EM ASIA CREDIT: JD.com: Q3 results disappoint.

(JD, A3/A-pos/NR)

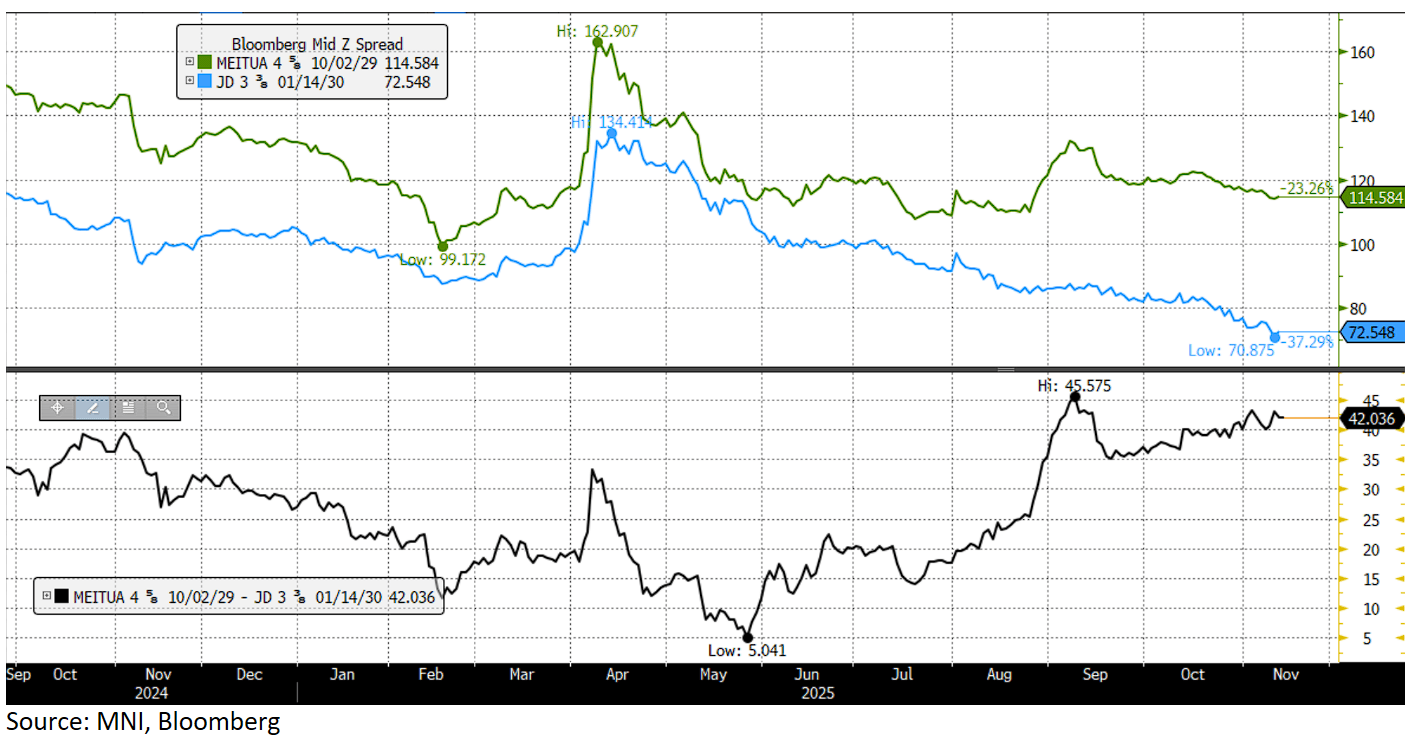

JD.com reported its 3Q results after market close with EBITDA down 84% YoY to RMB2.5bn, and materially below consensus (RMB3.4bn). Negative for spreads.

The JD Retail segment (84% of revenues) solid numbers, operating profits +28% YoY to RMB14.8bn and margin up from 5.2% to 5.9%, were not enough to offset declines in JD Logistics (-38% YoY) and material operating losses at New Business (RMB15.8bn loss), which include JD Food. In terms of credit, liquidity continued to be drained away, with reported free cash flows negative RMB11.2bn in the quarter, which drove the net cash position down to RMB4.5bn versus RMB15.8 at end Q2 and versus RMB18.1bn end FY24.

In terms of valuations, we note that the z-spread differential between the JD.com USD 30s and the Meituan USD 29s is close to the wides. The two issuers started to diverge post 2Q results when Meituan reported weak results on the back of the food delivery business price war. Meituan will report its 3Q results on the 19th November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: New Zealand AA+ Rating Affirmed By S&P

Headlines have crossed from S&P that it has affirmed NZ's credit rating at AA+, with the outlook remaining stable. The rating agency noted, via BBG: "S&P sees New Zealand to gradually consolidate its fiscal deficit over the next three years."

- S&P noted the economic challenges from a growth standpoint NZ has face in recent years, but also commented on the structural improvement in the current account position.

- NZ Finance Minister Willis stated recently a return to surplus was still the government's goal (by 2028) and that fresh fiscal spending/stimulus is not needed for the economy (despite current headwinds).

JPY: USD/JPY Under Fri Lows As US 10yr Eyes 4.00% Test, Key EMAs Under 150.00

USD/JPY is continuing to track lower, now under 151.15, up 0.50% in yen terms. This puts us under Friday lows in the pair, but we are still comfortably above key EMAs.

- Focus in the near term may rest on the softer US Tsy yield backdrop. The 10yr at 4.01% is close to recent lows, with eyes on whether we can break under the 4.00% handle. As we noted earlier USD/JPY looks too high relative to yield momentum between US-JP. The USD/CNY fix under 7.1000 has been another positive, while other cross asset trends have been mixed. Gold continues to rally, signifying some safe haven flows are still on-going, but the regional equity mood looks better.

- JPY is outperforming so far in the G10 space, although AUD isn't too far behind, up 0.30% (with similar benefits from the CNY fixing outcome).

- For USD/JPY we are now under late Friday highs, while other support points to note are outlined below. We are still some distance from the 50-day EMA.

- SUP 1: 150.92 High Sep 26

- SUP 2: 149.72 20-day EMA

- SUP 3: 148.50 50-day EMA.

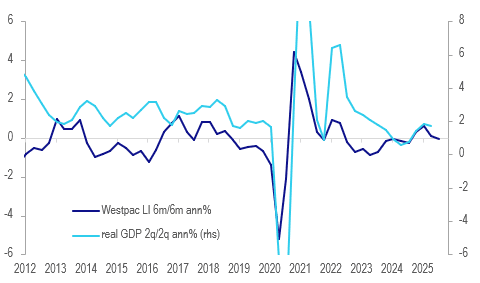

AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth

The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months. This measure leads detrended growth by 3 to 9 months and signals that growth may slow in H2 but be around trend early in 2026. Westpac is forecasting 2% growth in 2025 with it improving in 2026.

- Westpac forecast a 25bp rate cut at the November meeting but now believes that while the next move in rates is down, the upcoming decision will rely on Q3 CPI on 29 October. It notes though that its lead indicator signals GDP growth remains lacklustre.

- The indicator was stronger in H1 this year with the H2 moderation driven by dwelling approvals and AUD commodity prices. Westpac expects both of these components to turn with the latter already higher driven by gold and lower rates and policy likely to boost housing supply.

- Equity prices have been positive for the lead indicator over the last 6 months.

Australia Westpac lead indicator vs GDP %