CANADA DATA: Labour Report Highlights Weakening Trends In Youth Employment (2/2)

The 6.91% (unrounded) unemployment rate in July marked only a slight uptick from 6.87% in June, and equal to the prior 3-months' average (6.91%), defying widespread expectations for a rise to 7.0%.

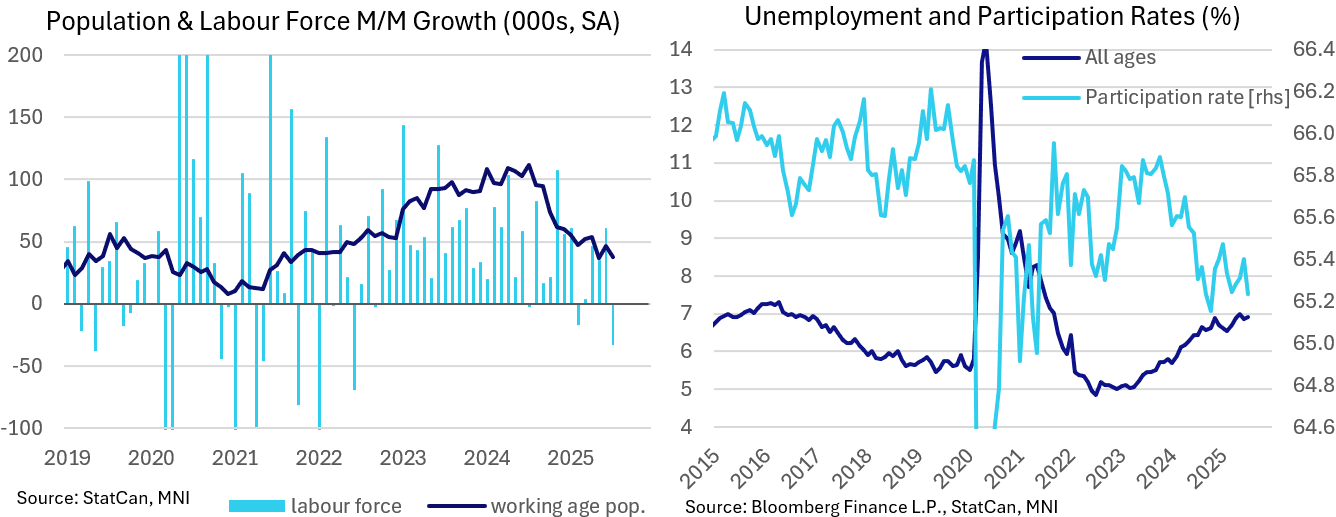

- Unpacking this surprising result: the participation rate fell to a 9-month low 65.23% (unrounded) from 65.40% prior - this had been expected to remain steady. That helps explain why despite the much-weaker-than-expected net employment change, the unemployment rate remained steady.

- The number of unemployed rose 7k, while the labour force fell by 33k (biggest drop since Jun 2022 and giving up over half of June's rise), amid a population rise of 38k (not out of the ordinary for 2025 but a continuation of a longer-term slowdown).

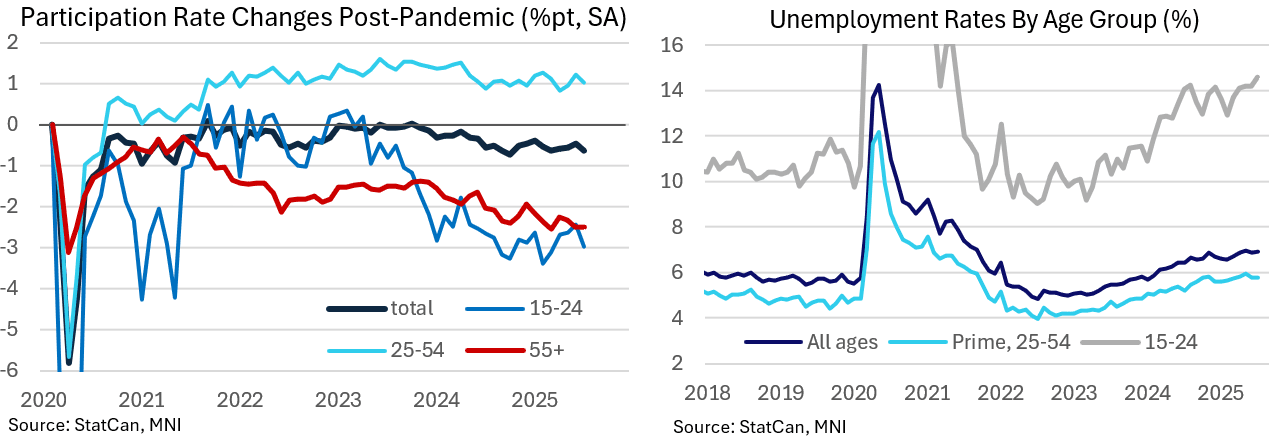

- And in turn, the rise in unemployment and the decline in the labor force is down largely to youth (15-24): employment dropped 33.7k (26-month worst) and their unemployment rate rose to a 50-month high 14.57% from 14.20%.

