JAPAN DATA: Local Investors Return To Offshore Bonds, But Sell Global Equities

Aggregate Japan weekly investment flows were mixed in the week ending Nov 7 (last Friday). In terms of Japan outbound flows, we saw a pick up in offshore bond buying, which ended a 3 week run of net outflows from this segment. As we have noted in recent weeks, cumulative outflows to offshore bonds have remained positive, owing to chunky net buying through late Aug, early Sep. Global bond returns have broadly moved sideways, not providing a fresh impetus for local investors. Japan investors continued to sell overseas equities, with net outflows in 7 out of the last 8 weeks. Strength in local equities may be keeping the home bias firmer, particularly with new PM Takaichi's pro-growth regime.

- Offshore investors did sell local Japan equities last week, albeit only modestly. This ends a run of five straight week of inflows. Offshore cumulative inflows have also been strongly positive in the past 6 months. Japan equities remain supported on dips, but the NKY is off earlier Nov highs.

- Offshore investors added to local bonds, but only modestly.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Nov 7 | Prior Week |

| Foreign Buying Japan Stocks | -347.3 | 690.1 |

| Foreign Buying Japan Bonds | 91.5 | 280.6 |

| Japan Buying Foreign Bonds | 566.3 | -354.5 |

| Japan Buying Foreign Stocks | -439.5 | -581.1 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Continues Rally Without New Drivers

Gold has continued to rally today despite a flat US dollar, 2-year yields and S&P e-mini as it appears to be carried by momentum with no new fresh catalysts. It is now up 7.8% in October and currently 1.3% higher at $4164.0/oz today, around the record high of $4164.24, above resistance at $4161.7. US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and for the US to negotiate. Gold & silver are looking even more stretched.

- After rising over 4% on Monday, silver continued to rally Tuesday driven by momentum and significant liquidity issues in London. The metal is up 1.6% to $53.20 today after an all-time high of $53.465 earlier in the APAC session, above the fourth resistance level at $52.689, a Fibonacci projection. It is now up over 14% this month.

- Societe Generale revised up its gold forecast to $5000/oz for end-2026, according to Bloomberg, due to strong ETF and central bank flows, which had exceeded its expectations.

- The ongoing US government shutdown is also supporting precious metals with no apparent progress to end the impasse. Wednesday military personnel will miss their first pay but President Trump has said money will be found. It would be the first time in modern US history if it occurs.

- US September CPI was scheduled for 15 October but has now been delayed to 24 October contributing to difficulty in gauging where the economy is ahead of the 29 October Fed decision.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism, UK labour market data and German September HICP and euro area October ZEW print.

FOREX: Higher Beta FX Struggling, NZD At Fresh Multi Month Lows, JPy Firmer

Risk currencies are underperforming as Tuesday trade unfolds, the softer tone to China/HK equities likely weighing at the margins. Otherwise fresh catalysts are lacking, gold and silver continue to rally, but they may hint at broader mkt risk aversion. USD/JPY is also off session highs (last 152.15/20), helped drive yen crosses lower. We saw another round of verbal FX jawboning from FinMin Kato. The pair was 152.15 in latest dealings, against session highs of 152.10/15.

- AUD/USD is testing under 0.6500(still above Friday lows of 0.6473)

- NZD/USD is lower though, eyeing 0.5700 test, levels last seen in April of this year. (last 0.5710).

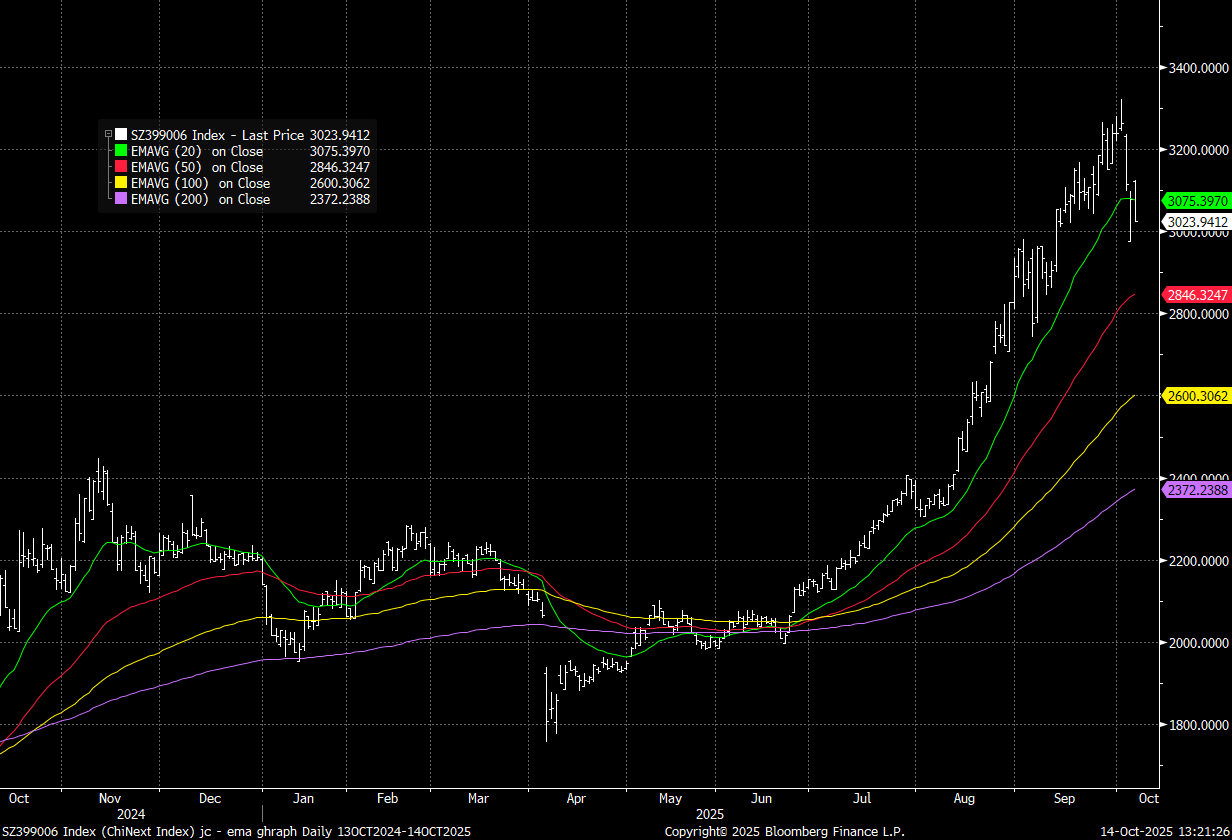

CHINA STOCKS: China/HK Equities Still Struggling Despite Better Global Trends

China/HK equities still struggling to maintain positive momentum, despite the broader gains seen over the past 24hrs in global equities. With sentiment stabilizing amid Trump's softer comments around China. Positioning/valuation concerns (tech headwinds amid export control fears) may also be playing a role. Chipmaker Wingtech also down earlier today after the Dutch government took control of its Nexperia unit.

- The Chinext is plotted in the attached, still above yesterday's intra-session lows, but sub 20-day EMA.

Fig 1: Chinext Equity Index Versus Key

Source: Bloomberg Finance/MNI