BUND TECHS: (Z5) Support Remains Intact For Now

- RES 4: 130.80 High Jun 13 and key resistance

- RES 3: 130.63 1.500 proj of the Sep 3 - 10 - 25 price swing

- RES 2: 130.07/59 High Oct 24 / 17 and the bull trigger

- RES 1: 129.73 High Oct 28

- PRICE: 129.39 @ 05:48 GMT Oct 31

- SUP 1: 129.12 50-day EMA

- SUP 2: 128.92 61.8% retracement of the Sep 25 - Oct 17 bull leg

- SUP 3: 128.52 76.4% retracement of the Sep 25 - Oct 17 bull leg

- SUP 4: 128.25 Low Oct 7

A short-term bear cycle in Bund futures remains intact. The move down that started on Oct 17 still appears corrective and this has allowed an overbought trend condition to unwind. The next important support to watch lies at the 50-day EMA, currently at 129.12. A clear break would signal scope for a deeper retracement. Key resistance has been defined at 130.59, the Oct 17 high. First resistance is 129.73, Oct 28 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Federal Gov't Shutdown: Payrolls, CPI Data Postponements Loom (1/2)

Amid the US federal government "shut down" starting today, we answer some of the most frequently asked questions we've received from clients.

- How long will it last? Prediction markets yesterday were signalling there's a higher than 50% market-implied chance that it lasts more than 5 days, and 40% it lasts more than 10 days. This would be the first full (and not "partial") shutdown since 2013 - that one lasted from Oct 1 to Oct 16 (regular operations resumed Oct 17).

- How will this impact data releases? With only essential government services being performed during a shutdown, this would effectively mean that any data from federal agencies including the Bureau of Labor Statistics, Bureau of Economic Analysis, and other agencies (commodities data via Dept of Agriculture and Dept of Energy) would be postponed until after the end of the shutdown. There would also be potential delays to subsequent releases as data collection is not able to be conducted.

- What are the data releases that are set to be postponed? The two key data releases that would be impacted by a shutdown through mid-month are Friday's Employment report for September, and the CPI report on Oct 15 (and PPI the next day). All the other not-quite 1st tier data, from construction spending to housing starts to trade balance, would also not be published (thankfully, the week of Oct 6 - 10 is unusually light). The Department of Labor's shutdown plans suggest there will be no weekly jobless claims reports published. These were published in 2013's shutdown, as while they were compiled and released by the BLS, they use state-by-state data. We go through the 2013 episode in more detail in the next note by way of illustrating what it could look like this time.

- What data will we get? Private-sector compiled data will still be released after September 30, and this will serve as an alternative of sorts to the official government data to gauge economic developments. Looking at the more immediate releases: for the labor market, this includes the ADP employment report and Challenger job cuts out this Wednesday and Thursday. For broader activity, we get ISM Manufacturing / Services (Weds and Fri). For retail sales we get indicators including the weekly Redbook release and Wards Automotive sales. Also Federal Reserve releases including the regional Fed surveys would be unaffected: in the 1st half of the month that includes NY Fed consumer survey and manufacturing surveys, as well as the Federal Reserve Beige Book.