- The youth participation rate fell to a 4-month low 62.73% from 63.26%, with the labor force falling 25.4k (5-month worst).

- Contrast these with prime-age statistics: unemployment was basically steady (5.79% after 5.77%) and participation dipped less dramatically (88.42% after 88.60%). The prime labor force fell 14.4k and employment fell 16.3k, but these were less than one-quarter of June's gains.

- Total participation has been dipping over the last couple of years, led by declines in youth and 55+ participation - and offset by sustained gains in prime-age participation, so this is a continuation of a long-standing trend.

- The overall decline in the working age population since early 2024, which largely looks related to reduced immigration, has therefore resumed. Alongside a reduced participation rate, employment gains look to remain capped.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NORWAY: June Inflation Tomorrow, Swedish Print Adds Upside Risks

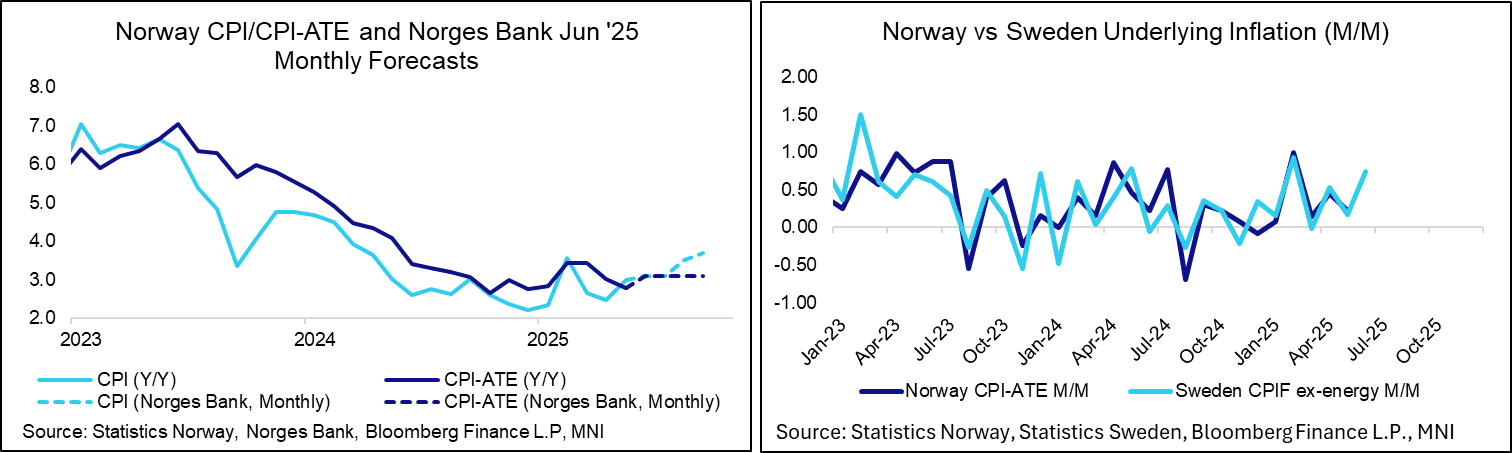

Norwegian June inflation is due tomorrow at 0700BST/0800CET. This will be the first inflation report since Norges Bank’s surprise 25bp cut on June 19. In an interview with the MNI Policy Team following the decision, Governor Wolden Bache indicated that Norges Bank opted to cut rates because it had gained confidence that the Q1 uptick in inflationary pressures was temporary. In this light, we think the base case should be that further cuts can be delivered in September and possibly December if CPI-ATE tracks in line with Norges Bank’s projections – provided economic activity momentum doesn’t accelerate unexpectedly. We continue to think that the bar to rate moves at interim decisions (August and November) is high, but NOK FX and rate markets will as usual be sensitive to large deviations from consensus.

