EMISSIONS: Lagarde says ETS2 on Track for 2027, Impact May Be Phased In

Q on ETS2 impact:

ETS2 has been in our projection since it was on the table, and has been in there since 2024 I don't think I would read too much again into an expected delay of the implementation.

And when I speak to colleagues at the European Commission, they are still strongly of the view that ETS2, which is committed, must proceed and the deadline for implementation is still 2027. What, on the other hand, is being discussed and has been put on the table by the Commissioner is, how would I put it, a slight smoothing in the implementation of ETS2, which means that the impact might be spread a little bit more over time, possibly a bit less in 2027 and a bit more in 2028. So overall, as with many other data, we will be attentive and the December projection exercise will certainly take that into account, that smoothing over a slightly longer period in order to make sure that ETS2, which is so important for climate change purposes, will actually be implemented.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

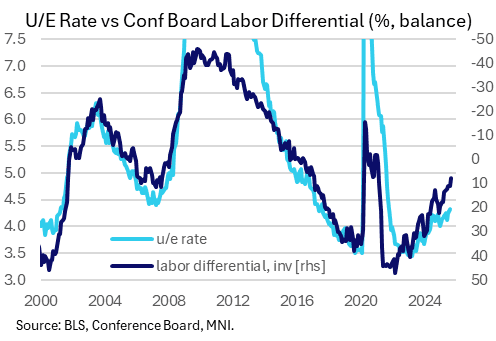

US DATA: Conference Board Labor Differential Hits Fresh Cycle Low

Standing out in a broadly weak Conference Board consumer confidence survey for September, the "labor differential" (jobs "plentiful" minus "hard to get") fell to 7.8 from 11.1 in August (rev from 9.7). That's the weakest since 2017 when excluding the 2020-21 pandemic period.

- While the percentage of those seeing jobs as "hard to get" was steady at 19.1%, the proportion seeing jobs as "plentiful" (26.9%) was the lowest since February 2021, but excluding the April 2020-Feb 2021 pandemic period, it was the lowest since February 2017.

- This is a closely-watched indicator for broader labor market conditions. It's historically correlated with the unemployment rate and having come down from over 22 at the end of last year, this has shown a decisive cooling which points to a continued rise in joblessness. A similar reading in 2017 was consistent with unemployment around 5.0%, vs 4.3% as of August.

US TSY FUTURES: BLOCKs: Dec'25 5Y & 30Y Sales

Futures coming off recent highs after latest Block sales:

- -3,000 USZ5 117-02, sell through 117-03 pos time bid at 1019:10ET, DV01 $42,600

- -10,400 FVZ5 109-09.5, sell through 109-10 post time bid at 1017:41ET, DV01 $456,400

FED: Boston's Collins: Limited Further Easing Possible By Year-End

Boston Fed President Collins (2025 FOMC Voter) says in a speech Tuesday (link) that "it may be appropriate to ease the policy rate a bit further this year – but the data will have to show that". This indicates that she may not be one of the 9 FOMC members at the median 3.6% dot seen in the latest SEP projections. Instead she may only see one further cut this year (there are two of 19 members in that camp). To take a literal interpretation, Collins says it may be appropriate to ease "a bit further" this year; having described the September 25bp cut as "a bit of easing", so it would stand to reason she is referring to 25bp moves in both instances.

- This would be 25bp more easing in 2025 than she saw as recently as July, when she said that one rate cut by year-end would likely be appropriate. Subsequently at Jackson Hole, she said “it is not a done deal in terms of what we do at the next meeting. But a range of possibilities is on the table and we are going to get more data between now and then."

- She supported the 25bp September cut because "in my view, a bit of easing was appropriate to address the recent shift in the balance of risks to our inflation and employment mandate. But I continue to see a modestly restrictive policy stance as appropriate, as monetary policymakers work to restore price stability while limiting the risks of further labor market weakening."

- Collins's "baseline outlook continues to be relatively benign. I anticipate hiring will pick up as firms adjust to the new tariff environment. And while inflation is likely to remain elevated into next year, I expect it to resume its gradual return to target over the medium term. This outlook is similar to the median forecast in the September Summary of Economic Projections (SEP)." Note that the latest PCE medians were: 3.0% 2025, 2.6% 2026, 2.1% 2027.

- But "in this highly uncertain environment, I do not rule out scenarios featuring higher and more persistent inflation, more adverse labor market developments – or both. Still, with less scope for inflationary pressures from the labor market, the upside inflation risks I was concerned about a few months ago are more limited."

- On the labor market she says "Anemic job gains amid solid economic growth are a somewhat puzzling combination." In Q&A she elaborates, saying "there's a lot of different indicators that I think make it quite clear that the labor market has softened... at the same time, there are a number of indicators that indicate what you might call a kind of curious type of balance" so assessing the incoming data will be key to "understand how labor supply and labor demand are evolving."

- She says in Q&A re inflation that "while I do expect tariffs to continue feeding through, I'm no longer expecting as large an impact as I had some months ago."