JAPAN DATA: IP Beats Forecasts But Government Cautious On Outlook

Japan Sep (preliminary) industrial production was stronger than forecast. We were up 2.2%m/m, versus a 1.5% forecast and 1.5% fall in Aug). The y/y outcome was 3.4% against a 1.8% forecast and -1.6% Aug outcome. The y/y outcome is just short of mid year highs, but the authorities are not confident this is start of a resurgent trend. A government official noted after the print, that they still can't be optimistic about the production situation and it needs close monitoring (via RTRS).

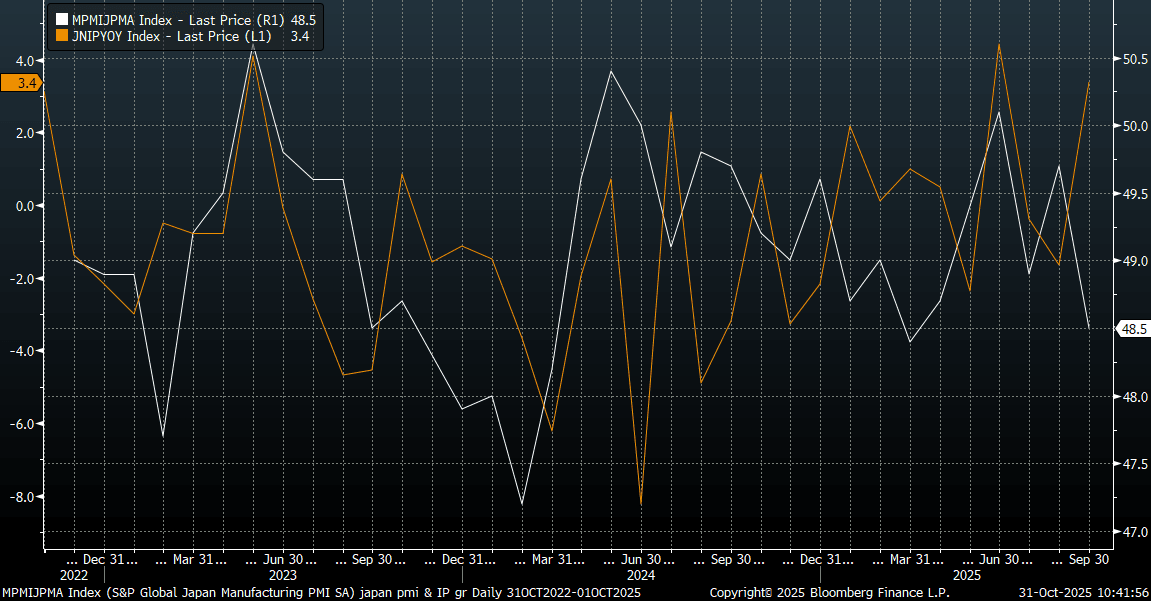

- The chart below shows IP growth Y/Y (the orange line) versus the Japan manufacturing PMI (white line), with the PMI painting a softer backdrop relative to IP.

- Our policy team noted, the Sep result was led by higher output of production machinery, though automobile production growth slowed. It adds, assuming flat output in December, industrial production would contract 0.1% q/q in Q4, marking a second consecutive quarterly decline following a 0.1% drop in Q3. This assumes METIs forecast of a 1.9%m/m Oct rise, but Nov fall of 0.9% unfolds.

Fig 1: Japan IP Y/Y & Manufacturing PMI

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Crosses - AUD Continues To Outperform, Reaching Levels To Pare Back ?

US equities continued to grind back towards its all-time highs brushing off concerns of an imminent US shutdown overnight. This morning US futures have opened lower on our open as the shutdown begins to be executed, E-minis(S&P) -0.35%, NQZ5 -0.45%. The AUD looks to be rebuilding momentum higher in the crosses after a period of consolidation.

- EUR/AUD - Overnight range 1.7714 - 1.7849, Asia is currently trading around 1.7765. The pair topped out after multiple failures to extend above 1.7900. Price is still in the middle of its recent 1.7600 -1.8100 range having failed to extend lower after moving below 1.7750 overnight. Expect sellers to fade bounces while price remains below 1.8000.

