ECB: Lane Eyes Wage Strength Amid "Nuanced" Service Momentum

ECB Chief Economist Lane's speech this morning (titled "Underlying Inflation") assesses that some signs of easing are emerging but while overall inflation pressures are still strong.

- That said, core inflation momentum remains robust, particularly in goods, while core services inflation momentum is more "nuanced" (for example, services price momentum began easing in Aug but picked up again in Feb when looking at a data series that excludes the German cheap travel ticket scheme).

- Wage growth is expected to be the main driver of euro area underlying inflation this year and next, with the pace of pay increases likely greater than that foreseen late last year. (Notably the word "wage" appears 80 times in Lane's speech, reinforcing the idea the ECB is watching this area very closely).

- Pretty limited market impact from his comments, which suggest 50bp looks like a done deal for March.

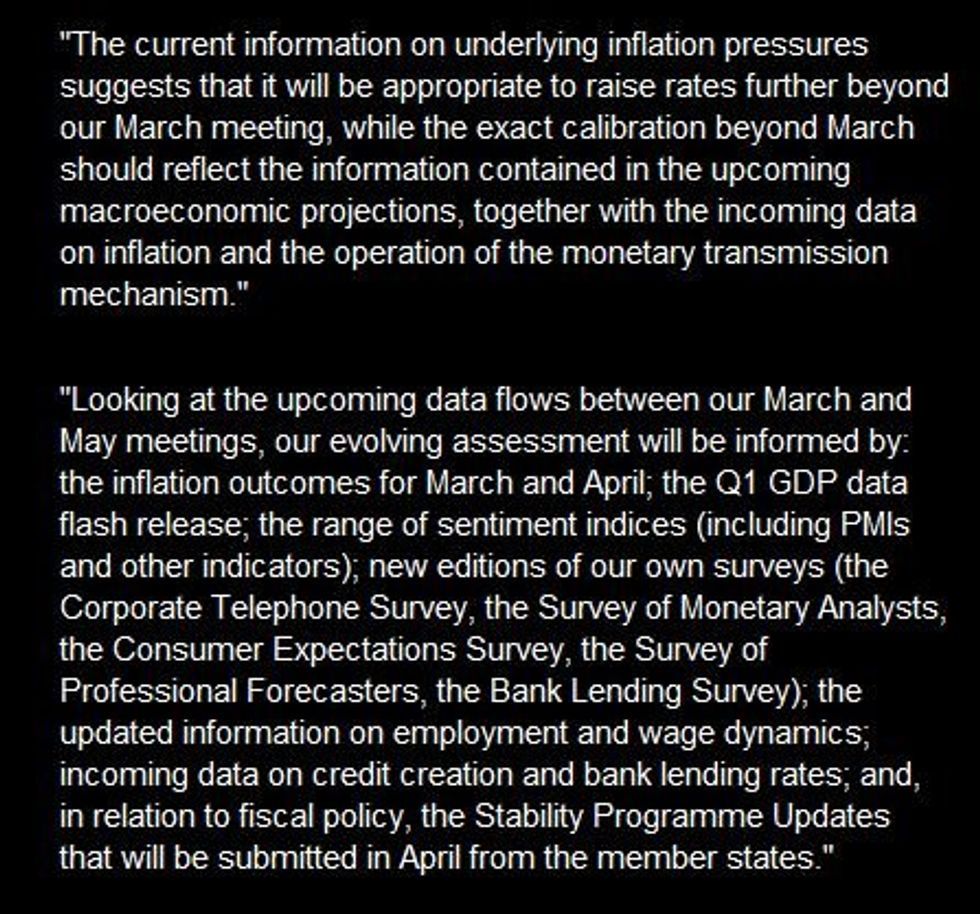

- On that note, Lane provided a list of key data the ECB will be watching between then and April, including several ECB surveys - see text in image below.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Key Support Remains Exposed

- RES 4: 1.3751 High Nov 4

- RES 3: 1.3705 Dec 16 and the bull trigger

- RES 2: 1.3665 High Jan 6

- RES 1: 1.3472/3521 High Jan 31 / 19 and key short-term resistance

- PRICE: 1.3387 @ 16:34 GMT Feb 3

- SUP 1: 1.3262 Low Feb 2

- SUP 2: 1.3226 Low Nov 15 and bear trigger

- SUP 3: 1.3205 61.8% retracement of the Aug 11 - Oct 13 rally

- SUP 4: 1.3131 0.764 proj of the Oct 13 - Nov 15 - Dec 16 price swing

USDCAD bearish trend conditions remain intact despite the Friday rally and the pair remains closer to recent lows. A continuation would strengthen bearish conditions and signal scope for weakness towards 1.3226, the Nov 13 low and the bear trigger. Moving average studies are in a bear mode position, highlighting a downtrend. On the upside, the pair needs to clear 1.3521, the Jan 19 high, to signal a reversal.

AUDUSD TECHS: Pullback Extends, But Still Looks Corrective in Nature

- RES 4: 0.7245 2.00 proj of the Nov 21 - Dec 13 - Dec 20 price swing

- RES 3: 0.7202 High Jun 9

- RES 2: 0.7172 1.764 proj of the Nov 21 - Dec 13 - Dec 20 price swing

- RES 1: 0.7158 High Feb 2

- PRICE: 0.6963 @ 16:32 GMT Feb 3

- SUP 1: 0.6930 Low Feb 3

- SUP 2: 0.6872 Low Jan 19 and a key support

- SUP 3: 0.6873 50-day EMA

- SUP 4: 0.6722 Low Jan 6

The AUDUSD uptrend remains intact and short-term weakness is considered corrective, although Friday’s dip could signal a more protracted move lower. The print above resistance at 0.7142, Jan 26 high this week, confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position, reflecting positive market sentiment. The focus is on 0.7172 next, a Fibonacci projection.

US TSYS: FED Remains in Play Post-NFP/ISM Data

Off lows, Tsy futures remain broadly weaker after this morning's surge in job gains for January of +517k, 2.75x larger than the mean estimate of 188k (and well over 320k high estimate survey of 77 economists by Bbg). Tsy 30YY at 3.6288% +.0840, yield curves extend inversion: 2s10s -6.590 at -78.151%).

- Unemployment rate sank a tenth to 3.4%, the lowest since 1969, the Bureau of Labor Statistics reported Friday. November and December payrolls figures were also revised 71,000 higher.

- Meanwhile, ISM services was far stronger than expected in January at 55.2 (cons 50.5), back at the 55.5 in Nov via December's 49.2. The largest increase since Jun'20 followed the largest downward surprise since 2008.

- Short end rates gapped lower as markets reverted back to more (possibly larger) rate hikes ahead - but moderated somewhat in the second half. Fed funds implied hike for Mar'23 at 22.5bp (vs. 23.3bp post-ISM), May'23 cumulative 37.5bp to 4.957%, Jun'23 41.5bp to 4.997%, terminal climbs to 4.980% in Jun'23.

- Goldman Sachs' chief economist Jan Hatzius tweeted “this morning’s report provides strong evidence of continued economic expansion in January. We continue to expect two more 25bp fed funds rate hikes in March and May, and we continue to expect no rate cuts in 2023."