US STOCKS: Late Equity Roundup: Comm Services, IT, Consumer Shares Hold Support

Jul-28 18:59

- Stocks are moving higher again in late trade after paring back from midday highs (SPX appr 18.0 off Thu's two-year highs before a Nikkei sources story on re: BoJ tweaking yield curve control spurred a sell-off in stocks and rates). Currently, DJIA is up 178.83 points (0.51%) at 35463.71, S&P E-Mini Futures up 44.5 points (0.98%) at 4609, Nasdaq up 277 points (2%) at 14327.38.

- Communication Services, Information Technology and Consumer Discretionary sectors continue to lead gainers Friday. Communication Services led by strong gains in Meta up another +4.0% after earnings and forward guidance beat expectations early Thu. Warner Bros +3.95% and Netflix +3.1%. Underlying demand by AI applications continued to buoy chip stocks/IT sector: Intel +5.85% after returning to profitability following two consecutive quarter losses, First Solar +5.55%, KLA +5.25%, Applied Materials +4. Auto makers leading Consumer Discretionary w/ Tesla +4.1%.

- Laggers: Utilities, Energy and Financials underperformed late. Exxon -2.12%, Kinder Morgan -1.4% and Chevron -1% weighed on broader but smaller gains elsewhere in the Energy sector. Meanwhile, Insurance companies weighed on financials in the second half, Hartford -4.95%, AON -4.65%, PFG -4.17%

- Technical focus on today's rebound puts focus on 4634.50/38.27 (High Jul 27 / Bull channel top) where clearance of the channel top is required to resume the uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

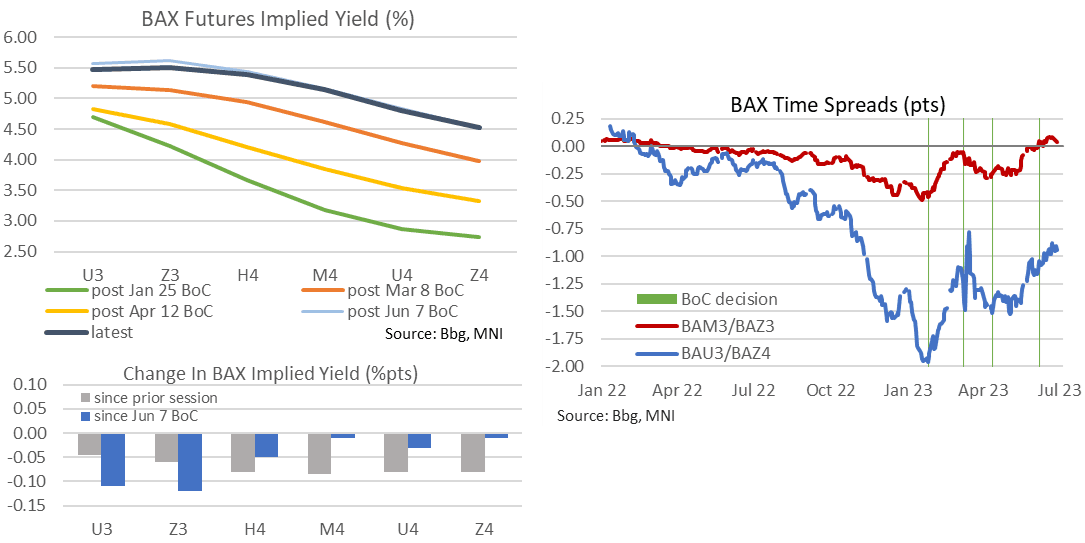

CANADA: Backloaded Rally In CAD Rates

Jun-28 18:56

- 10s may be leading the GoC rally on the day but the front end has still seen a decent -6bp decline.

- The latter’s dynamics are supported in rates markets, with BAX futures rallying 4 ticks for the front Sep’23, 6 ticks for the Dec’24 and building to 8.5 ticks through mid-2024.

- The upshot is that implied yields for 2H23 are now ~10bps lower than after the BoC Jun 7 hike (i.e. unwinding half of the then sell-off) and marginally lower for all 2024 contracts as well. The BAU3/Z4 spread widens back to -95bps although remains tight relative to recent months.

- In the near-term, OIS rates imply a 15-16bp hike for the Jul 12 decision, down from 17bp pre CPI, but still with the BoC surveys and monthly GDP this Fri before the employment report the following Fri.

