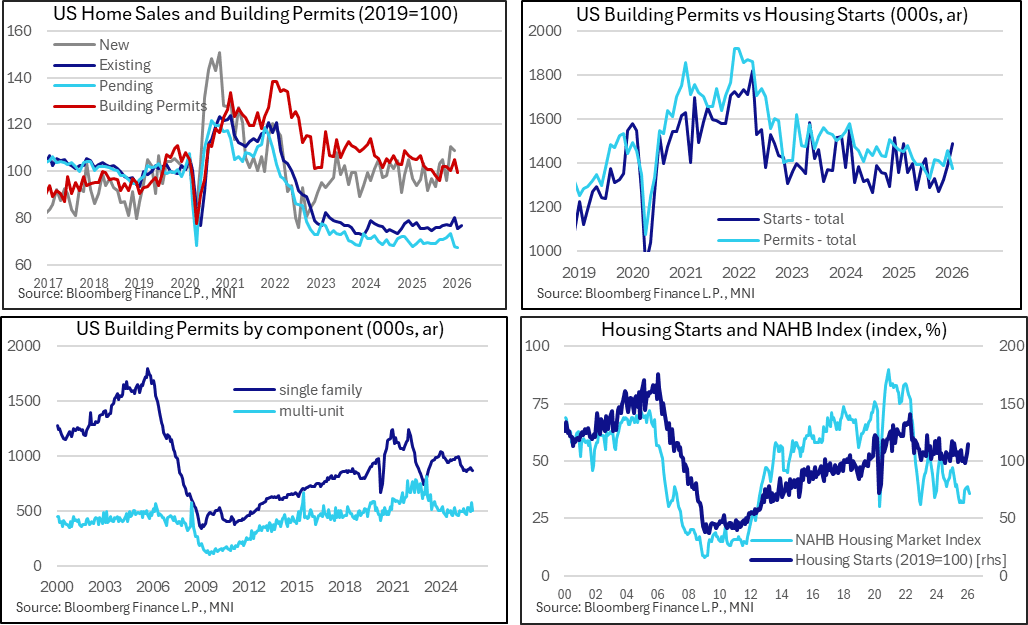

US DATA: Housing Starts Jump, But Permits Suggest Upward Momentum Is Elusive

Housing activity data was mixed to start the year, with starts jumping in January (as telegraphed by the previous month's rise in permits) but permits pulling back. The starts data were positive but at best, residential construction looks to be a neutral factor in overall economic activity in the early part of 2026.

- Starts posted an 11-month high 1,487k in January, well above the expected 1,341k and up from 1,387k prior (rev down from 1,404k).

- The breakdown of the jump parallels the trajectory of the prior month's permitting data. In December, permits rose to an 11-month high 1,455k, with single-family permitting dipping 15k but multi-units soaring 82k to a 28-month high. And in January, single family starts fell 27k but multi-units jumped 127k to a 32-month high.

- With permits demonstrating that they remain a natural leading indicator for actual activity, the 79k drop to 1,376k in January which marked a 5-month low, suggesting only limited momentum for housing activity.

- Notably single-family permits continued to wane (down another 8k to a 4-month low 873k), in line with the ongoing pullback in homebuilder sentiment, while multi-unit permitting dropped 71k though remains above the 500k mark.

- Overall, permits continue their overall multi-year deceleration, and we would need to see a meaningful sustained pickup here before assessing residential activity to be in any kind of recovery.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT PAOF RESULTS: The PAOF for the 4.125% Mar-31 Gilt was not taken up.

- GBP937.5mln had been on offer.

- This leaves GBP 24.842bln of the gilt in issue.

SONIA OPTIONS: SFIZ6 96.60 Puts Sold

SFIZ6 96.60 puts 12K sold at 10.0.

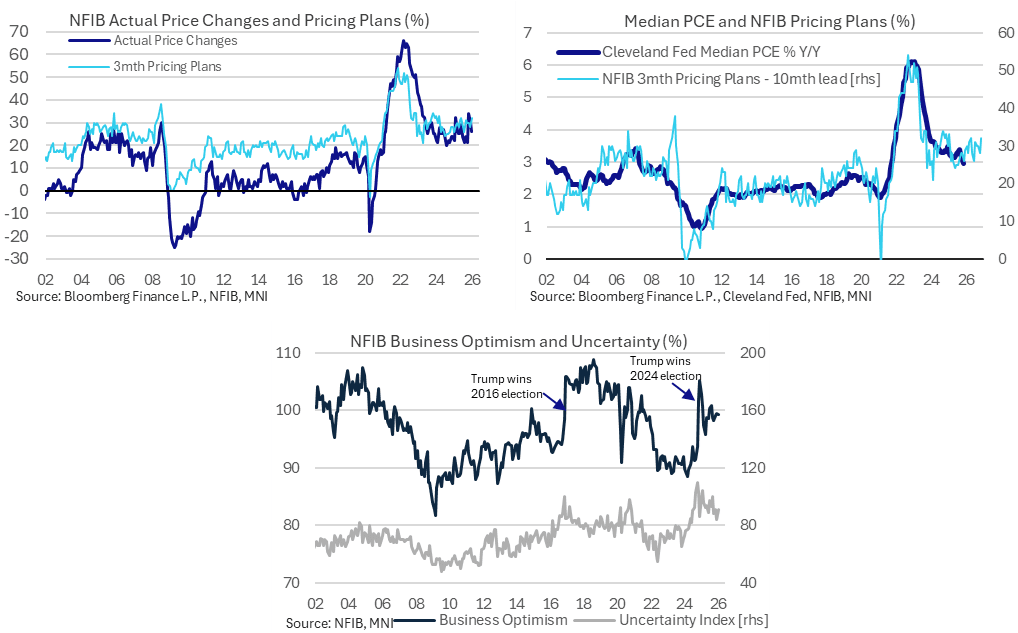

US DATA: Another Increase In Small Business Price Plans

The NFIB small business survey for January painted a mixed picture with its price components, with the net share who increased prices over the past three months at its lowest since October but those expecting to increase over the next three months at a joint high with June and last higher in early 2024. These price plans continues to point to inflation remaining stubbornly above the 2% target.

- Specifically, the net share reporting an increase over the past three months fell from 26% from 30% in December and a recent high of 34% in November. It averaged 11-12 pre-pandemic.

- Going against it, the net share expecting to increase prices over the next three months increased to 32% from 28% in Dec and 30% in Nov.

- It ties with the 32% back in June and was last higher at 33% in Jan and Mar 2024. For comparison, this series averaged 21-22% pre-pandemic and recently bottomed at 26% in August.

Price-relevant sections from NFIB member quotes in the press release (link) note insurance costs but also difficulty in passing costs on:

- “Insurance costs- business/liability, and health are having significant increases affecting uncertainty in pricing product.” – Construction, OR

- “Our business has been open since 1968. We are obviously doing something right for our customers. My struggle is passing on the increase in the cost of goods to my customers. That is a daily fight. I have to do it.” - Manufacturing, MI

- “Obtaining timely city/county permits is a nightmare. Takes months if not years for permits. Insurance eats up any profits, it just keeps going up and in our business we have limited sources that will insure us.” - Construction, CA

- “All my overhead has gone up significantly. My ability to raise my prices is negatively impacted by all the increased demands on my client’s “discretionary” income. Less taxes, less regulations, less bureaucracy, are the best help to my business and business prospects. Drastically less government spending and reduction of debt.” – Professional services, KS