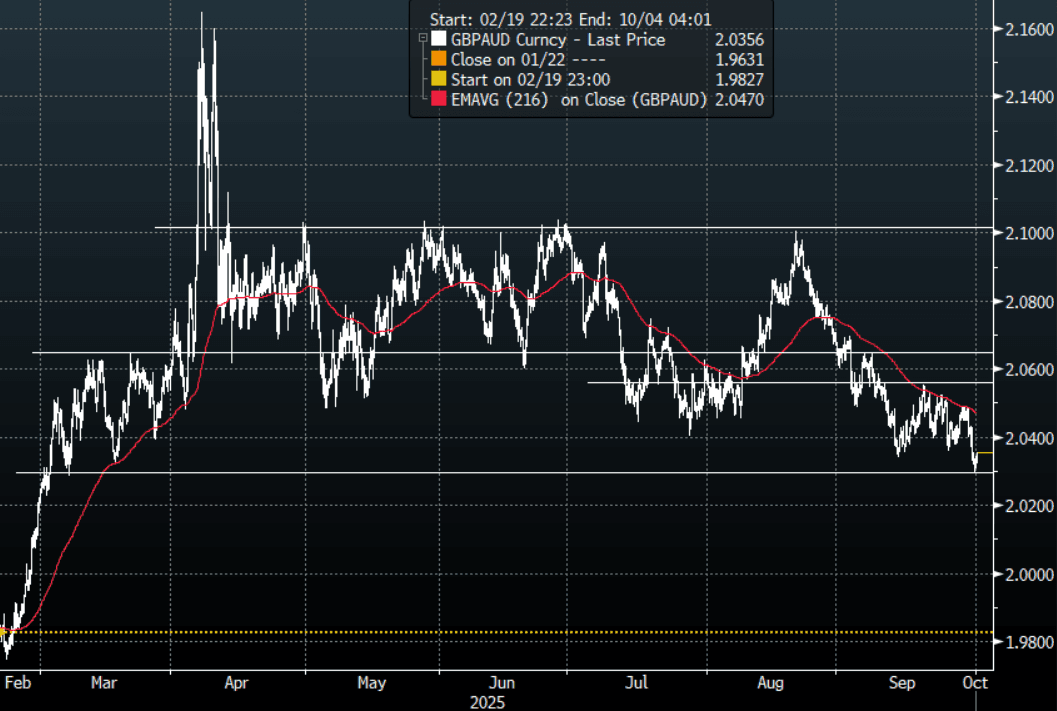

- GBP/AUD - Overnight range 2.0293 - 2.0428, Asia is trading around 2.0350. The pair has seen supply return on every look above 2.0500, the move lower has stalled back toward its support around 2.0300 where we should initially see some demand return, risk/reward looks a decent long first up. The price action of the pair is looking potentially exhaustive but a sustained break sub 2.0300 is needed to open up a deeper pullback towards 1.9800/2.0000.

- AUD/JPY - Overnight range 97.43 - 97.98, Asia is trading around 97.80. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

- AUD/NZD - Overnight range 1.1359 - 1.1418, the cross is dealing in Asia around 1.1400. The Cross has broken above the multiple highs around the 1.1200 area and has accelerated up towards 1.1400. I would think this 1.1400/1.1500 area would initially be met with sellers and expect some work to be done up here before another extension higher.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: AUCTION PREVIEW: ACGB Dec-34 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 3.50% 21 December 2034 bond, issue #TB168. The line was last sold on 25 June 2025 for A$1000bn. The last sale drew an average yield of 4.0895%, at a high yield of 4.0925% and was covered 3.1708x. There were 35 bidders, 18 of which were successful and 11 were allocated in full. The amount allotted at the highest yield as a percentage of the amount bid at that yield was 12.2%.

- This week's ACGB supply will be at the top end of the recent weekly issuance range of $1500-2200mn, with A$1000mn of 1.25% 21 May 2032 to be issued on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

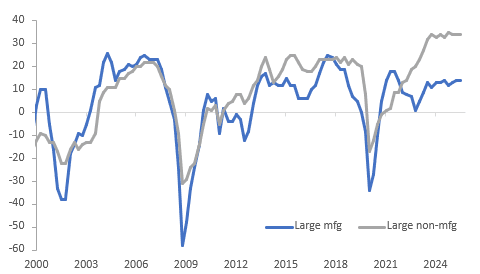

JAPAN DATA: Tankan Steady, Capex Intentions Higher

The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector. USDJPY is higher on the data rising to 148.15 up from 147.82 before the data and equities are lower. Respondents see USDJPY around 145.68 in FY25.

- The large manufacturers’ index rose 1 point to 14 in Q3 while the outlook for Q4 is forecast to deteriorate 2 points. The series has not been affected by new US tariffs and the 2025 average is slightly higher than 2024’s.

- Non-manufacturers’ conditions were steady at 34, well above the series average of +7.3, with the outlook at 28.

- Small non-manufacturers are also outperforming manufacturers with the index at 14 (down 1 point) compared to +1 (stable). The outlook for both sectors improved 1 point.

- The September BoJ summary of opinions showed a bias towards a resumption of tightening.

Japan Tankan - large enterprises business conditions

Source: MNI - Market News/LSEG