JAPAN DATA: Inflows Into Japan Stocks Continued, Locals Sold Offshore Assets

At the end of Oct we still had positive offshore inflow momentum to local Japan stocks. Last week's inflow bought the late to Sep to early Oct inflow sum to nearly ¥7.15trln. Since the start of Nov we have seen equity weakness emerge, although so far the NKY 225 is supported sub the 50000 level. Market risk aversion is elevated amid AI valuation concerns and given the extent of recent run ups. We may see offshore investors trim some of their Japan holdings in response, although dips since April in benchmark Japan equity indices have been very well supported. Offshore investors added to Japan bonds as well, last week, but cumulative inflows were only modestly positive for most of Oct.

- In terms of Japan outbound flows, we saw local investors continue to sell offshore bonds. This marked the fifth out the last six weeks we have seen net selling in this space. Cumulative outflows to offshore bonds are still positive in recent months, due to chunky buying through September. Global bond returns have struggled for upside in recent months, largely flat since early Sep.

- Local investors also sold offshore equities, which was a consistent theme through much of Oct.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Oct 31 | Prior Week |

| Foreign Buying Japan Stocks | 690.1 | 1345.3 |

| Foreign Buying Japan Bonds | 280.6 | -249.2 |

| Japan Buying Foreign Bonds | -354.4 | -354.6 |

| Japan Buying Foreign Stocks | -581.1 | -62.1 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

