ECB: Lagarde: Additional Upside Inflation Risks Flagged

Q: "Could you elaborate a little bit more about the GC discussion about inflation risks, because in recent days, some members seemed more concerned about upside risk but other weren’t? So what are the position now?"

A: "I'm happy to say that we discuss actively in a very friendly manner. So you have a distinction between those who have a more upbeat view and those who have a more downbeat view. You may categorize them as the hawks and the doves and those categories do exist. But I'm happy to say that on the occasion of this meeting, in fairness, there was absolutely anonymity on the part of all members of the governing council to arrive at the decision that I have mentioned earlier".

- "Now let me mention a few elements that we discussed or that we are attentive to. One risk that we have not yet seen materialize and could be a risk to the upside, so we will continue to be attentive to that is the risk that would result from potential bottlenecks and disruption in the supply chain. We are still to understand exactly what the outcome of the discussions between the US authorities and the Chinese authorities will deliver in terms of rare earths in particular, which is a very material segment of the supply chains in quite a few sectors, including the automotive sector, but the energy sector as well. It's not a big amount in terms of actual volume, but it's critical at the juncture where it is situated in the in the production chain, but that risk has not yet materialised. We shall see we are in this sort of wait and watch or wait and see mode in relation to that specific risk".

- "There are two other areas that we are attentive to, and that is the composition of inflation and the way in which the labour market evolves. You don't find it in the risk section, but I just want to mention these two because there are ingredients that feed into service inflation, which in September, has picked up by 0.1pp and they, of course, have an impact also on underlying inflation, particularly domestic inflation".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCKs: Dec'25 5Y & 30Y Sales

Futures coming off recent highs after latest Block sales:

- -3,000 USZ5 117-02, sell through 117-03 pos time bid at 1019:10ET, DV01 $42,600

- -10,400 FVZ5 109-09.5, sell through 109-10 post time bid at 1017:41ET, DV01 $456,400

FED: Boston's Collins: Limited Further Easing Possible By Year-End

Boston Fed President Collins (2025 FOMC Voter) says in a speech Tuesday (link) that "it may be appropriate to ease the policy rate a bit further this year – but the data will have to show that". This indicates that she may not be one of the 9 FOMC members at the median 3.6% dot seen in the latest SEP projections. Instead she may only see one further cut this year (there are two of 19 members in that camp). To take a literal interpretation, Collins says it may be appropriate to ease "a bit further" this year; having described the September 25bp cut as "a bit of easing", so it would stand to reason she is referring to 25bp moves in both instances.

- This would be 25bp more easing in 2025 than she saw as recently as July, when she said that one rate cut by year-end would likely be appropriate. Subsequently at Jackson Hole, she said “it is not a done deal in terms of what we do at the next meeting. But a range of possibilities is on the table and we are going to get more data between now and then."

- She supported the 25bp September cut because "in my view, a bit of easing was appropriate to address the recent shift in the balance of risks to our inflation and employment mandate. But I continue to see a modestly restrictive policy stance as appropriate, as monetary policymakers work to restore price stability while limiting the risks of further labor market weakening."

- Collins's "baseline outlook continues to be relatively benign. I anticipate hiring will pick up as firms adjust to the new tariff environment. And while inflation is likely to remain elevated into next year, I expect it to resume its gradual return to target over the medium term. This outlook is similar to the median forecast in the September Summary of Economic Projections (SEP)." Note that the latest PCE medians were: 3.0% 2025, 2.6% 2026, 2.1% 2027.

- But "in this highly uncertain environment, I do not rule out scenarios featuring higher and more persistent inflation, more adverse labor market developments – or both. Still, with less scope for inflationary pressures from the labor market, the upside inflation risks I was concerned about a few months ago are more limited."

- On the labor market she says "Anemic job gains amid solid economic growth are a somewhat puzzling combination." In Q&A she elaborates, saying "there's a lot of different indicators that I think make it quite clear that the labor market has softened... at the same time, there are a number of indicators that indicate what you might call a kind of curious type of balance" so assessing the incoming data will be key to "understand how labor supply and labor demand are evolving."

- She says in Q&A re inflation that "while I do expect tariffs to continue feeding through, I'm no longer expecting as large an impact as I had some months ago."

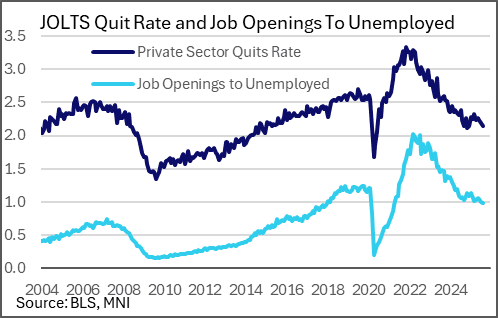

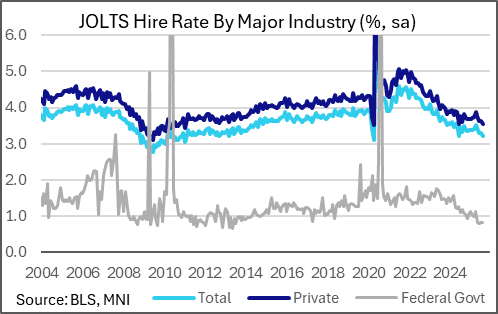

US DATA: JOLTS Reaffirms "Low Hiring, Low Firing" Labor Market Narrative

Job openings were relatively steady in August in the latest JOLTS report, totaling 7,227k (SA, vs 7,200k consensus) with July's slightly upwardly revised to 7,208k (from 7,181k). But secondary metrics suggested further loosening in labor market conditions, and while there was no marked deterioration in the month, overall the report bolstered the prevailing "low hiring, low firing" narrative.

- The first was the ratio of openings to the number of unemployed, which fell to 0.98 from 1.00 - lowest and first time below 1.0 since April 2021 (July's held that title, but was revised up from 0.99).

- The second was the quits rate, which fell to a 9-month low 1.9% (the number of quits fell to 3,091k vs 3,165k consensus - from 3,166k prior rev from 3,208k). The private sector quits rate dipped to 2.1% for the first time in 8 months, from 2.2% (we calculate at 2.14% from 2.20%). The rate dropped or was steady across the vast majority of sectors, with a fall in leisure and hospitality quits (3.3%, lowest in over a decade, from 4.2% prior) standing out in particular as this had been one of the hottest pandemic-reopening sectors.

- The third was a further deterioration in the hiring rate, at 3.21%, down from 3.28%. Excluding the pandemic-hit April 2020, that's the lowest hiring rate since September 2012. The private sector hiring rate is just 3.53%, with the government hiring rate of 1.36% (0.82% federal) both around the lowest in a decade or more (ex-pandemic).

- The fourth, in the "low firing" department, the level of layoffs was relatively tame at 1,725k, down from 1,787k prior for a 3-month low and well below the rise to 1,827k expected, keeping the layoffs rate steady at 1.1%.

- The vacancy rate ticked up very slightly (to 4.33% from 4.32%).