JGBS: Little Changed, HH Spend Lower Than Expected

In Tokyo morning trade, JGB futures are stronger, +8 compared to settlement levels, but well off session bests.

- Japan's Sep real household spending data was softer than forecast. Real spending fell 0.7%m/m, against a -0.1% forecast (per Rtrs). In y/y terms, we were up 1.8%y/y, against a 2.5% forecast.

- Offshore investors added to Japan bonds last week, but cumulative inflows were only modestly positive for most of Oct. In terms of Japan's outbound flows, we saw local investors continue to sell offshore bonds. This marked the fifth out of the last six weeks we have seen net selling in this space. Cumulative outflows to offshore bonds have still been positive in recent months, due to chunky buying through September. Global bond returns have struggled for upside in recent months, largely flat since early Sep.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday’s sold rally.

- Cash JGBs are little changed across benchmarks. The benchmark 10-year yield is at 0.6bp lower versus the cycle high of 1.705%.

- Swap rates are ~1bp higher.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

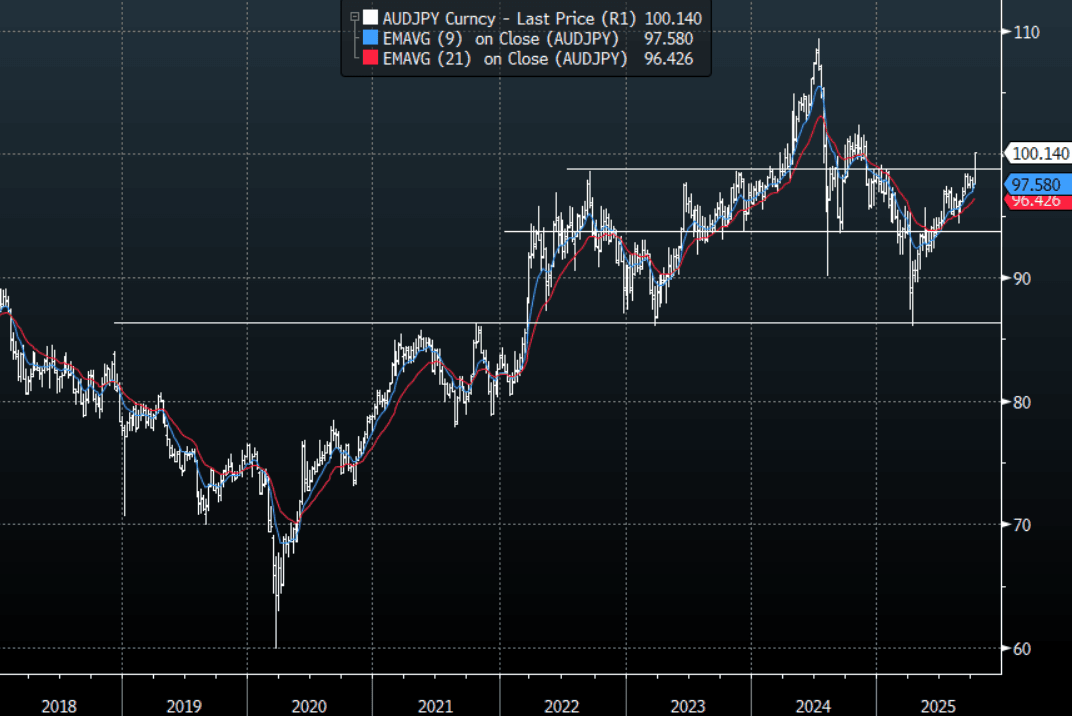

FOREX: AUD Crosses-Outperformance Stalls With Risk, AUD/JPY Disregards Tests 100

US equities have shown the first signs of the huge rally potentially becoming exhaustive as momentum higher seems to be stalling. This morning US futures have opened pretty muted, E-minis(S&P) +0.01%, NQZ5 +0.03%. The AUD outperformance has also stalled, outside of AUD/JPY which is now challenging above 100.00.

