OIL: KPC Offers Additional Heavy Crude After Al-Zour Refinery Outage

Oct-31 09:26

Kuwait Petroleum Corp has offered additional heavy crude for prompt loading in November following an unplanned Al-Zour refinery outage last week, Reuters sources said.

- KPC offered 800kbbl of Kuwait Heavy Crude for Nov 15-16 loading and 500kbbl Eocene scheduled to load on Nov 18-19.

- The tender closed on Thursday although it is not known if it has been awarded.

- The total volume of heavy crude offered so far is 2.9mbbl after two cargoes were sold last week.

- On Oct. 21, Kuwait Integrated Petroleum Industries Company shut down parts of its 615k b/d Al-Zour refinery due to a fire.

- The refinery was running at about one-third of its capacity with only one of three crude processing units operating, sources told Bloomberg on Oct. 28.

- All units are tentatively expected to restart by Nov. 7, according to IIR.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

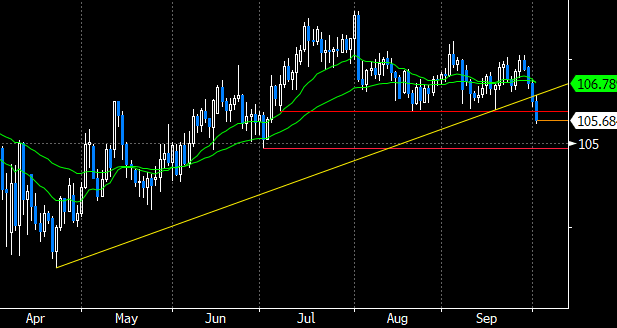

FOREX: GBPJPY Extends Below 50-Day EMA, CADJPY Slips to 3-Month Lows

Oct-01 09:19

- The general risk off tone on Wednesday is providing a safe haven bid to the Japanese yen, adding to the themes touched upon in the above post. This has prompted some notable declines for Cross/JPY, with CADJPY (shown below) breaking through a cluster of lows around 106.00 and slipping to a fresh three-month low.

- Bearish developments have been bolstered by a trendline break from the April lows, and price action signals scope for an initial move to 104.85, the July 01 low. Canada employment data is not due until next Friday.

- We had been highlighting GBPJPY as a potentially vulnerable candidate to further yen demand, and the significance of the 50-day EMA. The cross broke below the average, which intersects at 198.98, and the next downside target would be 195.04, the August low.

- AUDJPY had been in a strong uptrend, however, the most recent turn lower has seen the cross dip back to an area of support around 97.25, notably breaching the 20-day EMA which has been supportive in recent weeks.

- In similar vein, EURJPY bullish momentum stalled above 175 having traded to within 30 pips of the 2024 highs at 175.43. Spot now trades back below 173, having pierced the 20-day EMA. Support to watch lies at 172.46, the 50-day EMA.

Source: Bloomberg Finance L.P. / MNI

EUROPEAN INFLATION: HICP broadly in line with consensus: The breakdown

Oct-01 09:08

- Eurozone HICP came in at a little below the MNI tracking of 2.3% with 2-way risks at 2.23%Y/Y, but broadly in line with the market consensus.

- Core and services both rounded down to consensus expectations, although core at 2.35%Y/Y was almost 2.4%.

- It appears as though FAT (food, alcohol and tobacco) is the only notably surprise, coming in softer than expected at 3.04%Y/Y (down from 3.19%Y/Y where it was expected to remain).

- No substantial market reaction, given that the data was broadly in line with expectations.

