ASIA STOCKS: Korea Has First Inflow of Month

A period of significant outflows for Korea halted briefly with a meaningful inflow yesterday as other countries’ flows remain mixed.

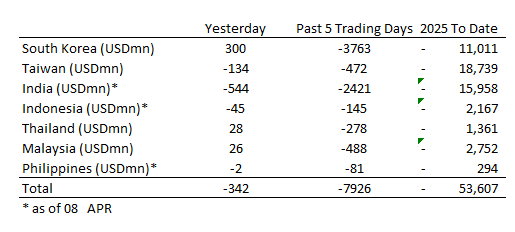

- South Korea: Recorded inflows of +$300m as of yesterday, bringing the 5-day total to -$3,763m. 2025 to date flows are -$11,011, m. The 5-day average is -$753m, the 20-day average is -$276m and the 100-day average of -$152m.

- Taiwan: Had outflows of -$134m as of yesterday, with total outflows of -$472m over the past 5 days. YTD flows are negative at -$18,739. The 5-day average is -$94m, the 20-day average of -$335m and the 100-day average of -$253m.

- India: Had outflows of -$544m as of the 8th, with total outflows of -$2,421m over the past 5 days. YTD flows are negative -$15,958m. The 5-day average is -$484m, the 20-day average of -$36m and the 100-day average of -$149m.

- Indonesia: Had outflows of -$45m as of yesterday, with total inflows of -$145m over the prior five days. YTD flows are negative -$2,167m. The 5-day average is -$29m, the 20-day average -$43m and the 100-day average -$35m

- Thailand: Recorded inflows of +$28m yesterday, outflows totaling -$278m over the past 5 days. YTD flows are negative at -$1,361m. The 5-day average is -$56m, the 20-day average of -$24m the 100-day average of -$19m.

- Malaysia: Recorded inflows of +$26m as of yesterday, totaling -$488m over the past 5 days. YTD flows are negative at -$2,752m. The 5-day average is -$98m, the 20-day average of -$64m the 100-day average of -$40m.

- Philippines: Saw outflows of -$2m as of yesterday, with net outflows of -$81m over the past 5 days. YTD flows are negative at -$294m. The 5-day average is -$16m, the 20-day average of -$3m the 100-day average of -$6m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Bullion In Tight Range Ahead Of US CPI

Gold prices are little changed during APAC trading rising moderately to $2916.5/oz, close to March’s high of $2930.31. It is up 2.1% this month benefiting from flight-to-quality flows driven by increased global uncertainty. Risk appetite improved following the US taking a step back from an escalation of the US-Canada trade war and Ukraine agreeing to a US ceasefire proposal. This drove bullion down to $2910.96 early in today’s session but it has now recovered. Markets are waiting for US February CPI data out later.

- Slightly lower US Treasury yields have provided support for gold’s recovery today but the 0.2% rise in the USD index is capping gains.

- The US 30-day ceasefire proposal will now be presented to Russia following Ukraine’s readiness to agree to it but Russia has said that it will only approve it on its own terms and not the US’. A refusal would likely result in further quality flows into bullion.

- Gold’s trend condition remains bullish and recent moves appear corrective. Initial support is at $2880.3, 10 March low, while resistance is at $2930.3, 7 March high. The bull trigger is at $2956.2.

- US CPI for February is out later (see MNI CPI Preview) and forecast to show a 0.1pp moderation in headline and core to 2.9% y/y and 3.2% y/y respectively. An undershoot is likely to increase Fed easing expectations and buoy gold prices. February budget and real earnings data are also released.

- The BoC decision is announced and it is forecast to cut rates 25bp. The ECB’s Lagarde and Lane speak at the “ECB and Its Watchers” conference.

BONDS: NZGBS: Closed With A Bear-Steepener, US CPI Due Later Today

NZGBs closed showing a bear-steepener, with benchmark yields 5-7bps higher. That said, yields finished away from their worst levels, with US tsys partially retracing some of yesterday’s weakness.

- Cash US bonds are ~1bp richer in today’s Asia-Pac session. The February CPI report is the highlight of today’s US session, while some attention will be paid later in the morning to the Bank of Canada which is expected to deliver a 25bp cut.

- NZ-US and NZ-AU 10-year yield differentials closed little changed.

- The AFR revealed that RBNZ Orr’s resignation was tied to him refusing to pull back from imposing one of the world’s heaviest capital burdens on the big four Aussie banks, which dominate the Kiwi banking system.

- Swap rates closed 4-7bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed flat to 4bps firmer across meetings. 25bps of easing is priced for April, with a cumulative 74bps by November 2025.

- Tomorrow, the local calendar will see Net Migration data.

- The NZ Treasury also plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$200mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

JGBS AUCTION: Mixed Demand Metrics For 20Y Auction

The 20-year JGB auction delivered mixed results across key metrics. The low price underperformed dealer forecasts, which were set at 96.10 according to a Bloomberg poll. However, the cover ratio increased to 3.4594x from 3.0557x in the previous auction and the auction tail shortened dramatically to 0.20 from 0.55.

- As noted in the auction preview, today’s offering featured an outright yield at a cycle high, 25-30bps higher than last month’s auction.

- Moreover, the 10/20 yield curve was dramatically steeper after bouncing off its lowest point since mid-2023.

- Additionally, the 20-year JGB had cheapened from its most expensive valuation within the 10/20/30 butterfly since late 2022.

- This result was aligned with the mixed performances observed in the 30-year JGB auction earlier this month.

- Post-auction, the 20-year JGB is little changed.