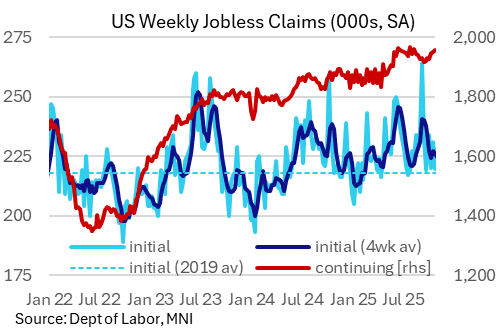

US DATA: Initial Jobless Claims Hold Steady In Latest Week

Initial jobless claims fell to an estimated 227k in the week of Nov 8, basically steady from 228k the week prior, per MNI's aggregation and seasonal adjustment of state-level data.

- While this didn't reverse the prior week's 8k rise, initial claims overall remain in a relatively steady range below 240k for 20 of the last 21 weeks (with the one exception being the first week of September which looks exaggerated by fraudulent claims in Texas).

- Overall the series remains indicative of a "low firing" labor market. The 4-week moving average is 226k, and has now printed 224-227k in the last 6 weeks.

- The rise in the NSA figure to 237k from 215k prior (data for Massachusetts and Tennessee were not available for the latest week so we use an estimate) is typical for this week of the year.

- Re the government shutdown: Washington DC-area (Maryland, Virginia, and the District of Columbia) claims have been relatively steady over the last 4 weeks, having picked up in the usual seasonal rise in the Oct 11 week.

- Note that this is almost certainly the last week in which we don't get an official Department of Labor estimate for national claims, with the end of the federal government shutdown almost certain to initial claims for the Nov 15 week released next Thursday (along with a back-fill of the 7 weeks that have gone without an official figure).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Yield Downtrend Persists, 10yr Close To 4.00%, Multi Year Lows

Early Wednesday trade is seeing NZGB yields track lower, led marginally by the back end. We are 3-4bps weaker across the benchmarks. This keeps downtrends in place. The 2yr bond testing under 2.60%, while the 10yr is under 4.05%. The 10yr benchmark has spent little time sub 4.00% since 2023. These moves are outperforming more modest US Tsy yield losses seen from Tuesday.

- The NZ-US 10yr spread looks to be biased lower, back near flat and just up from recent lows. 2025 lows rested just under -20bps for this spread.

- The 2yr swap rate is under 2.35%, also maintaining a firm downtrend. For RBNZ pricing, we have another 25bps easing close to fully priced for the Nov meeting. The terminal rate is around 2.12% for July next year, so roughly another 50% chance of another 25bps cut priced in.

- Focus will be on next Monday's Q3 CPI print around further easing risks (i.e. market pricing shifting to 2.00% for 2026 or gravitating back towards 2.25% as the terminal rate).

- Before that we get Sep food prices data tomorrow.

- The RBNZ has released its monetary policy decision dates for August 2026 to Feb 2027. The central bank has reduced the window between the end 2026 meeting (Dec 9) and first 2027 meeting (Feb 17). There had been criticism the dates between the end of year meeting and the first meeting of the new year was too long. The RBNZ noted it will still hold 7 policy meetings per year.

AUSSIE 3-YEAR TECHS: (Z5) Strong Start to Week

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.685 - 1.000 proj of the Sep 3 - 12 - 15 price swing

- RES 1: 96.615 - High Sep 12

- PRICE: 96.505 @ 16:24 BST Oct 14

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Aussie 3-yr futures surged on the resumption of trade after the weekend, returning focus higher after the break of support last week. While prices appear more stable, the recent break of Sep 3 low of 96.435 negates the recent short-term bullish theme. This breach signals scope for an extension towards 96.280, the May 15 low on the continuation chart. The short-term resistance to watch is 96.615, the Sep 12 high. Clearance of this level is required to reinstate a bullish theme.

JPY: USD/JPY Bullish Set Up Remains, Takaichi Seeking Meeting With Oppo Parties

USD/JPY tracks under 152.00 in early Wednesday dealings, after posting a modest gain for Tuesday's session. Bullish technical conditions persist, with the recent correction lower considered corrective for now. The next important support lies at 149.72, the 20-day EMA. On the upside, clearance of last Friday’s 153.27 high, would resume the uptrend and open 154.39, a Fibonacci retracement point.

- This backdrop didn't shift as Tuesday's session unfolded, with focus elsewhere, as EUR recovered some ground, while AUD/USD moved up from lows as the USTR said US-China talks were still continuing. AUD/JPY is near 98.40 in latest dealings, remaining supported on dips sub 98.00 for now.