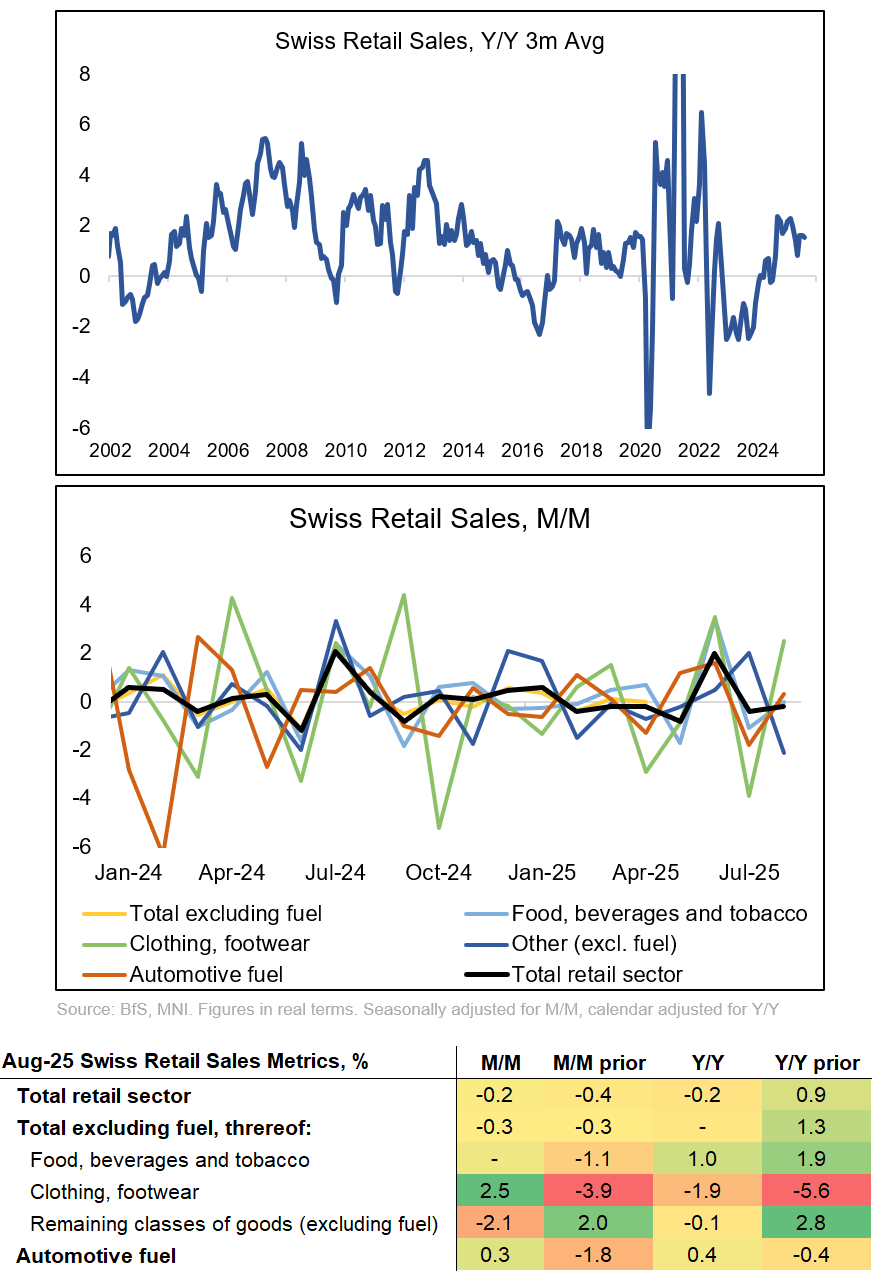

SWITZERLAND DATA: August Retail Sales Weak But Broader Picture Solid So Far

Oct-01 09:06

Swiss (real) retail sales were rather weak in August on a sequential comparison, at -0.2% M/M.

- Looking at the drivers of the release shows that weakness was centred in the "remaining" category (which contains a lot of durable goods, table below). The August data was the first incorporating the 39% US tariffs levied on Swiss goods. The question is if this filtered through to consumer scepticism here already.

- However, on a broader 3-month moving average of the Y/Y measure, Swiss retail sales continue to grow around their long term average rate, at a current 1.5% (1.6% July).

- This means the big picture is that the Swiss consumer overall continues to screen healthy. However, we watch for potential signs of a cooling of the propensity to consume going forward.