ASIA FX: KRW Has Scope To Rally More, As Risk Sentiment Bounces

In North East Asia FX, the USD has lost ground amid better risk appetite in the equity space. The US Senate voting on a procedural bill (60-40 votes), to start the process to end the government shutdown has aided equity risk sentiment. US equity futures are up strongly, led by the tech side. In Asia, the Kospi has surged over 3%, but China markets have been laggards.

- The better risk on tone has helped KRW outperform. USD/KRW was last near 1452/53 up around 0.60% in won terms. Still, this only pares Nov to date underperformance ( still off 1.5% despite today's rally). After last week's more than $5bn in offshore outflows (the most since 2021), the focus will be on whether such trends stabilize. So far today, offshore investors haven't returned though. USDKRW also remains well above 20-day EMA support (near 1430), so even with further downside, won bulls might not get excited until we breach such support levels.

- USD/CNH is drifting lower, but still above 7.1200 at this stage. The USD/CNY fix edged up, but the fixing error remain wide, pointing to on-going yuan resilience. A downside test under 7.1200 should bring the 7.1000 region back into focus, but it is likely to be a steady grind rather than a dramatic move lower in the pair. CNH/JPY upside is back in focus with the better risk tone. We were last 21.6200, with late Oct highs around 21.70 targeted on the upside.

- The supportive macro backdrop, coupled with overbought technicals, suggests USD/TWD may lose some upside momentum. Oct export data from the end of last week showed surging export growth on the back of the AI/chip boom. If we see equity inflows return it may aid downside in the pair (note the 200-day EMA is around 30.83, against current spot just under 31.00).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Oval Office Announcement Underway Shortly

US President Donald Trump is shortly due to deliver an announcement in the White House Oval Office. LIVESTREAM The announcement is expected to relate to drug pricing and could follow a similar template to a recent pledge from Pfizer.

- The announcement will be Trump's first press remarks since a market-moving Truth Social statement earlier today in which Trump suggested calling off a meeting with Chinese President Xi Jinping and raising tariffs on China in response to new export controls from Beijing on rare earths. See earlier bullets here and here.

RATINGS: Moody's Completes Periodic Review Of Belgium, No Rating Action

No ratings actions for Belgium from Moody's, which is quoted in a press release on Bloomberg: "Moody's Ratings (Moody's) has completed a periodic review of the ratings of Belgium and other ratings that are associated with this issuer. The review was conducted through a rating committee held on 2 October 2025 in which we reassessed the appropriateness of the ratings in the context of the relevant principal methodology(ies), and recent developments. This publication does not announce a credit rating action and is not an indication of whether or not a credit rating action is likely in the near future."

- There had been some speculation there could be a ratings action - MNI wrote Thursday: "* Moody's on Belgium (Current rating Aa3, Outlook Negative): We expect Moody's to maintain their current stance in the absence of 2026 budget details."