US TSYS: Late SOFR/Treasury Option Roundup

Jun-28 18:48

- Generally quiet FI option trade Wednesday, two-way positioning in SOFR calls and midcurve volatility sales reported. Salient trade includes:

- SOFR Options

- 4,000 SFRM4 96.50/98.50 call spds, 23.0 ref 95.435

- -4,000 SFRH4 98.00 calls, 4.5

- over 3,000 SFRU3 94.56 puts, 1.5 ref 94.635

- 2,500 SFRU3 94.50/94.56/94.62 put flys, ref 94.625 to-.63

- -8,000 OQZ3 94.50/98.00 strangles, 8.5

- -5,000 SFRU3 95.00/95.50/9600 call flys, 1.0 vs. 94.655/0.06%

- +10,000 SFRU3 95.00/95.25 call spds, 1.5 vs. 94.665/0.05%

- +10,000 OQU3 96.50/97.00 call spds vs. 2QU3 97.25/97.75 call spds, 2.0 net steepener

- -5,000 SFRZ3 95.50 calls, 13.0 vs. 94.725/0.20%

- 2,000 SFRU3 94.43/94.62 put spds ref 94.645

- 3,000 SFRU3 94.75/94.87 put spds ref 94.65

- 3,000 OQU3 96.00/96.50/97.5 broken call trees ref 95.85 to -.855

- Treasury Options:

- -6,000 TYU3 111.5/113/114.5 iron flys, 3 net (2xstrangle vs. 1xstraddle)

- over 2,100 FVU3 101.5 puts, 1 ref 107-20.25

- over +7,500 FVQ3 109 calls, 9-9.5 ref 107=20.75

- 2,750 TYQ3 115 calls, 11 ref 112-31

- over 8,100 TYQ3 114 calls, 22 ref 112-30

- over 5,500 TYQ3 112 puts, 24 ref 112-28.5

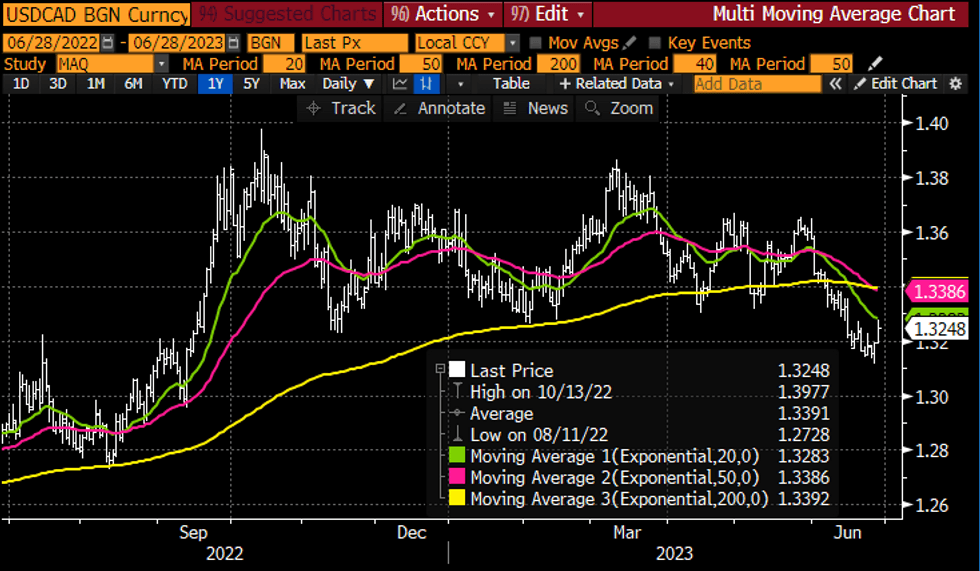

CANADA: USDCAD Climb Stopped Short Of Firmer Resistance, Decent Expiry At 1.315 Tomorrow

Jun-28 18:41

- CAD has seen somewhat mid-pack performance today despite a solid recovery in WTI, following yesterday’s CPI-induced underperformance.

- USDCAD is currently ~1.325 (+0.4%) having earlier topped out at 1.3277 to stop short of firmer resistance at 1.3286 (20-day EMA).

- The technical set-up suggests the bounce off yesterday’s pre-CPI trend low of 1.3117 could be corrective with the trend outlook remaining bearish, but a breach of the 20-day EMA could easily open 1.3355 (Jun 15 high).

- One factor that could limit a further bounce for the pair is a sizeable $1.055B of expiry at 1.3150 with tomorrow’s NY cut. It will however follow second tier domestic releases of the CFIB survey and the lagged SEPH report plus potentially more of note the third release of US GDP and initial claims.

Source: Bloomberg

Source: Bloomberg

Trending Top

Mar-27 20:13