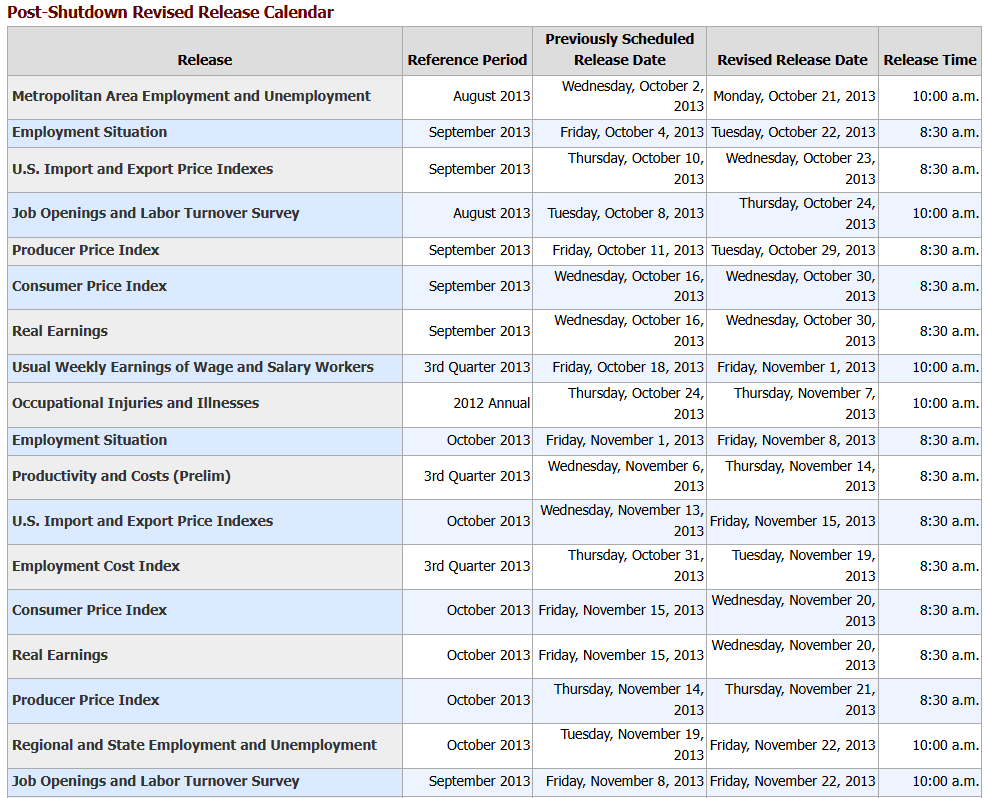

- When would data releases resume? In 2013, releases were pushed back to slightly after the end of the shutdown. That meant that there were some odd days of the week: the September 2013 payrolls data for example came out on Tuesday Oct 22 (instead of Fri Oct 4). The Department of Labor's notice summarizes the impact of a federal shutdown: "BLS will suspend all operations. Economic data that are scheduled to be released during the lapse will not be released.... The BLS website will not be updated with new content or restored in the event of a technical failure during a lapse. The releases of economic data will likely be delayed if a lapse is prolonged." See the table the BLS provided in 2013 after the shutdown ended to get a sense of the impact of delays.

- Will Treasury auctions be affected? These are considered "essential" and will be conducted as normal. However, bill auctions have already been increased for this week. 4-week by $5B to a record $105B, 8-week also by $5B to a joint-record $90B, and 4-month by $2B to a record $67B. Instead of raising $5B in net cash if they had been unchanged, these will raise $17B on next Tuesday Oct 7's settlement.

USDJPY TECHS: Tests Support At The 50-Day EMA

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 151.21 High Mar 28

- RES 2: 150.92 High Aug 1 and a key resistance

- RES 1: 149.96 High Sep 26 and the bull trigger

- PRICE: 147.53 @ 06:59 BST Oct 1

- SUP 1: 147.60/46 50-day EMA / Intraday low

- SUP 2: 146.77 Low Sep 18

- SUP 3: 145.49 Low Sep 17 and a pivot support

- SUP 4: 144.23 Low Jul 7

USDJPY continues to weaken as the retracement from last week’s high print extends. The move down - for now - appears corrective. Support to watch lies at 147.60, the 50-day EMA. It has been pierced, a clear break would expose pivot support at 145.49, the Sep 17 low. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would signal scope for a climb towards key resistance at 150.92, Aug 1 high.

EUROZONE ISSUANCE: EGB Supply Daily

Germany is scheduled to hold an auction today, while Spain and France are both scheduled to hold auctions tomorrow. We pencil in issuance of E22.2bln for the week, around half of last week’s E43.3bln. We expect Ireland’s Q4 funding plan this morning (expecting 0-1 auctions).We received the Q4 funding plans from Finland (two bond auctions) and Portugal (auctions for the year completed).

- Germany will kick off Q4 issuance today with E5bln of the 10-year 2.60% Aug-35 Bund (ISIN: DE000BU2Z056) on offer.

- Spain will look to hold a Bono / Obli / ObliEi auction tomorrow. E4.5-5.5bln of nominals will be on offer including the on-the-run 2.70% Jan-30 Bono (ISIN: ES0000012O00) alongside the new long 7-year 3.00% Jan-33 Obli (ISIN: ES0000012P74) and the 1.00% Jul-42 Green Obli (ISIN: ES0000012J07). E250-750mln of the 1.15% Nov-36 Obli-Ei (ISIN: ES0000012O18) will also be on offer.

- France will conclude the week’s issuance tomorrow with a LT OAT auction. A first reopening of the 10-year 3.50% Nov-35 OAT (ISIN: FR0014012II5), the off-the-run 1.25% May-36 OAT (ISIN: FR0013154044), the 0.50% Jun-44 Green OAT (ISIN: FR0014002JM6) and the 4.00% Apr-60 OAT (ISIN: FR0010870956) will be on offer.