US DATA: Lack Of Momentum For New Residential Construction Activity

March housing starts/permits data were mixed, with the New Residential Construction report pointing in sum to the continuation of subdued activity.

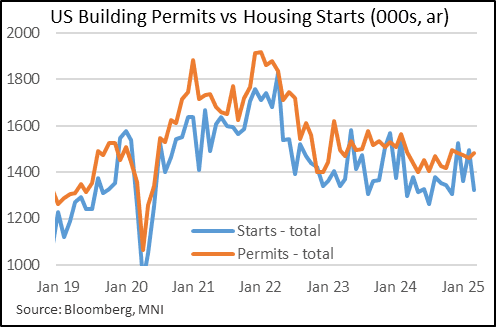

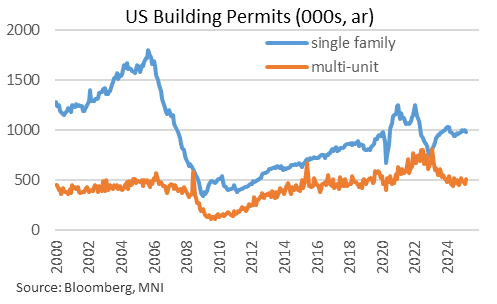

- March housing starts missed expectations by nearly 100k, at 1,324k(1,420k survey/1,494k prior, downward rev from 1,501k - all figures on a seasonally adjusted, annualized basis). Single family starts fell 14% to 940k (1,096k prior), the 2nd lowest figure in the last 2 years (multi-units dipped 3.5% to 384k).

- Building permits - a less volatile (and better leading) indicator of activity - told the opposite story across these categories: total permits rose to 1,482k, beating expectations (1,450k survey/1,459k prior rev from 1,456k), with multi-unit permits at a 4-month high 504k but single-family dipping to a 4-month low 978k.

- On a regional basis, there was a notable advance in permitting in the South, which accounts for over 50% of permits: they hit a 15-month high 830k, joined by a rebound in the West and Northeast but a reversal lower in the Midwest. As with other data, including industrial production and retail sales, there is some suggestion that better weather in the South may have played a factor in March activity.

- In short, residential construction activity continues to trend sideways, with little discernable improvement or deterioration since early 2023. The pickup in permits was somewhat encouraging but remain below levels that prevailed for much of 2022-23, let alone the heights of the pandemic reopening (see chart). The pullback in homebuilder sentiment (per NAHB data) remains a worrying sign for future construction as well.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Early Equities Roundup: Interactive Media, Discretionary Shares Lag

- Stocks trading lower Tuesday - reversing Monday's gains with major indexes back to late Friday levels ahead midday. Currently, the DJIA trades down 253.37 points (-0.61%) at 41585.29, S&P E-Minis down 65 points (-1.13%) at 5665.75, Nasdaq down 326.4 points (-1.8%) at 17477.72.

- Communication Services and Consumer Discretionary sectors underperformed in the first half, interactive media and entertainment stocks weighing on the former: Alphabet -4.65%, Meta Platforms -4.65%, Alphabet -4.53%, Netflix -3.06% and Live Nation Entertainment -1.71%.

- The Discretional sector weighed on by Tesla and cruise lines: Royal Caribbean Cruises -6.05%, Tesla -5.41%, Norwegian Cruise Line Holdings-4.29% and Carnival -3.64%.

- On the positive side, Real Estate and Energy sectors outperformed in the first half, investment trusts buoyed the former: Crown Castle +2.08%, Kimco Realty +1.78% and American Tower +1.47%. Meanwhile, oil and gas stocks supported the Energy sector: Coterra Energy +2.45%, EQT +2.09%, Marathon Petroleum +1.43% and Valero Energy +1.19%.

GERMANY: Fitch: Pressure On AAA Rating Could Arise Absent Growth Improvements

Fitch Ratings write that although “Germany has substantial fiscal headroom to accommodate the planned major shift to much larger military and infrastructure spending”, pressure on its AAA/Stable rating “could arise over the longer term if this spending increase is not eventually offset by consolidation measures or a lasting improvement in growth prospects”.

- The Bundestag vote on incoming Chacellor Merz’s fiscal reforms is currently ongoing, with the Bundesrat vote due on Friday March 21. Fitch expect the bill to be passed “broadly as envisaged”.

- Fitch pencil in “EUR900 billion-1 trillion (21%-23% of 2024 GDP) of additional government expenditure over the next decade”, with new spending expected to be scaled up gradually.

- “Under this assumption, Germany's debt-to-GDP ratio would approach 70% by 2027, the highest among ‘AAA’ rated peers (median at 36.5%), but still below the 80% peak of 2010. Germany's status as the eurozone’s benchmark issuer and its large, diversified economy also enhance its debt-carrying capacity”.

- “Our initial estimate is that the new spending could directly add on average about 0.4pp to GDP in 2025-2027, but we expect higher US tariffs to offset this in 2025 and forecast growth of just 0.1%”…. “However, fiscal stimulus will allow the German economy to recover modestly next year, when we forecast growth of 1.1%”.

- “Germany faces significant structural challenges, including rising competition from China, tariff risks due to its export-oriented economy, and competitiveness issues in the manufacturing sector caused by increased energy and labour costs, bureaucratic hurdles, and high corporate taxes”… “he additional spending will support growth and enhance competitiveness, but it is unlikely to substantially improve Germany's longer-term growth prospects in isolation”.

GERMANY: CORRECTION: Fiscal Bill Only Now Up For Vote, Results Around 15:00 GMT

The key German fiscal bill on higher military and infrastructure spending by CDU/CSU and SPD was only now up for vote in Bundestag, until 14:50 GMT. Vote collation took around 10 minutes for the last drafts, meaning results should be in around 15:00 GMT.

- The previous bill up for vote was a second one by pro-business FDP, which, as expected, failed to gain the required 2/3rds majority of votes.

- Threshold for passing sits at 489 votes in favour.