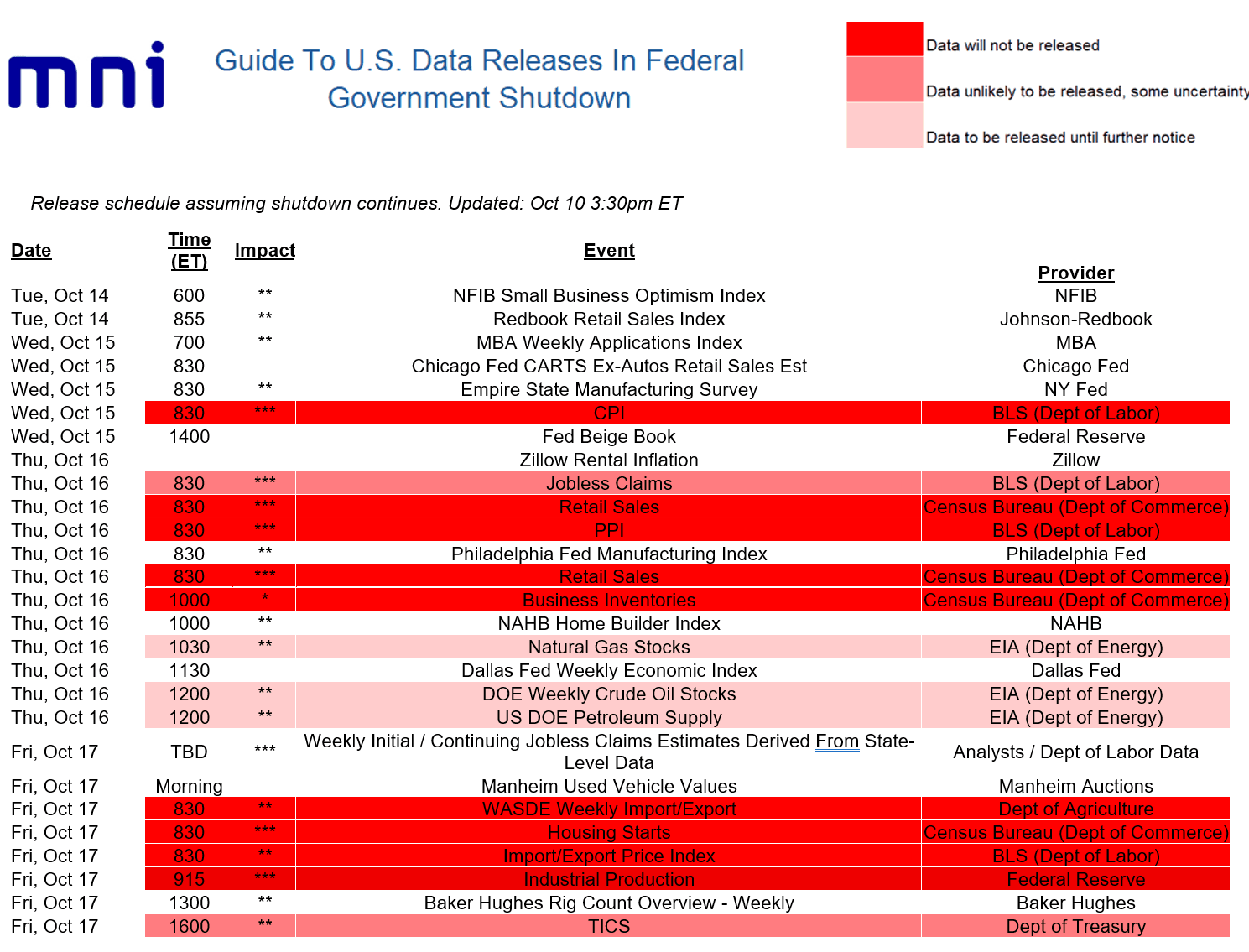

MACRO ANALYSIS: US Macro Week Ahead: No CPI, But Plenty Of Pre-Blackout FedSpeak

Below is the week’s data schedule, with MNI’s annotation of whether or not data will be postponed.

- As we went to press, the Fed announced that next week's Industrial Production data will be postponed (was due to be published next Friday Oct 17) as the data “incorporate a range of data from other government agencies, the publication of which has been delayed as a result of the federal government shutdown.”

- We won’t be getting September CPI as scheduled on Oct 15, but at least the BLS announced it will publish the data on Oct 24.

- As such next week we’ll be looking at some under-covered data points, including the Redbook weekly and Chicago Fed’s CARTS retail sales data (in lieu of the Census Bureau retail sales report), with a little more focus than usual on regional Fed manufacturing indices (NY, Philadelphia).

- Once again, the dearth of tier-one data leaves Fed commentary in focus ahead of the pre-FOMC blackout period: highlights for us are Philadelphia Fed President Paulson making her first comments on monetary policy on Monday since being appointed in the summer, while as always Chair Powell bears watching on Tuesday (we also hear from Bowman, Waller, Collins, Miran, Schmid, and Musalem).

- Additionally we get the latest Beige Book which was already key given the FOMC was already increasingly focused on anecdotal information as it attempts to navigate murky economic waters.