- EUR/AUD - Overnight range 1.7683 - 1.7737, Asia is currently trading around 1.7710. The pair has found some decent demand sub 1.7700. Price remains trendless within its recent 1.7600 -1.8100 range. Look for sellers to fade bounces while the price remains below 1.7850/7900.

- GBP/AUD - Overnight range 2.0338 - 2.0423, Asia is trading around 2.0395. The move lower has stalled back toward its support around 2.0300 where demand has initially returned. The price action of the pair is looking potentially exhaustive but a sustained break sub 2.0300 is needed to open up a deeper pullback towards 1.9800/2.0000.

- AUD/JPY - Overnight range 99.17 - 100.04, Asia is trading around 100.15. The pair has surged higher for good reason on the election outcome. The pair extended its move higher even with risk wobbling. Dips will now be supported as the focus now turns toward 100 and then beyond.

- AUD/NZD - Overnight range 1.1338 - 1.1357, the cross is dealing in Asia around 1.1350. The Cross has seen some selling to cap the move above 1.1400 for now, price action suggests we could potentially see more reversion back to the mean but expect dips back towards 1.1200 to now be supported. Depending on how the RBNZ comes out today will impact which side is tested, a 50bps dovish cut would see another challenge above the 1.1400 area.

Fig 1: AUD/JPY spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Weak Earnings Data But market Slightly Cheaper

In Tokyo morning trade, JGB futures are weaker, -16 compared to settlement levels, and at session lows.

- August labour earnings data in Japan was comfortably below market expectations. Headline earnings rose 1.5%y/y (against a 2.7 forecast and 3.4% July outcome), while real earnings dipped back to -1.4%y/y (-0.5%) was forecast. Real earnings have not been in positive territory (in y/y terms) so far in 2025. This will reinforce expectations of the BoJ likely remaining on hold at the Oct policy meeting.

- Japan's new political regime had already noted that Oct is too soon for a rate hike. BoJ Governor Ueda also noted recently that the risk was low for the central bank to fall behind the inflation/policy curve (with today's data supporting this theme).

- Cash US tsys are flat to 1bp cheaper, with a steepening bias, in today’s Asia-Pac session after yesterday’s modest rally.

- Cash JGBs are flat to 1bp cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 0.9bp higher at 1.694% versus the cycle high of 1.699%.

- Swap rates are 1-2bps higher. Swap spreads are wider.

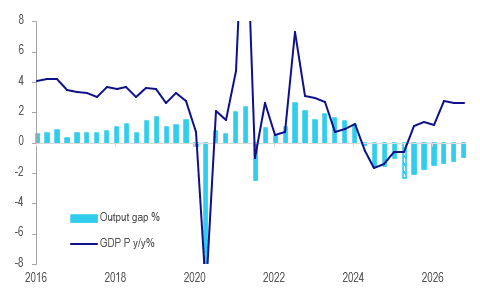

RBNZ: Spare Capacity To Require Further Easing

There are valid arguments for both 25bp and 50bp rate cuts at today’s RBNZ decision. One reason for an outsized reduction is that Q2 GDP contracted by significantly more than the RBNZ projected in August meaning that the degree of excess capacity was larger than it thought at that time. However, arguing for 25bp is that GDP is prone to large revisions and that the output gap may not actually be as large as it currently looks. Whatever the size, there is material spare capacity which is likely to require further easing.

- We have estimated a simple output gap using a Hodrick-Prescott. The current -0.9% q/q for Q2 production-based GDP results in the output gap widening around 1.3pp in the quarter.

- However, the output gap had been negative for the previous four quarters and while the size is difficult to estimate, especially as GDP will be revised in the future, it is clear that there is substantial spare capacity in NZ that requires further monetary easing.

- Using the RBNZ’s quarterly GDP forecasts, our estimate doesn’t have excess economic capacity being worked off until Q3 2027, in two years’ time. This implies that rate cuts could continue into 2026 shifting policy into stimulatory territory.

- The RBNZ estimates the “neutral” rate to be between 2.5% and 3.5%. Consensus has the OCR declining to 2.75% this month but analysts are split with many forecasting 2.5%.

NZ GDP (production) y/y% vs output gap %

Source: MNI - Market News/LSEG