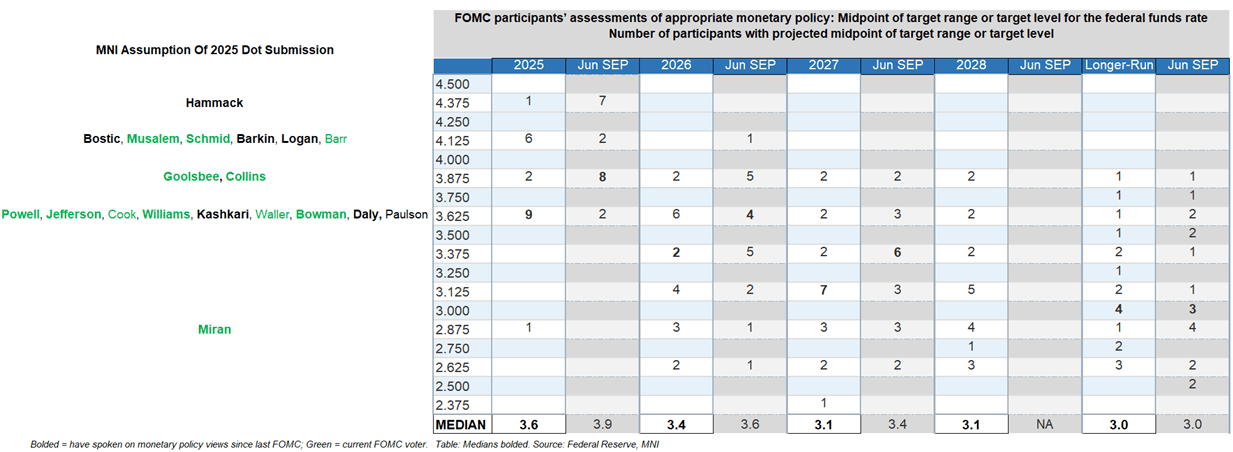

In the September Dot Plot, there were 9 rate dots at 3.9% or above for this year and 10 at 3.6% or below, making the latter the 2025 median. We presume that includes the leadership of the Committee including Chair Powell. But interesting that one saw no cuts this year (and it wasn't a voting dissenter) and 6 see this as the last reduction. For 2026 the highest dot has shifted lower by 25bp to 3.9%, but again it's a fairly split median. 8 members are at 3.6% or higher (was 10 previously), with 11 at 3.4% or below (vs 9 prior). And while the longer-run median was unchanged at 3.00%, the new distribution and post-meeting participant commentary point to rising longer-run neutral rate estimates. See below for our assumption of participants’ 2025 submissions.

- Since the meeting, the rest of the FOMC largely following their own pre-meeting scripts albeit most expressed a slightly more dovish tilt in keeping with the shift in the broader Committee’s perception of the balance of risks. We go through all the key commentary in our PDF preview (sent separately). All participants acknowledged that recent labor market indicators have signaled rising risks to that side of the dual mandate, and largely noted that tariff impacts on inflation were more limited than foreseen, though the conclusions differed on what that means for monetary policy.

- Current voters Musalem and Schmid for example supported the September cut, but it’s doubtful they anticipate support for any more this year given inflation risks. Non-2025 voters Hammack, Logan, and Bostic also suggested they didn’t see any further cuts this year, with Bostic the most open-minded of the three about another easing.

- As for the other two 2025 regional voters, Goolsbee cautioned against too much front loading of cuts, while Collins eyes “a bit” more easing – suggesting that they may only see one further cut this year.

- But a majority of the 12-member FOMC voters – including 7 of 8 permanent voters – are likely to see at least another 2 cuts this year. Waller, Bowman, and (especially) Miran are the strongest proponents of further cuts, but Powell, Jefferson, Cook, and Williams are all likely in the camp of two further cuts. The latter are joined by Kashkari and Daly, and, in an assumption, Paulson who is yet to speak on monetary policy since joining the FOMC this summer.

- Among the 19 we have the least conviction on dot placement for Barkin, Barr, and Goolsbee, but given the numbers we think they are either on the side of 1 or 2 further cuts.

EU: VdL Faces Latest No Confidence Votes 9 Oct ~12:00CET, Neither Likely To Pass

President of the European Commission Ursula von der Leyen faces two votes of no confidence on Thursday, 9 October. Voting will take place from ~12:00CET (06:00ET, 11:00BST). One of the motions was put forward by the right-wing populist Patriots for Europe (PfE) group, and another by the far-left The Left group.

- As was the case in July, neither motion is likely to succeed. In order for a no confidence motion against a Commission to pass, it needs at least a two-thirds majority of those voting, representing at least half of all MEPs. With 719 MEPs in total, this requires 360 MEPs to vote against VdL for a censure motion to pass.

- This threshold cannot be achieved unless sections of the 'moderate' groups, the centre-right European People's Party, centre-left Socialist and Democrats or liberal centrist Renew Europe, vote in numbers against the Commission. None of these groups is willing to formally back motions put forward by the far-left or far-right.

- In the July censure motion, 175 MEPs voted against the Commission, with 360 in favour and 18 abstentions. The remaining 167 MEPs did not vote.

- The 360 MEPs voting in favour represented a decline from the 370 that backed the Commission in the November 2024 censure motion, and from the 401 that voted in VdL for a second term as Commission president in July 2024.

- Another decline in the number of MEPs willing to back the Commission would not be fatal for the VdL Commission, but could further weaken its position amid long-running arguments over the EU's stance on issues as varied as Gaza, trade with the US, immigration, and the green agenda.

FED: US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $69.000 BLN TOTAL

- US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $69.000 BLN TOTAL