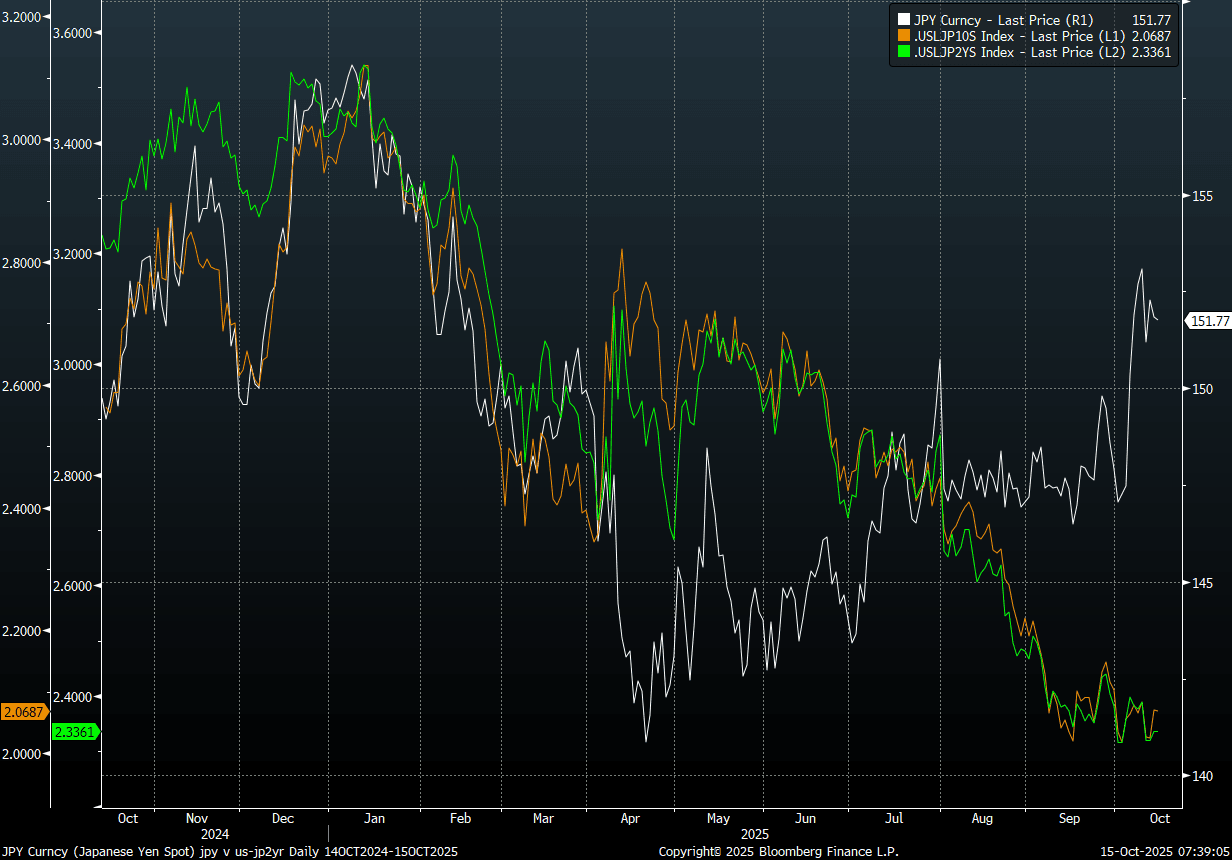

- Despite the bullish technical set up, more broadly, USD/JPY looks too high relative to US-JP yield differentials, see the chart below. Fed Chair Powell largely maintained status quo in terms of signaling another 25bp rate cut at the end of October, without a significant market reaction. Intervention risks also lurk in the background for USD/JPY.

- Some offset is coming from continued domestic political uncertainty. The chairpersons of the House of Councillors' Diet Affairs Committees from the governing Liberal Democratic Party (LDP) and main opposition Constitutional Democratic Party (CDP) met yesterday and agreed on the convening of an extraordinary session of the National Diet on 21 October (likely to elect a new PM). LDP leader Takaichi is seeking meetings with the three main opposition parties today (see this link).

- On the data front today we have Aug final IP, while a 20yr debt auction is in focus on the JGB side.

- In the option expiry space, note the following for NY cut later: Y143.00($1.8bln), Y150.00($1.1bln), Y151.55($956mln), Y151.95-00($500mln).

Fig 1: USD/JPY Versus US-JP Yield Differentials

Source: Bloomberg Finance L.P./MNI