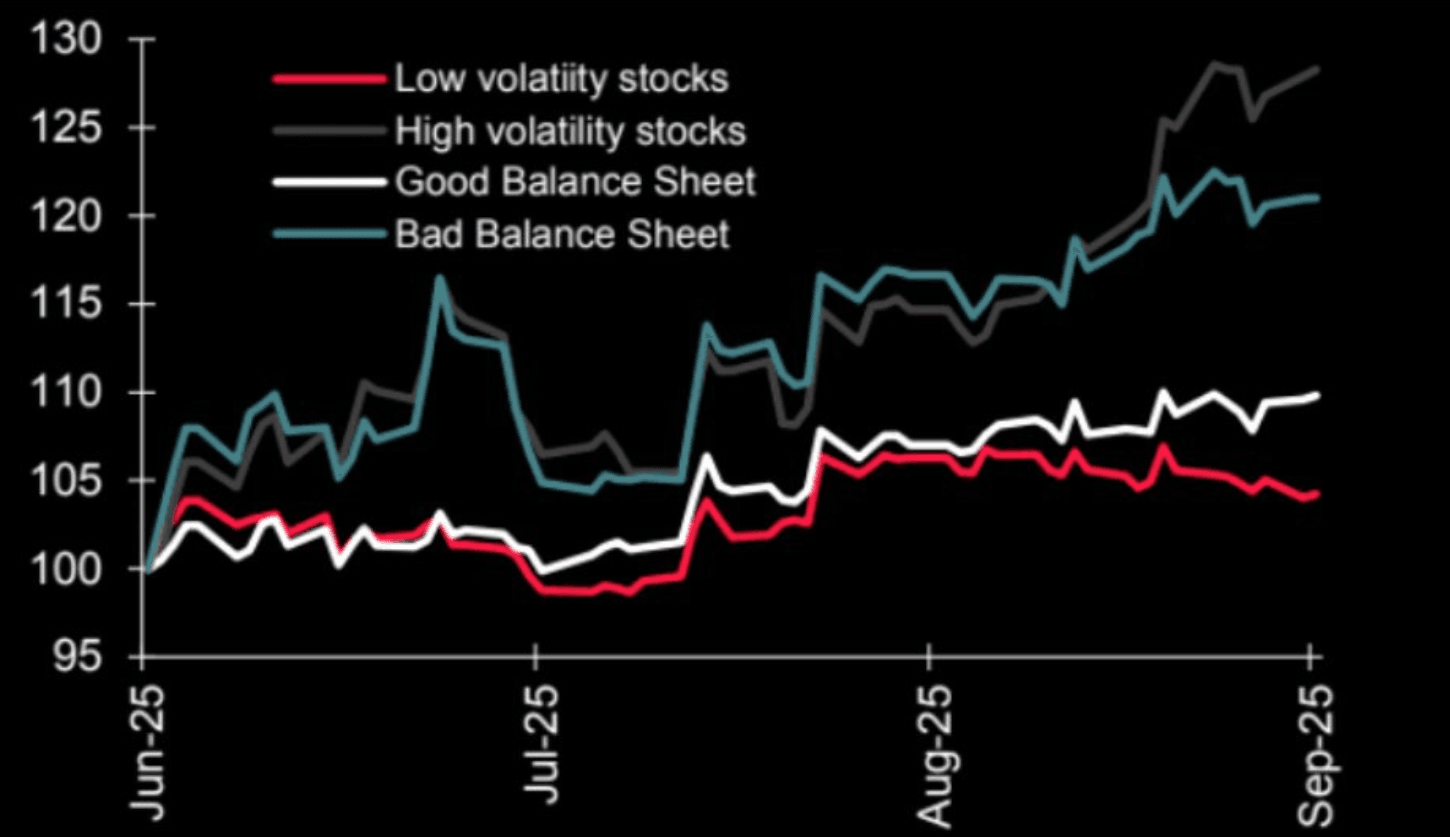

US STOCKS: Russell Index - Rejects 2500, Look For Support Back Toward 2400

The Russell 2000 overnight range was 2451.31 - 2493.10, closing -1.12%. The Russell 2000 took a sharp turn lower after briefly probing above 2500. The move in small caps has been more about positioning as the underperforming and least loved sectors have surged in the past month on short covering and momentum funds buying as new highs are being made. Are we seeing the first signs of this huge move finally running out of steam ? If we do at some point get some sort of a correction then small caps are likely to be hardest hit, the newly built longs will be looking for the price to sustain its break above 2400 and build a base from which to move higher, back through 2350/2400 and these longs will begin to be challenged.

- Lance Roberts on X: “Be careful of that small cap chase. 1) Small caps are the most economically sensitive stocks so much of the speculation hinges on a strong economic rebound. 2) After taxes and interest payments, net income is negative. 3) The majority of the current small cap chase is in high volatility and bad balance sheet stocks. Know what you own.”

- Zerohedge on X: "Incredible Demand": Retail Investors Buy Record-Shattering $100BN Stocks In Past Month.”

Fig 1: High Vol, Bad Balance Sheets Outperforming

Source: MNI - Market News/@LanceRoberts/@themarketear

AUSSIE BONDS: Smooth Digestion Of Mar-36 Supply With More Demand

The latest ACGB Mar-36 auction saw strong demand, with the weighted average yield coming in 0.22bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions.

- Moreover, the cover ratio nudged higher to 3.4917x from 3.3111x.

- As highlighted in our preview, bidding at today’s auction faced an outright yield that was roughly 10-15bps higher than the previous auction level and about 20bps below the late February peak.

- However, the 3/10 yield curve was slightly flatter than the previous auction level and sat 30-35bps flatter than its recent high.

- There has been no material movement in XM or the cash line in post-auction trading.

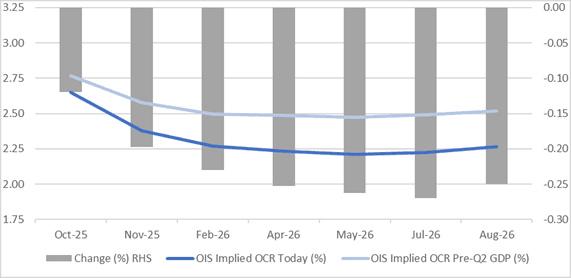

STIR: RBNZ-Dated OIS Set To Move After Today’s RBNZ Decision

RBNZ-dated OIS pricing is slightly firmer across meetings today ahead of today’s RBNZ Policy Decision.

- Easing expectations show 36bps of easing priced for today’s meeting, with a cumulative 63bps by November 2025 and 73bps by February 2026.

- Today’s decision is likely to have a material impact on pricing. A 50bps cut could bring forward the full 75bps of cumulative easing to November, while a 25bps cut would likely push at least half of that 25bps into early 2026.

- Notably, pricing is 12-27bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI