NATGAS: Iraqi Oil Ministry Ready to Help Repair Khor Mor Gas Field After Attack

Iraqi oil ministry is ready to help the Kurdistan Regional Government repair the damages at the Khor Mor gas field following the latest drone attack, Rudaw said.

- Security forces are still working to determine the origin and nature of the attack, Kurdistan Region Natural Resources Minister Kamal Mohammed said.

- A rocket attack struck a liquid storage tank at the Khor Mor facility in the Kurdistan region of Iraq late on Wednesday, Dana Gas has announced.

- Production has been shutdown to extinguish the fire and conduct a situation assessment, Dana Gas said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: OCT STORE SALES +5.4% V YR AGO MO

- MNI: US REDBOOK: OCT STORE SALES +5.4% V YR AGO MO

- US REDBOOK: STORE SALES +5.2% WK ENDED OCT 25 V YR AGO WK

GBP: Weakness Stems From Fiscal Pressures and Downside Risks to Inflation Exp.

GBPUSD has shown below the earlier pullback lows of 1.3301, extending the day's spell of weakness to challenge Friday's 1.3288, and keeping GBP as the poorest performing currency in G10. Move comes despite few fresh headlines across the morning - in contrast with the busier Monday session for Budget speculation. That said, there are a few key fundamental drivers pressing GBP:

- As noted a few times this morning - speculation that Reeves will break a manifesto pledge and raise income tax has been bolstered by the FT's reporting on a sizeable productivity estimate cut triggering a broader financing need.

- Higher income taxes would contain consumption, helping smooth the path for faster BoE rate cuts across 2026 (and potentially by the end of 2025).

- Food inflation remains a key driver of inflation expectations (e.g. Just this week: The Times: '‘Shrinkflation’ of supermarket staples rife on British high streets', BBC: 'Businesses face 'rising costs and staffing pressures''), however today's BRC-NIQ shop price data suggests we have passed the peak in food price gains.

- Food price inflation is particularly important given how well supported it has been this year via both higher employer's NIC contributions as well as incoming packaging taxes, but today's numbers endorse the step lower in ONS food inflation and may suggest inflation expectations will follow.

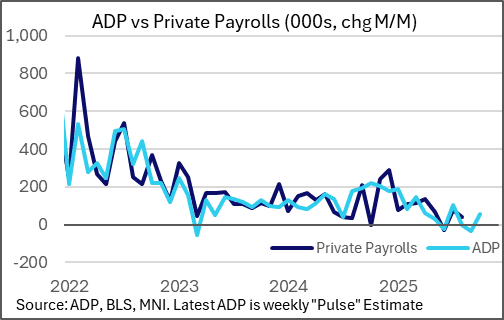

US DATA: ADP Initiates Data Showing +57k 4-Week Private Payrolls Through Oct 11

ADP announced Tuesday it would release weekly preliminary estimates of private sector employment, with the first reading showing an average weekly rise in payrolls of 14,250 in the 4 week period ending Oct 11, 2025.

- This initial National Employment Report "Pulse" report (as ADP calls it) as suggesting 57k private payroll gains over the course of the month, though the underlying data was not made available. This data is being released on a 2-week lag.

- If carried through the full month it would mark an improvement from -32k in September, though that figure was impacted by a rebenchmarking that reduced the total by 43k - making the "underlying" growth around 11k.

- So 57k would be a solid figure by recent standards (and best since July) especially if it translates into the eventually-released October nonfarm payrolls data.

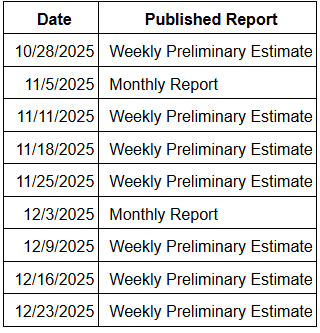

- The period for the 4-week estimate comes just before the nonfarm payrolls reference period for October. The ADP's practice of publishing a monthly report published on the Wednesday before the BLS Employment Report will continue (the next one will be Nov 5, with or without nonfarm payrolls to follow on Nov 7). The schedule is below; more from ADP here.

- The ADP had apparently been compiling this data for some time, with the Fed having had access to it since at least 2018 per the Wall Street Journal - however various reports this month suggested the ADP had stopped providing the data to the Fed. Now, it's available to everyone, and looks to be a fixture on the data calendar even beyond the resolution of the government shutdown.