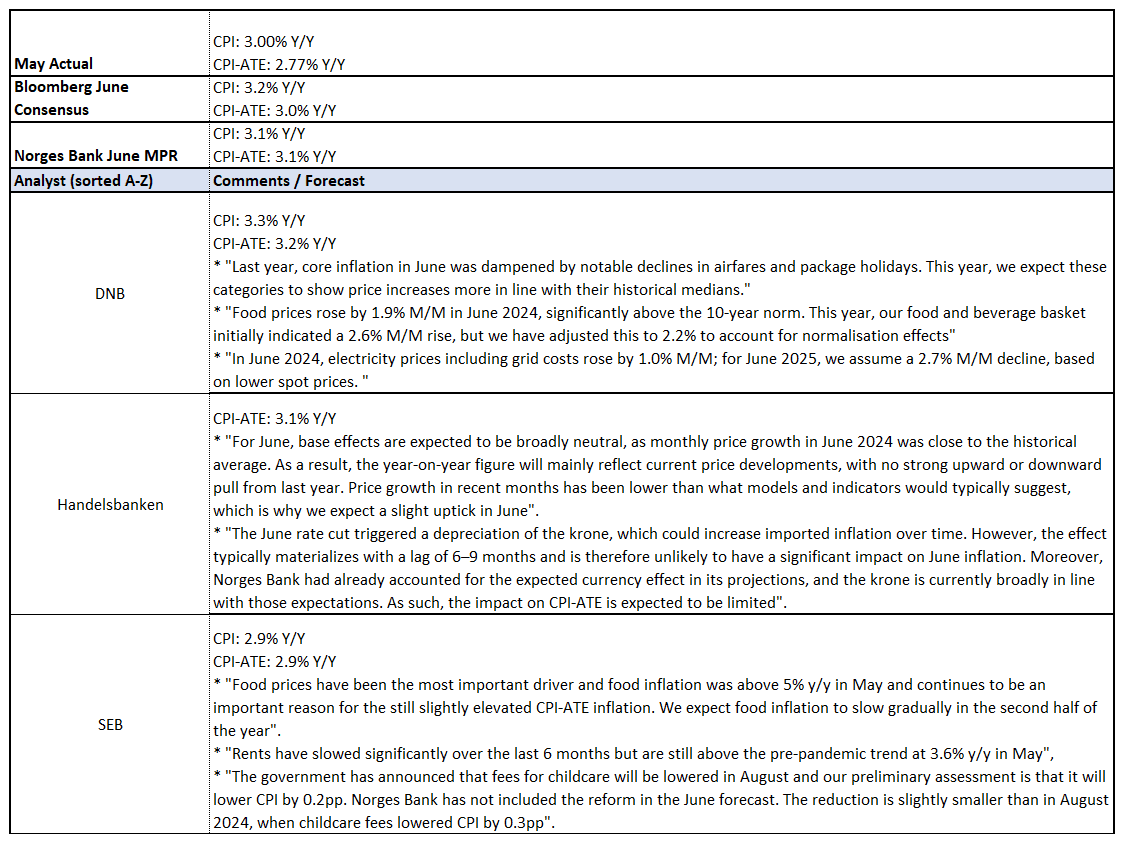

- In the June MPR, Norges Bank projected CPI-ATE inflation at 3.1% Y/Y in June through September (May: 2.77% Y/Y). For tomorrow’s print, the median analyst pencils in a 3.0% Y/Y reading.

- There could be upside risks to analyst and Norges Bank projections after Monday’s Swedish flash June inflation report (3.3% Y/Y vs 2.9% cons, 2.5% prior). Since 2015, there has been a 0.56 correlation between M/M NSA Norwegian CPI-ATE inflation and Swedish CPIF ex-energy inflation. Since 2023, this correlation has risen to 0.69. The chart below also indicates a close relationship between the two inflation rates since February. Clearly, this is a crude and non-causal observation, but still worth keeping in mind.

- Swedish CPIF ex-energy was 0.74% M/M in June. If realised in Norway, this would imply an annual rate of 3.3% Y/Y – comfortably above expectations.

- Norges Bank projects headline CPI inflation at 3.1% Y/Y (vs 3.00% prior), while analysts see 3.2% Y/Y.

- See below for a selection of analyst comments:

BONDS: FF Flow & Downtick In Oil Support

A move lower in crude oil and the previously covered buying FFQ5 futures helps underpin wider core global FI markets, allowing TY futures to trade from fresh session lows to fresh session highs in a ~50-minute window. TY still operates in a narrow 0-06+ range.

- Light demand in gilt and bund futures on spill over from the move in Tsys.

- U.S. and German yields little changed to ~1.5bp lower on the day, while the gilt curve still twist flattens, with yields +1.5bp to -2.5bp.

US-EU: Sefcovic To MEPs: Hope For Satisfactory Result On Trade In Coming Days

European Trade Commissioner Maros Sefcovic has just finished updating the European Parliament on the state of talks with the US intended to mitigate the impact of tariffs on EU-US trade. Sefcovic says that "Our priority is a negotiated solution with the US", and that trade talks "continue remotely every day." Claims that the two sides have "made good progress on the text of an agreement in principle" and that he "hopes to achieve a satisfactory result in the coming days." Acknowledges that even with a skeleton deal, "a degree of rebalancing" will be needed in future transatlantic trade.

- Sefcovic: "Our regulatory framework remains non-negotiable." Says that the EU's trade diversification agenda is a priority, which the Commission is also working to "protect the EU from trade diversion from other countries."

- The Commissioner says that EU unity is "crucial". This unity may prove hard to come by, with countries such as Germany and Italy advocating for a swift deal, little matter of the content, while others, such as France and Spain, support a more robust stance that could imperil an agreement being reached by 1 August.

- Speaking on 8 July, US President Donald Trump said, “the European Union has been speaking to us, Ursula and the whole group, and they have been very nice.” Says that the EU “treated us very badly until recently,” claiming the Union has been “in many respects much worse than China," before adding "Now they are being very nice to us and we will see what happens."